Select your investor profile:

This content is only for the selected type of investor.

Investisseurs particuliers?

Positioning for a sea change in fixed income

Bonds are expected to have more volatility than in the past: this will offer careful investors rewarding opportunities.

Written by

Mary-Therese Barton

Chief Investment Officer Fixed Income

It’s a new era for fixed income investing. Investors are only slowly catching on to how significant a shift we’ve undergone from the post-global financial crisis decade of zero interest rates. Which is to say, investors can once again expect to be rewarded for holding bonds and credit instruments. But there’s a catch: unlike the generational bull market that started in the early 1980s, this time the tide won’t be lifting all boats. These waters require deft navigation.

With bond yields higher than they have been for many years, investors no longer need to seek out quality stocks in order to generate return – as they did during the long years of official zero interest rate policy. The bond and credit markets can once again be relied for significant income, which, in turn, gives a buffer against volatility.

But yield isn’t the only source of return from these instruments. There is also scope for considerable capital appreciation as the interest rate cycle starts to turn down – though a likely rise in market volatility will necessitate a careful and active investment approach. As a result, smart investors should be able to generate high single digit returns from fixed income for years to come.

From barbell to belly

During 2023, a barbell approach worked well for investors. That meant, on the one hand, taking substantial positions in money market instruments, making the most of some of the highest low-risk yields available for decades. On the other, investors allocated their risk budgets on illiquid but high-return instruments like private credit.

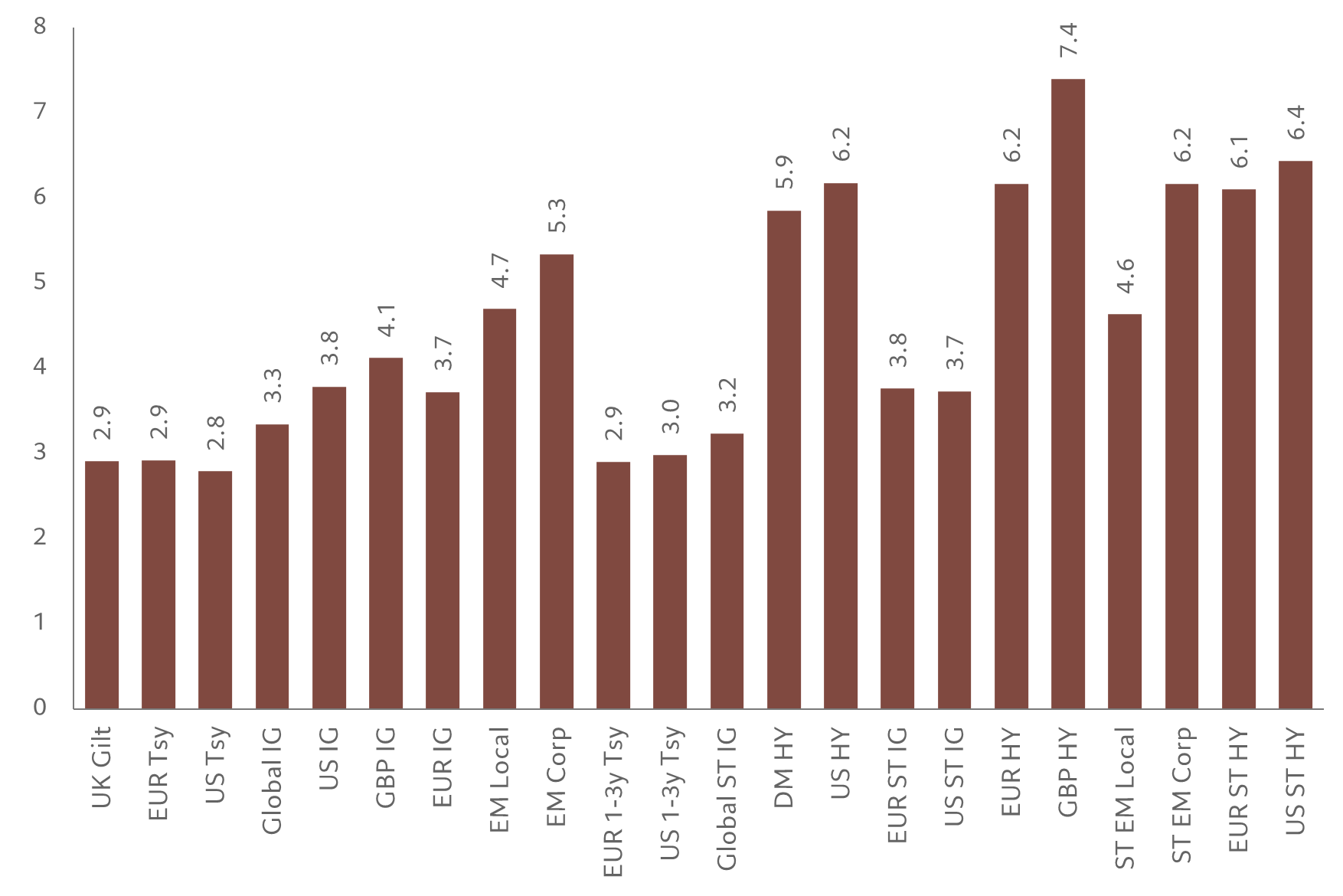

But now, with official rates plateauing and market rates starting to come down as developed economies also start to slow, the most attractive opportunities are spread right across the risk spectrum: in credit, sovereigns and, not least, emerging markets, as well as in money markets and private markets (Fig.1).

Fig. 1 - A universe of yield

Yield to maturity for various fixed income segments, hedged in euros, %

That, though, will take some dexterity. Unlike past cycles, it won’t be enough for investors to buy and hold. That’s because the course of monetary policy is unlikely to run quite as smoothly as the market seems to be anticipating.

For instance, the market has been overambitious in how quickly and deeply the US Federal Reserve is likely to cut rates this year. Inflation is proving stickier than many were hoping, particularly in the services sector. And, in a world of very high government debt loads, substantial fiscal deficits are bound to keep upward pressure on yields.

A monetary policy path of a slow pace of rate cuts and relatively high terminal rates is likely to trigger significant interest rate volatility. With volatility comes dispersion of returns across asset classes and instruments. And dispersion creates a landscape that favours well-informed investors, who then are able to generate excess returns though application of analysis and insight.

Emerging attractions

Emerging market (EM) bonds in particular are poised to be an important, if much neglected, source of excess returns over the coming years. Although returns from the asset class during 2023 were stifled by wild swings in developed market bond yields and disappointment with China’s recovery, there are a number of reasons to be positive about the market for the coming year.

First, the volatility that has roiled even the safest sovereign bonds ought to dispel the notion that developed markets equals stability while EM spells volatility.

Second, China is less important to the market than it once was. Yes, the wider EM market has tended to look to it for a lead – China is a big source of demand for Southeast Asia as well as a major source of tourism revenue – but as these economies have matured, domestic demand has become an ever bigger engine of growth. That, in turn, has been attracting foreign direct investment.

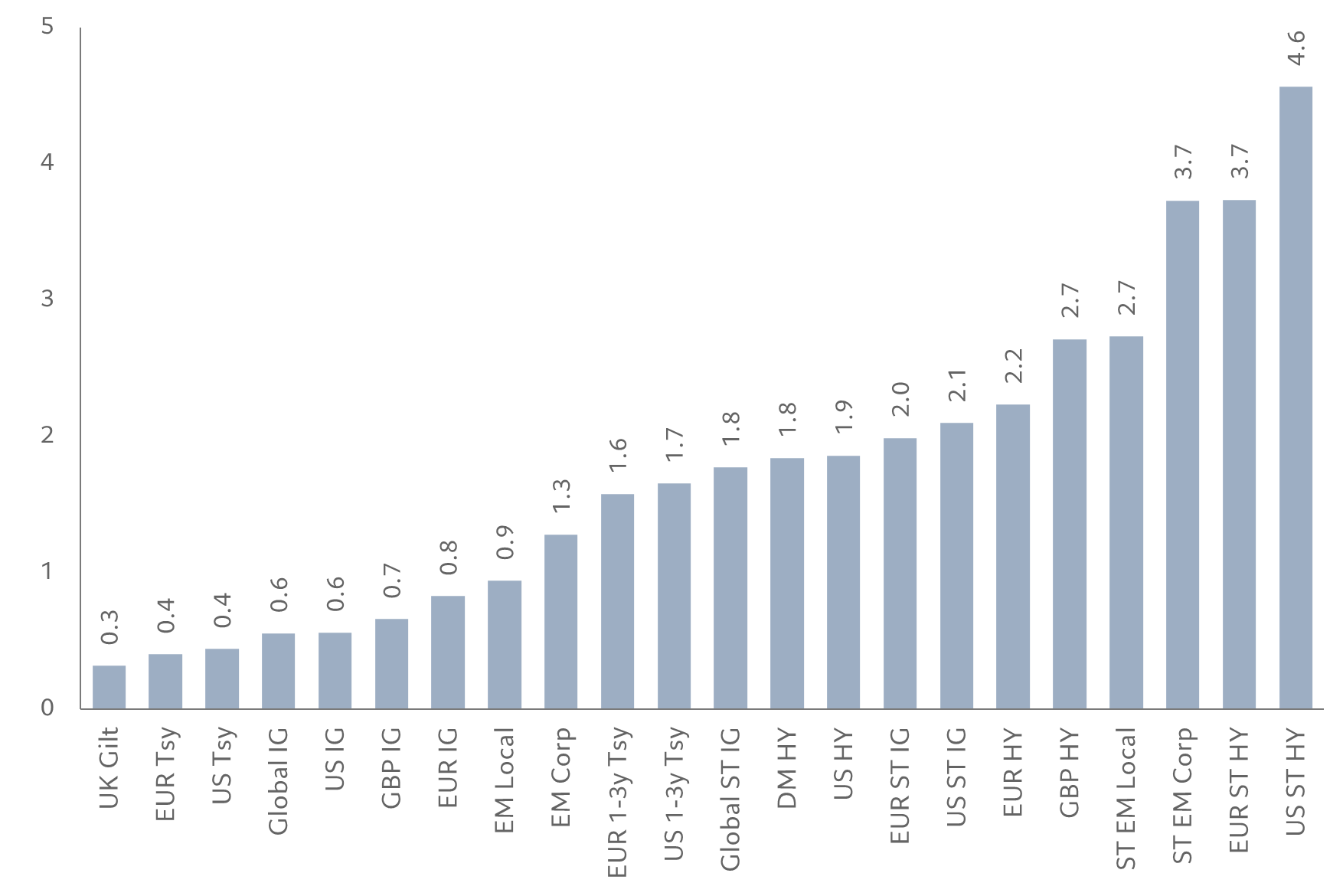

Fig. 2 - Margin of safety

Breakeven rates for various fixed income segments, hedged in euros, %

Passive risks

Investors grew so used to a lack of dispersion in returns across fixed income and a general lack of yield during the years of quantitative easing and zero interest rates, that passive index-based products became increasingly attractive. After all, when excess returns were hard to come by, it made sense to focus on reducing costs.

That’s no longer the case. Higher yields and significant market dispersion make an active investment approach much more advantageous. When the difference between outcomes is the difference between mid-single digit returns or high single or even double digit returns, the difference in costs between passive and active styles becomes less relevant.

It's a new world for investors, one of considerably more volatile inflation and therefore of more volatile interest rates.

Related articles

Fixed income through the investment cycle

There are fixed income assets for every economic scenario.

October 2023

A short cut to better bond returns

The volatility of the fixed income market has left investors wary. But the yields offered by shorter-dated bonds are as attractive as they have been in quite a while.

November 2023

Higher for longer than you think

Investors are overly optimistic about how soon and deeply central banks will be able to cut rates. The fight against inflation isn't won yet.

January 2024

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The NAV are available at www.beama.be.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.