Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Tech: here for the long term

Technology isn’t all volatile start-ups or new gadgets. It's a sector whose prospects make it an attractive investment for the long run.

Written by

Anjali Bastianpillai

Senior Client Portfolio Manager

Lyft and Uber IPOs have dominated tech sector headlines, with investors first snapping up shares in the car-sharing firms only to dump them weeks or even days later. Such a quick turnaround in sentiment is clearly unsettling. But it is not indicative of the tech sector as a whole. In fact, tech stocks are up over 15 per cent since the start of the year1, the strongest performance of all the sectors.

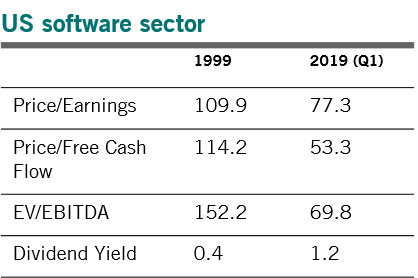

Fig. 1 Getting stronger

That’s in part because the sector benefits from long-term structural trends: technology’s role in our lives is growing by the day. For investors willing to take a longer term view – and ignore the market noise – the potential rewards are attractive.

Compared to the dot.com boom of the late 1990s, the companies in the tech sector today are in a different league when it comes to their fundamentals.

To begin with, tech firms are profitable, with room for manoeuvre should times get tough. These days, the median US tech company has a free cash flow (FCF) of USD349 million compared to just USD46 million two decades ago2. And the sector now contributes nearly a fifth of S&P 500’s earnings, up from 10.3 per cent in 1998.

Secondly, while valuations are, undoubtedly, less attractive on average than they were a year or two ago, they are still a long way off the ultra-stretched levels seen in the run-up to the dot.com bubble.

According to our calculations, US software companies, for example, are more attractively priced now on every major metric than they were in 1999. Such stocks' price to free cash flow ratio now is less than half what it was then, while the dividend yield is three times higher (see Fig. 1).What also distinguishes tech today from tech in the 1990s, is that its influence spans virtually every industry sector, engaging businesses and consumers alike.

Take artificial intelligence, for example. Google is working with AI, through DeepMind and RankBrain machine learning systems, to improve its search engine. Amazon uses AI to learn about your shopping preferences and predict your most likely purchases, as well as for Alexa. Microsoft’s personal assistant Cortana can help predict business outcomes - such as demand for your product - based on machine learning. Facebook’s investment in AI includes natural language processing, real-time analysis of news feeds and facial verification software that is able to identify people in pictures with over 97 per cent accuracy.

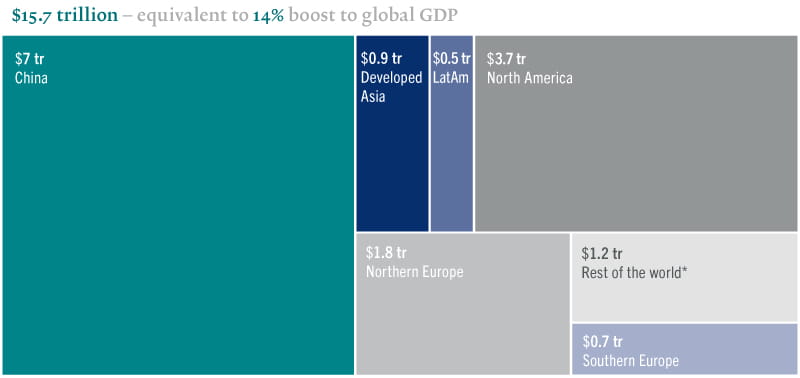

By 2030, AI is expected to have boosted world GDP by 14 per cent – or some USD15.7 trillion3.

Fig. 2 economic benefits

AI's forecast contribution to world economic growth in 2030

* Developed Asia includes Japan, South Korea, Taiwan and Singapore. Rest of the world includes Africa, Oceania and rest of Asia.

Source: PWC, "Global artificial intelligence study: sizing the prize", 2017

To accommodate this, the world needs more data storage, tougher digital security and faster networks. Cloud computing is evolving to meet the challenges of exponential data collection on a pay-what-you-use basis. Revenues in the sector are set to grow five-fold from 2017-2022 to USD331 billion, according to research consultancy Gartner. We believe that is just the beginning: there is potential for spending on cloud technology to grow ten-fold from current levels.

When it comes to networking, 5G can help improve wireless network speeds by a factor of 10, whilst reducing delays (latency). Crucially, this technology is designed with AI in mind, which means it is capable of collecting exponential amounts of data. The US is taking the lead, with telecom equipment firm Verizon expected to have 30 cities connected by the end of the year. Gradual rollouts are also underway in Japan, Korea and China and 5G is expected to be globally widespread by 2025 according to Bank of America Merrill Lynch.

Increased digital security, meanwhile, can come from blockchain. The cryptocurrency bubble may have burst, but for blockchain that’s arguably been good news, pushing the technology more towards real world applications. Its ability to fragment data and keep it private has applications everywhere from banking and online shopping to human resources and logistics. By 2030, blockchain will create USD3.1 trillion in business value4.

Of course, every industry and every investment comes with its own risks, and tech is no exception. The two main threats come from regulation – as US and European governments crack down on cyber security – as well as from the global trade war. It is important to be cognisant of these risks, but they can also create pricing anomalies and thus attractive investment opportunities, particularly as some tech stocks are more likely to be impacted than others.

Overall, the tech sector is now much more diverse and more profitable than it was two decades ago. The long-term opportunity is as attractive as ever, while the broad sector’s ability to withstand any potential bouts of volatility is much stronger than it was during the dot.com bubble.

read more

The future's bright the future's digital

Digital technology has radically changed our lives in the past decade. The rapid progress is set to continue.

February 2019

Demystifying thematic equities

Actively-managed by specialists who conduct rigorous company research thematic equity funds are designed to help investors get the most from their stock investments.

February 2018

Beyond the FAANGs

Think the tech sector's fate is in the hands of a few big name stars? Think again.

August 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.