ESG in Practice series: Gabriel Micheli on environmental investing

A deep appreciation for nature runs in the family for senior investment manager Gabriel Micheli, who has been shaping environmental portfolios for the past 15 years.

Written by

Gabriel Micheli

Senior Investment Manager

How long have you worked in environmental investing?

I joined Pictet in 2006, precisely as Water was becoming a multi-billion strategy. I was thrilled to be involved in the launch of a new environmental strategy, Clean Energy, in 2007, because I wanted to apply my knowledge of economics and finance to have a positive impact on the environment. I strongly believe that as a shareholder you are in a very good position to do that. Quickly thereafter, in the middle of the crisis in 2008, I participated in the launch of Timber strategy with the aim of investing in sustainable forestry. We then progressed to a concept that would combine all our environmental strategies - Water, Clean Energy and Timber - into one. We had secured a few institutional mandates by 2010 but it took a while to come up with a coherent concept, because many companies that were linked to our themes sometimes solved an environmental issue, but at the same time caused damage on other dimension.

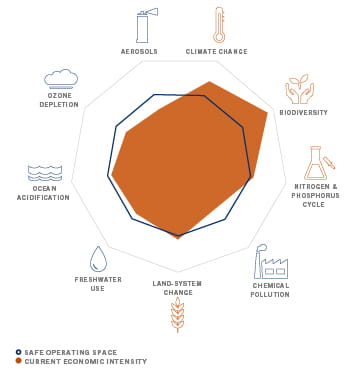

The Planetary Boundaries framework

At the time, climate change was talked about but pollution, biodiversity, or plastics were not necessarily perceived as problems. My conviction was that by focusing on one environmental dimension you ran the risk of creating problems elsewhere. With the help of my highly creative colleague Christoph Butz, who as a trained forest engineer has a deep understanding of earth systems, we created an investment methodology based on the Planetary Boundaries.

It is a scientific framework that presents a holistic view of all environmental issues, and that recognises that each dimension has a limit that we should not exceed. The investment methodology we came up with was very innovative at the time. We're still improving it but now it's becoming more mainstream and you see many books or documentaries featuring the planetary boundaries; it's becoming a common language. We have been calculating the impact of companies based on this methodology for years.

The European taxonomy that is being implemented now uses our methodology almost exactly: in addition to climate change adaptation and mitigation, there are four other dimensions that really correspond to our planetary limits. With the double approach of "do no harm", so stay within planetary limits, and “do good”, or improve the situation on at least one of the dimensions.

We want to remain on the cutting edge and to develop today the strategies that clients will be asking for in five years’ time.

What do you make of the trend towards net zero?

It’s a step in the right direction, but sadly so far it does not yet change the long-term trajectory. Today we have an economy that’s degenerative for the environment: everything we do partly destroys the planet. Large brands going green are essentially aiming to do a little better than before, but this is still degenerative on the whole, in my opinion.

We need to go beyond net zero – it is becoming increasingly clear we have to restore what we've destroyed. We have to put carbon back into the earth with regenerative agriculture or by planting trees; we have to find new technologies. What we need above all is a level of structural organisation where we move towards an economy that is regenerative, that is circular, but in addition, brings something positive for biodiversity or nature. This would be modelled on systems in nature which perpetually regenerate themselves. Destroy a forest and it will eventually regenerate itself. We should have an economy that is based on that structure. As shareholders we can be partners to companies that embark on that path. My conviction is that for a company to survive, to deliver superior growth, to be innovative, to hire the brightest talent, it will have to adopt that new structure.

Do you find it easier to get your environmental views across today?

It’s impressive how much has changed in the last few years. When I started, there wasn’t a consensus on why fertilisers, plastics, air conditioning, nuclear energy, or even pesticides did not belong in an environmental investment strategy. We did not hear much about biodiversity until a few years ago. Plastic pollution has only really been talked about since the BBC documentary Blue Planet featured the damage to the oceans, but it’s always been an issue! Today, a much larger share of the population feels concerned, and surprisingly it’s accelerated with the Covid crisis. The younger generation seems to have these issues at heart; for most people we hire today it’s a no-brainer.

Ten years ago, I wouldn't have bet on such a sudden change in this direction. I believe that sustainable investing was still a niche because of the prevailing thought that imposing ethical considerations on investments would result in underperformance since it would constrain the investment universe. We no longer need to have that debate now, the track record of our environmental strategies speaks for itself.

Corporate engagement was seen as negative by investors who worried that it might strain relations with company management. Today companies come to us for advice because they realise that capital flows towards those with the best ESG scores. In the Timber strategy which I used to manage with Christoph, we have always had discussions with companies on the best silvicultural practices and maintaining a good level of biodiversity while producing valuable timber. We’ve always pushed companies to adhere to high standards in sustainable forest management since the value of our investee companies is determined in large part by the sustainability of their forestry assets.

We need to go beyond net zero. We have to restore what we've destroyed.

Have you always had an interest in responsible investment?

My family always had a strong connection to nature that was passed down to me. In Geneva there was a very strong environmental impulse in the twentieth century. I think it’s in line with the legacy of three major historical figures - Jean Calvin, Jean-Jacques Rousseau and Henri Dunant, who imbued Geneva with a sense of openness towards the world, a sense of justice and compassion which we call the “Geneva spirit”. This did extend to the environment with figures like Robert Hainard, a naturalist painter who was a friend of my father’s, who inspired a whole generation to appreciate nature in its wild and free state. My father himself is an ornithologist who has spent his whole life with binoculars around his neck. We lived close to nature and that’s still part of everyday life for me.

I travel by electric bike, I have a wood pellet heater, I've been a vegetarian for about fifteen years, and recently started a permaculture food-forest in my garden. I try to limit the impact I can have on the environment in everything I do. I adhere to the systemic thinking that everything in nature has a place and a purpose, and every time you take away a component of the system, it might affect the whole system. My wife used to be a lobbyist in Brussels, fighting pesticides in agriculture. We try to transmit our love for nature to our three children.

RELATED ARTICLES

ESG in Practice series: Stéphane Rüegg on credit

Credit expert Stéphane Rüegg discusses what's on the mind of his clients, the nascent green bond market and his very personal view of responsible investing

November 2021

ESG in Practice series: Mayssa Al Midani on engagement in the Nutrition strategy

As active managers, we can collaborate with portfolio companies to trigger positive change. Mayssa Al Midani, Senior Investment Manager, shares her perspective on environmental and social engagement with food companies.

August 2021

ESG in Practice series: Cédric Lecamp on engagement in the Water strategy

For Cédric Lecamp, managing a USD10 billion strategy with a 20-year track record means he has an outsized opportunity to engage with companies and push for change.

July 2021

more about our ENVIRONMENTAL STRATEGIES

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.