The great resignation or the great re-direction?

The world of work is changing, with many leaving the workforce. Covid may have accelerated this shift, but ultimately it's down to demographic, social and technological trends.

Written by

The Thematic Advisory Board

The world of work has undergone dramatic upheavals over the past couple of years – not least a wholesale flight from the labour force. Whether the Covid pandemic triggered these changes or merely accelerated longer-term trends is moot. But what seems apparent is that many of these changes are becoming embedded, according to the Pictet-Human Advisory Board.

No one anticipated the great resignation, as the rapid withdrawal people from the workforce is called. But the pandemic seems to have caused demographic, social and technological trends to converge in such a way that has encouraged people to reconsider the way they conduct their working lives.

According to the Advisory Board: people are looking inward and seeing different possible selves. This isn’t a new phenomenon, the trend was already in place before the Covid outbreak. Though it is the rapidity with which it took hold after the spread of the pandemic that has been surprising.

One explanation for the sudden surge in resignations is high rates of personal savings, which have grown thanks in part to income support and other pandemic stimulus efforts.

That’s particularly true of people over 55, many of whom didn’t return to the workforce as economies rebounded. Unlike in the past, it’s not that they left unrewarding or unsatisfying jobs for better ones. They just disappeared and we can’t be certain what they’ve gone on to do.

In some cases they will have decided to retrain or to volunteer for charitable work. Education is typically becoming a life-long pursuit. This is fueling demand for less formal training but more varied certificates. There is evidence that people are turning away from professional training, like law or business administration where post-graduate admissions have been dropping off over recent years.

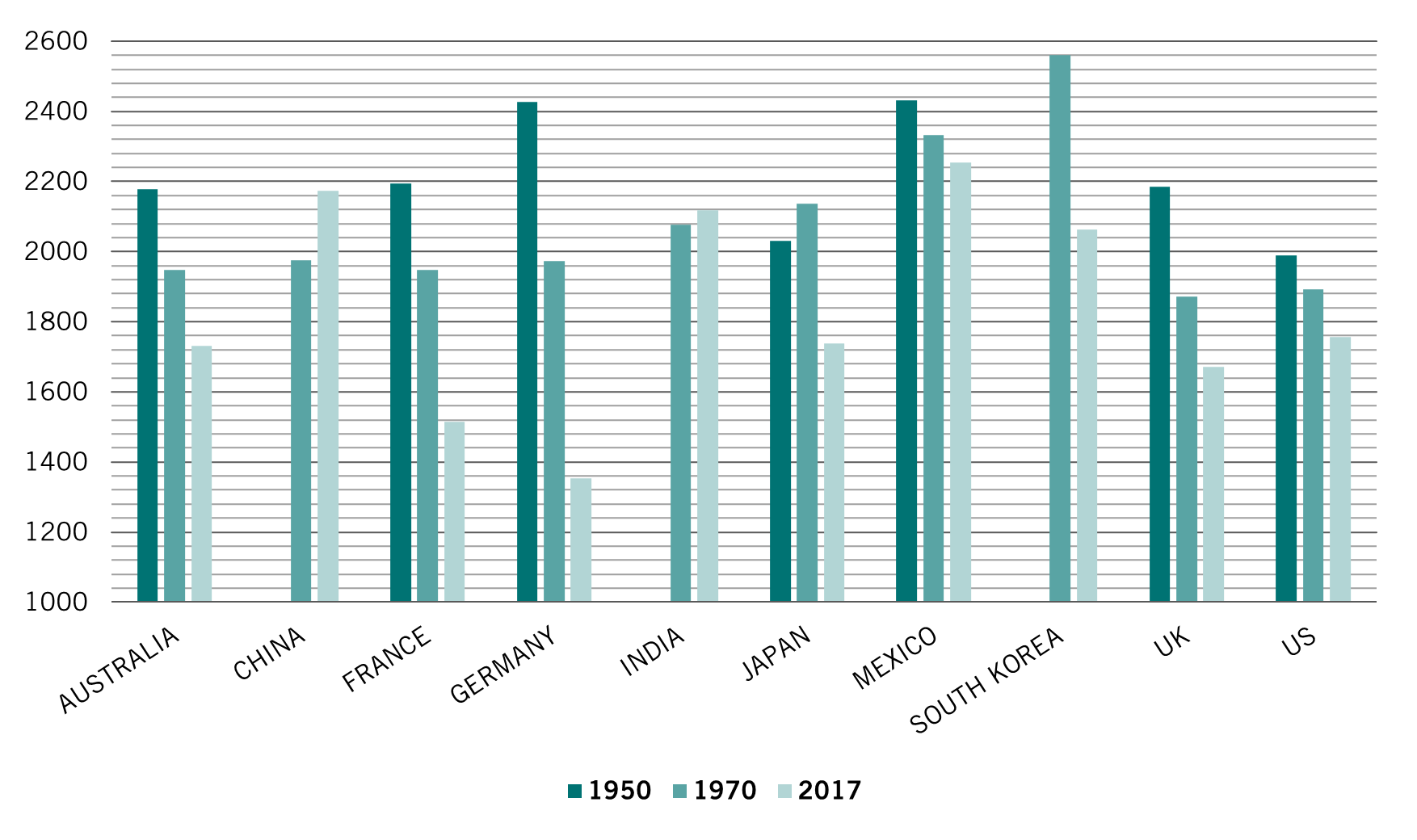

Working smarter not harder

Average working hours per worker over a full year

Some are preferring to develop their manual skills, from plumbing to printmaking, and on-line learning means that the sources of education has been globalised. This has allowed people to shift from long-term commitment to single employers to portfolios of paid and unpaid jobs.

Tight labour markets mean that companies are having to be increasingly flexible in how they attract workers. Many are undergoing major workforce experiments, often beyond work-from-home concessions. It’s a very brave chief executive who is determined to go back to how things were pre-pandemic.

Some of this is likely to include automation of more functions – for instance, robolawyers and roboaccountants are likely to take over mundane tasks, leaving their human counterparts to do the more highly skilled functions. In fact, in 60 per cent of jobs, around a third of tasks can already be automated.

In other cases it will mean making the workplace competitive with the home for atmosphere. So there will be an increasing mix of what makes offices successful – serendipity as a product of accidental interactions, scope for effective mentoring and coaching, the human touch of meeting colleagues – with the benefits of home work, including less time spent commuting, fewer interruptions and more comfortable spaces.

This picture is complicated by inflation. Exceptionally low rates of unemployment and large numbers of vacancies mean workers currently have some leverage over employers. But unless they unionise, some of these gains will be lost to inflation. Rising prices will increase the need for people to supplement or boost their earnings, which will push them more towards the marginal and less-favoured jobs and force them to work longer. Tighter monetary policy that accompanies inflation will, in turn, reduce employment opportunities as business investment cools.

However, the pendulum of power swings between workers and their employers, the face of employment has undoubtedly changed. There might be a reversal of the great resignation if economic conditions prove more difficult in the coming years, but the re-direction of the nature of employment seems likely to stick. A wide spread of sources and types of education will help people develop their skills and the development of technology that allows learning and working to be done remotely ensures that the future of work will be different from its past.

The trends and technologies discussed in this article are some of the investment themes that inform the Pictet-Human strategy, which centres on services that help us adapt to the demographic and technological shifts that are changing our lives.

Related articles

Ageing population and its impact on business

Some industries are beginning to adapt to the needs of a longer-living population, boosting the world economy's long-term prospects in the process.

Mar 2021

Robots in the workplace

Robots are revolutionising how we work and the jobs we do. Is it all bad news?

Jul 2017

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.