Asset allocation: China's stumbles a cause for concern

The sell-off that rattled global stock markets in early February has largely been blamed on signs the US economy could be overheating. That is still a risk, but it’s not the main reason we find equities’ near-term prospects uninspiring. Our primary concern is China. There, economic growth is slowing as authorities in Beijing make yet another attempt to deflate the country’s credit bubble. So far, thanks to healthy demand for Chinese exports, the tightening of monetary policy has not done too much damage. But if, as seems likely, the pace of credit growth slows further and US President Donald Trump enacts additional protectionist measures against China, the prospects for emerging markets and the rest of the global economy will look less rosy than they did a few months ago.

Also likely to hold stocks back is a change in monetary conditions in the developed world. While an extreme example, China is not alone in reining in stimulus. In the US, new Federal Reserve Chairman Jay Powell used his first testimony before Congress to suggest that the pace of rate rises could quicken in 2018 as economic growth and inflation gather strength. The same looks likely in the UK. And while the Bank of Japan and the European Central Bank retain quantitative easing for now, both are certain to retrench later this year.

It’s not all bad news for equity markets, however. More positively for stocks, the February sell-off has lowered price-earnings (P/E) multiples to fairer levels. Taking all this into account, we have opted to retain our neutral stance on equities.

Elsewhere, the draining of central bank stimulus threatens something more serious for the fixed income market. We remain underweight bonds, concerned that European markets in particular have yet to factor in the prospect of an end to ultra-easy money.

Our business cycle indicators show the global economic expansion is slowing.

While the US remains in good shape – unemployment is close to its lowest since the 1960s and we expect output to expand 2.8 per cent this year versus a previous estimate of 2.6 per cent – China is heading in the opposite direction.

Activity in the country’s manufacturing sector declined at its fastest pace since 2011 last month, according to the purchasing managers’ index. Nor is this slowdown limited to China. Both our emerging market and global leading indicators have declined somewhat over the past two months, albeit from very healthy levels.

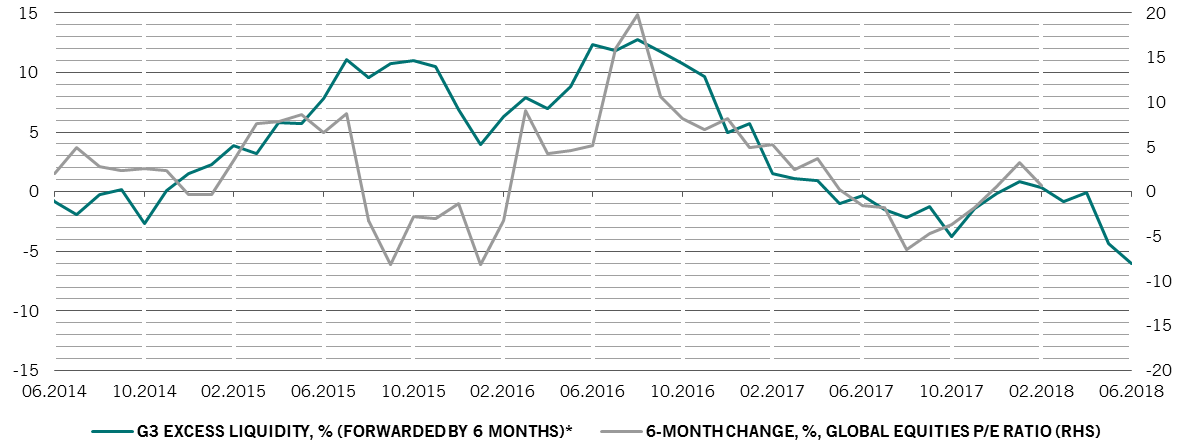

Our liquidity readings show that monetary stimulus is being steadily drained from the financial system. In our model, central bank policies are stimulative when money supply is growing at a faster rate than industrial production.1 That differential, which we have found has a positive correlation with stocks’ earnings multiples, is now at its narrowest in seven years, suggesting P/E ratios could contract by some 5 to 10 per cent over 2018 (see chart). That would counteract any potential acceleration in corporate profits.

Tighter liquidity conditions could weigh on stocks' earnings multiples

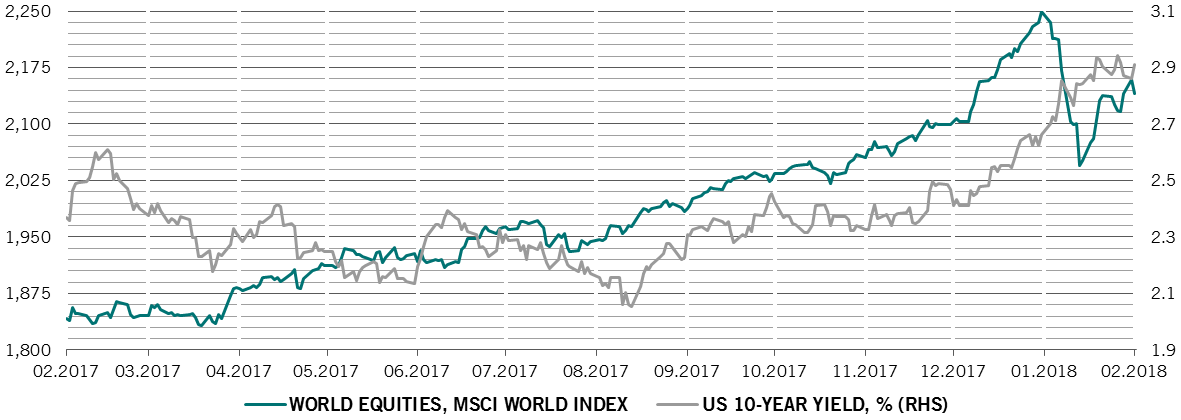

The February sell-off has returned valuations for some equity and bond markets to fairer levels. But US stocks continue to command what we consider to be an excessive premium over European ones: the gap in their respective price-to-book ratios is now at its widest since 1993 (3.5 vs 1.7). The recent rise in bond yields, meanwhile, has given rise to attractive opportunities in longer-dated US government debt (see fixed income section).

Our technical indicators provide a neutral signal for equities but a clear "sell" signal for developed market bonds. Our readings on the US dollar, meanwhile, suggest the currency may be due a rebound. That’s because professional investors have largely favoured setting up short positions in the dollar, an imbalance in positioning that limits the scope for further falls in the currency.