Rising inflation and improved corporate governance have turned the tide for Japanese stocks.

Written by

Sam Perry

Senior Investment Manager

Share this article

Japanese equities are entering a new era. Two developments in particular have forced companies to rethink how they do business – for the better.

First, years of corporate governance reforms are starting to pay off, with a growing number of Japanese firms becoming more strategic and focused in their approach. Second, inflation has finally returned after two decades of stagnant prices and wages. That means it no longer makes sense for businesses to keep large piles of cash on their balance sheets – a relief to investors who have looked on helplessly as Japanese companies amassed some JPY258 trillion of funds that could have been put to more productive use.1

Over the coming months, we expect companies to start spending those cash piles. The quick and easy way to do so would be through share buybacks and dividend payments. The more strategic, long-term options include merger and acquisition activity and capital expenditure. Either of which would be good news for investors.

Spending spree

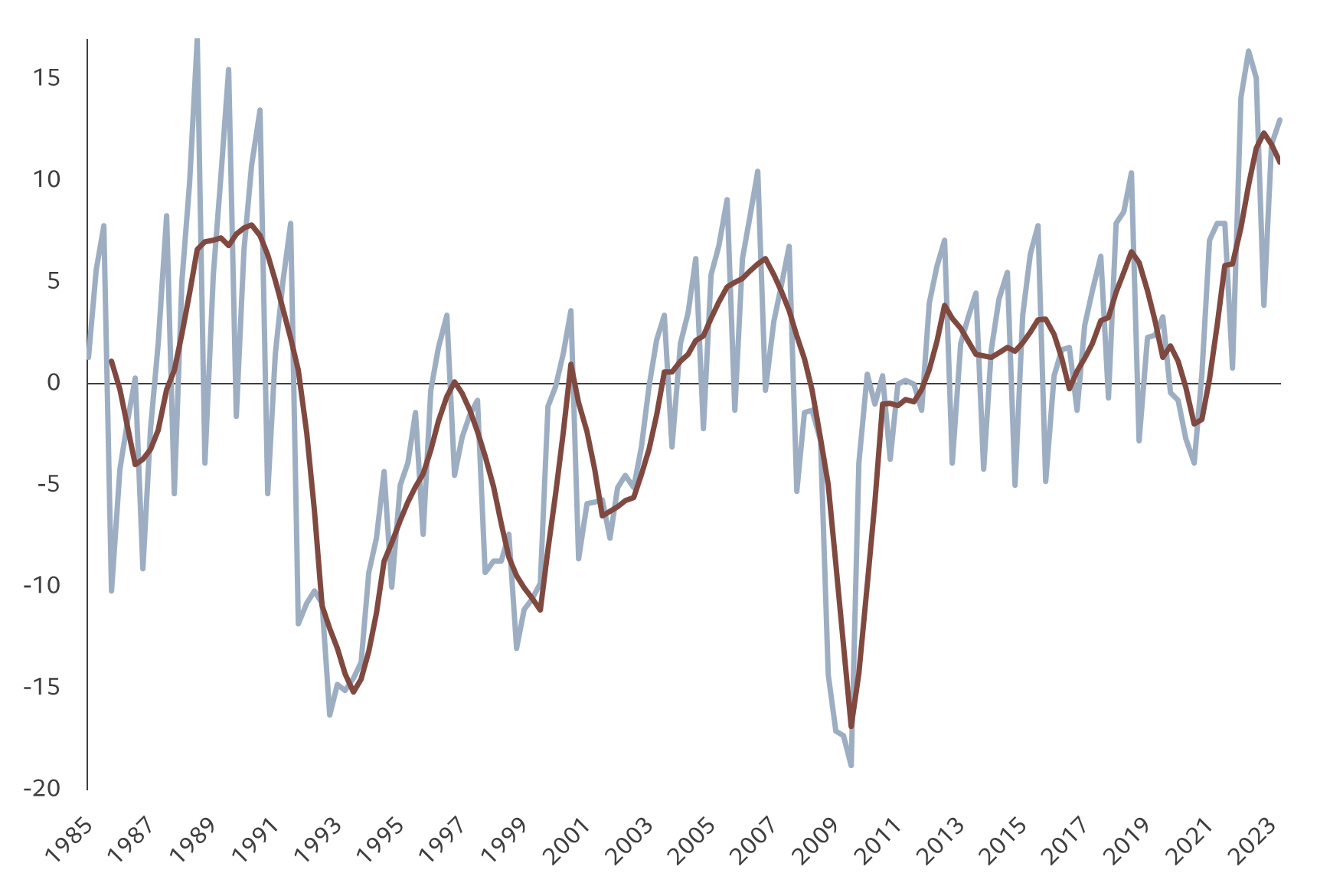

We are already seeing signs of companies loosening their purse strings. According to the Tankan survey, they are intending to invest faster than they have at any point in the last 40 years (see Fig. 1). That momentum will only strengthen as domestic economic activity picks up. (Our economists estimate Japan’s gross domestic product to grow by around 1.5 per cent in 2024 – above potential and faster than both the US and the euro zone.)

Fig. 1 - Ambitious investment plans

Fixed investment intentions (Tankan survey, all companies 4Q moving average)

Source: Bank of Japan, Pictet Asset Management. Data covering period 01.06.1985-30.09.2023.

Given the size of the cash pile at Corporate Japan’s disposal, we expect this investment to be material and to lead to not only increased capital expenditure, but also increased M&A activity, increased share buybacks and increased dividends. As balance sheets normalise, we will also see an rise in leverage from current lows. (Adjusting for different sector weights and excluding financial stocks, the median leverage of Japan’s TOPIX 500 stands at around 2.19 times compared to 2.79 for the US S&P 500.)2

The increase in leverage will then lift the Return on Equity (RoE) for Japan. While many people rightly point out that Japan’s RoE is considerably lower than that of, say, the US, it is less widely understood that, once adjusted for the different sector weights, the median Return on Assets of the TOPIX 500 index is very close to that of the S&P 500. The difference in RoE is in small part due to the different rates of corporate taxation and in large part due to leverage: Japan has cash, the US has debt. That is about to change.

The positive shift in Japan’s balance sheets and business practices comes at a time when the structural dynamics are also looking very positive thanks to corporate governance reforms. Today, 97 per cent of listed companies now provide English investor materials (up from 80 per cent just three years ago), while 99 per cent have at least two independent directors (from 22 per cent in 2014). Cross-shareholdings have fallen to new lows, as Japanese companies focus on core competencies.

Authorities have also opened up tax free investments in Japanese stocks for domestic investors, further boosting demand for equities.

Stock pickers' advantage

But not all companies will cope equally well in this new normal. Managed well, increases in capital expenditure and M&A can be a route to stronger business growth and improved returns for investors. Yet poorly devised investment plans can have the opposite effect . So while investing in Japan Inc in general should reap rewards, a bottom-up, stock picking approach could help maximise returns by drilling down into the idiosyncrasies of each company.

Take the tech industry, for example. Tech in Japan looks very different to tech in the US. The latter is focused on communications services and service system providers and dominated by a handful of giants like Alphabet and Microsoft. Japan’s tech sector is much more diverse, featuring precision engineering, electronic components, and high-tech functional materials.

While investing in Japan Inc in general should reap rewards, a bottom-up, stock picking approach could help maximise returns by drilling down into the idiosyncrasies of each company.

A company at the cutting edge of its industry and with strong governance should be well-placed to reap great rewards from additional investment. That’s where an active investment approach can show its true value. In the Pictet Japanese Equities team, we do not start our bottom-up process with a fixed style of company in mind. We are agnostic about whether we find valuation upside from the market’s misperception of the balance sheet and the probability of realising its value (classical value investing) or from its misperception of the company’s likely future growth (classical growth investing). That frees us to select what we believe are superior stocks regardless of style. Valuations are an important consideration. So, for example, while the pharmaceutical sector in Japan offers innovation and growth potential, much like tech, we see few opportunities there as much of that potential is already largely priced in.

With a strengthening economy, improved governance and stronger incentives to spend balance sheet cash, the investment case for Japan Inc looks very compelling. Particularly for those investors who can identify the companies which are best placed to capitalise on the changes and grow their business.

japanese equities at pictet asset management

Experienced team with an open culture

Our investment team has a combined 160 years' of experience and an average of 15 years at Pictet Asset Management. This gives us an understanding of Japanese companies and their management obtained through multiple business cycles. An open culture allows every team member to express their investment ideas with freedom and passion.

Decisive and resilient

We believe the key to outperformance is to act decisively when the share price moves away from its fair value and with resilience when the market tests our convictions.

Bottom-up, active approach

The Japanese Equity Selection strategy takes a focused, active approach to investing. This results in a concentrated portfolio of circa 40 large-cap stocks. The team’s style agnostic approach helps to build a resilient, diversified portfolio.

Sam Perry joined Pictet Asset Management in 1997 and is a Senior Investment Manager in the Japanese Equities team.

Sam graduated from the University of Oxford with a first class degree in Philosophy and Psychology. He holds a doctorate in Experimental Cognitive Psychology, also from the University of Oxford. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages.Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.