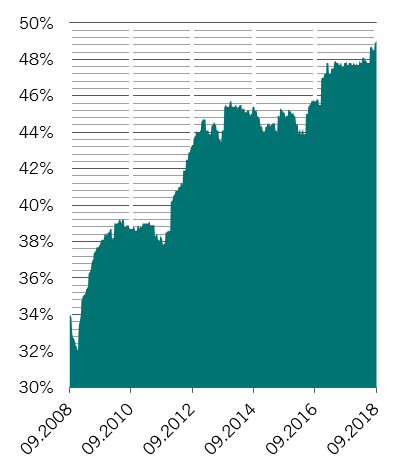

BBB-rated bond issuers - those just one notch above high-yield - now make up half the investment grade universe. That could have serious consequences in a downturn.

Written by

Shaniel Ramjee

Co-Head Multi Asset London

Supriya Menon

Senior Multi Asset Strategist

Share this article

History doesn’t always repeat itself. A profound shift in the US corporate bond market will likely make the next crisis – whenever it comes – look quite different to previous ones. Compared to previous cycles, the proportion of bonds with the lowest possible investment grade rating (IG) – BBB – is exceptionally high, having increased sharply over the past decade. BBB-rated debt now accounts for around half of the whole market in both Europe and the US (see chart).

rise off bbb

Share of BBB-rated debt in US IG universe, %

Source: ICE BofAML US Corporates Index (IG), Datastream. Data covering 19.09.2008-21.09.2018

One reason for the increase is that more firms have been turning to the credit market for funding as banks have scaled back lending in response to tougher regulations. At the same time, companies have been borrowing heavily to fund acquisitions – indeed firms operating in the telecom and consumer sectors, which have been particularly active in M&A, make up a substantial proportion of BBB-rated bonds – each sector accounts for around 8 per cent of the universe. Meanwhile, there has also been an increase in debt-funded buybacks and dividend payouts.

Consequently, today’s investment-grade bond market is, in aggregate, significantly more risky than in the past.

This is a problem because in periods when economies slow, or default rates rise, a significant proportion of BBB-rated borrowers tend to be downgraded as their finances deteriorate. This pushes them out of the investment-grade universe and down in to the high yield market. Sectors that are more defensive and have struggled to keep up with the broader pace of earnings growth would tend to be hit hardest. Portfolios which mostly or exclusively focus on investment-grade debt would therefore be forced to sell.

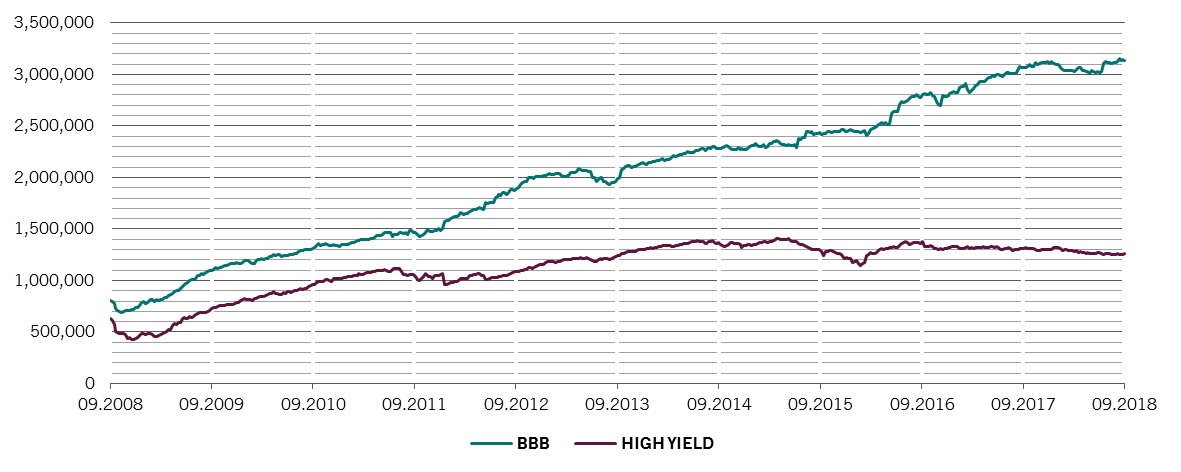

That would clearly have serious repercussions for the market as a whole. But, arguably, the impact on the high-yield segment would be even greater as that market is forced to absorb a large volume of newly-downgraded paper. During previous credit downturns, around 5-10 per cent of BBB-rated US debt was downgraded, worth around USD60-80billion on average. Based on today’s USD3.1 trillion BBB-rated market, any equivalent downturn would create at least USD 150 billion of these fallen angels. That would be a huge amount for a USD1.3 trillion high yield universe to soak up.

dominant market

ICE BofAML US credit market indices, full market value, in USD million

Source: Datasteam. Data covering 19.09.2008 – 21.09.2018.

The only way for this mass of fallen angels to be absorbed by the market at a time when liquidity conditions are likely to be strained is through price. This will also affect new issuance, as costs for borrowers rise.

Consequently, we think both investment grade and high-yield bonds are riskier than their yields currently suggest. While we do not anticipate an imminent end to the credit cycle, as it grows ever longer in the tooth ever more stresses will appear. We think the predominance of BBB-rated paper make investment-grade bonds among the least attractive parts of the debt market.

Shaniel Ramjee joined Pictet Asset Management in 2014 and is Co-Head of the Multi Asset London team.

Shaniel holds a MSc in Finance from the University of St. Andrews and a BA Hons in Economics and International Business from the University of North Carolina at Chapel Hill (US). Shaniel is a Chartered Financial Analyst (CFA) charterholder and holds the Investment Management Certificate (IMC).

In 2016, Shaniel was one of Financial News’ 40 under 40 Rising Stars in Asset Management.

About

Supriya Menon

Supriya plays a vital role in providing the Multi Asset team in London with in-depth investment research that helps steer tactical and strategic asset allocation decisions. She has built out cross-asset decision-making quantitative indicators covering valuation, fund flows and macro areas that are used across the firm. Supriya provides the Pictet Asset Management Strategic Unit with monthly Sentiment and Technical analysis and contributes to long-term thought leadership pieces.

Having joined Pictet Asset Management as a strategist in 2012, Supriya moved to the Multi Asset London team in 2018, where she assists the portfolio managers in decision-making and generates trade ideas for the balanced and multi-asset products. Supriya also communicates the team’s investment strategy to institutional clients and regularly appears on international media channels.

Supriya started her career at Morgan Stanley in 1999. She then worked as an Equity Strategist and Investment Analyst at Lehman Brothers from 2005 to 2009 after which she joined Aviva Investors as a Macro Strategist.

Supriya holds a BA in Economics and International Relations from Mount Holyoke College, Massachussets, USA and an MBA from the Harvard Business School.

Share this article

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.