Emerging Market Monitor: investing in latin america in 2019

January 2019

Marketing Material

Emerging markets - Where to find growth in 2019?

Latin America is the only EM region set to do better than last year. We look at the countries with the strongest prospects.

Written by

Anjeza Kadilli

Senior Economist

Share this article

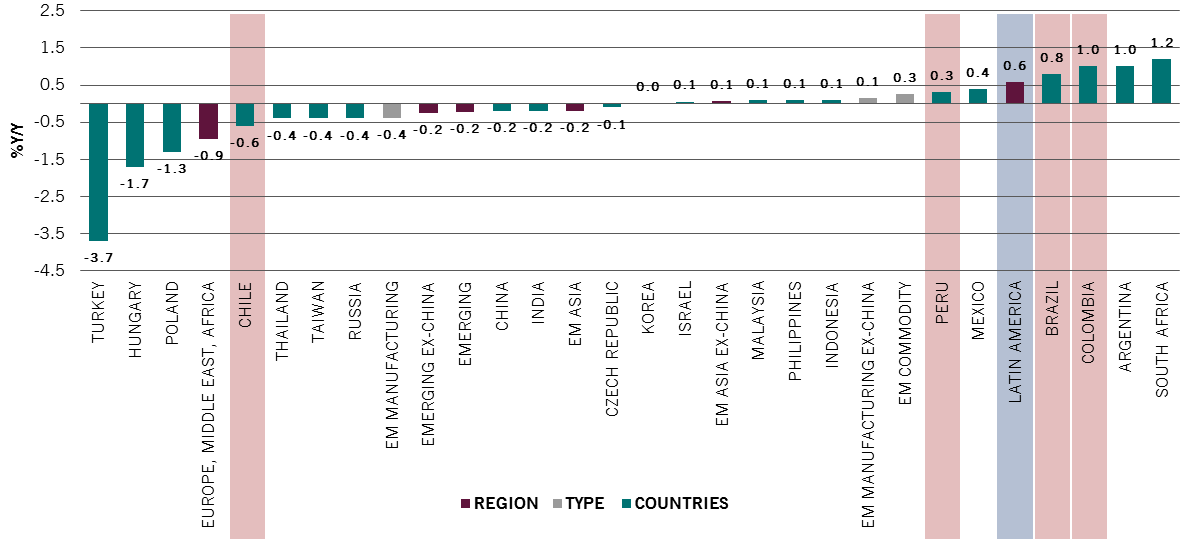

LOOK TO LATIN AMERICA FOR ECONOMIC GROWTH

Against a challenging backdrop for emerging markets, Latin America is the only region which should do better than in 2018. Brazil, Colombia and Peru in particular are the most promising markets in terms of growth acceleration (Fig.1).

Fig.1 - Relative to 2018, Latam will lead the way among Emerging Markets

Real GDP growth change: 2019 forecasts less 2018 estimates (%Y/Y)

Source: Pictet Asset Management, CEIC, Datastream, January 2019

Chile won't repeat the performance of 2018 but growth is still projected to remain strong in 2019, as illustrated by the absolute numbers in Fig.2 below.

Fig.2 - Latin American growth led by smaller, andean countries

LatAm actual & forecasted real GDP growth

Source: Pictet Asset Management, CEIC, Datastream, January 2019

In absolute terms, Latin America’s GDP growth rate in 2019 (2.6%) should outperform that of the EMEA region (2.0%), the first time since 2013.1

Inflation in the region should remain within targets, in spite of risks such as falling commodity prices, enabling policymakers to continue accommodative monetary policies.

A new period of political stability

Elections took place in all four countries between 2016 and 2018, meaning that this year should be clear of any major political instability.

The elections have led to the establishment of more conservative governments willing to reform the public sector and to stimulate the economy through long-term policies. Colombia, for instance, has reduced corporate tax. In Chile, new laws are being introduced to speed up the process of setting up new businesses. In Brazil, one of President Jair Bolsonaro’s top priorities is to cut down public spending.

CHINA'S RISING PREDOMINANCE

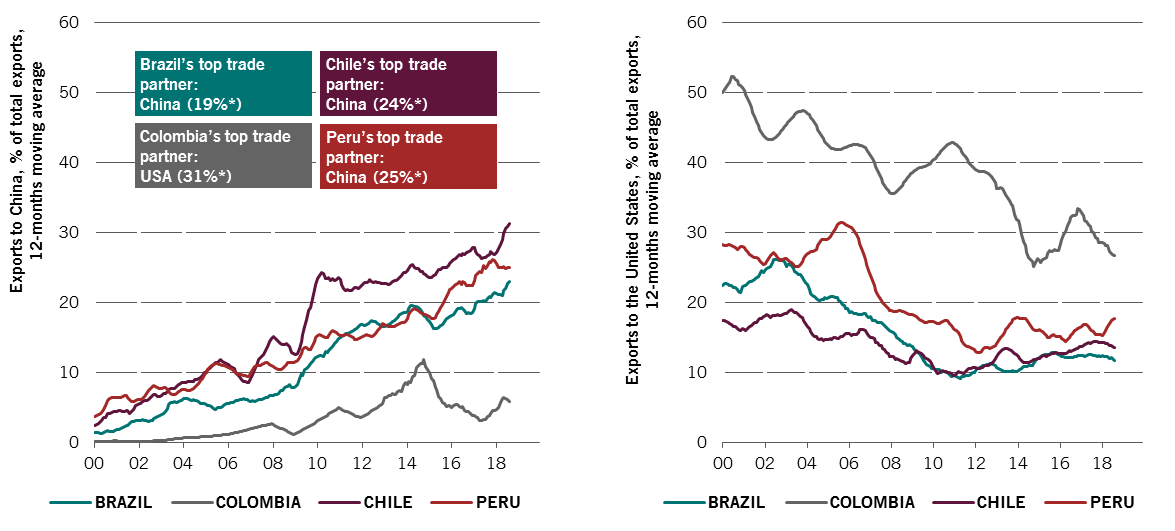

But one risk is looming for these countries: their increasing dependency on China for exports, especially in the current context of global trade tensions. As illustrated in Fig. 3 below, China is the main trade partner for Brazil, Chile and Peru.

For all four countries, albeit to a lesser extent for Colombia, exports to China have been on the rise since 2000 (Fig.3.). Over the same time period, exports to the US have slowed down, especially for Colombia (Fig.4.).

Fig.3 & 4 - Exports to China are on the rise; Exports to the US have slowed down

Fig. 3 (left) - Exports to China as share of total country's exports and top trade partners / Fig.4 (right) - Exports to the United States as share of total country's exports

Source: Pictet Asset Management, CEIC, Datastream. *Percentage of the country's total exports, based on August 2018 data available as at 31.12.2018.

China has extended its influence globally and increased imports of commodities such as metals, or cereals in the case of Brazil to satisfy domestic demand. This has allowed Latin American countries to diversify trade partners away from neighbour countries. Meanwhile the US has imported less oil as it has ramped up domestic production, impacting Colombian exports.

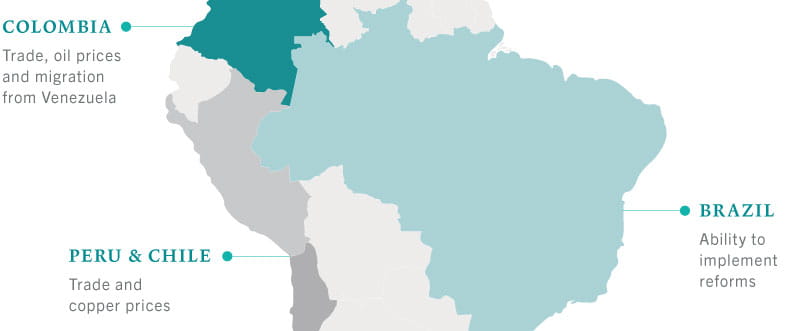

What to watch in 2019

Source: Pictet Asset Management, January 2019

In conclusion, Latin America’s economic growth should be stronger this year than in 2018, mainly driven by smaller countries such as Chile, Colombia and Peru. Brazil, the region’s largest country, will also grow, although at a more moderate pace. All of these countries have new governments in place with credible plans from an economic standpoint. Despite risks such as growing reliance on exports to China and inherent dependence on commodity prices, we believe these countries will provide opportunities for long-term investors.

CHART FROM OUR EMERGING CORPORATE BOND TEAM

By Karen Lam, Senior Client Portfolio Manager

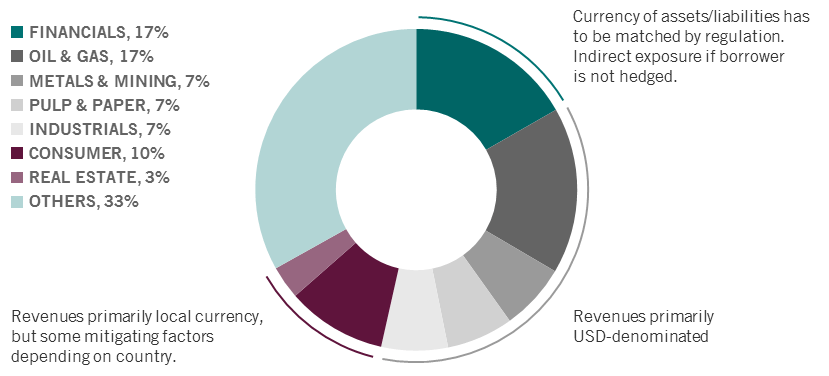

From a bottom-up perspective, we see attractive opportunities in commodity-related names. Given these are exporters, they tend to benefit from local currency depreciation. This is one of the reasons why we have given commodities a 7% overweight in our EM corporate bonds portfolio.2

Another sector that has appeal in Latin America is the pulp and paper sector, particularly in Chile and Brazil, based on relatively strong price fundamentals.

Fig.4 - In Latin America, the pulp and paper sector is a sector where we see investment opportunities

Latin America corporate hard currency bonds universe by industry and sensitivity to FX moves

Source: JP Morgan, as at 31.12.2018. Data taken from the LatAm only part of the JPM CEMBI DB index.

Anjeza Kadilli joined Pictet in 2015. She is an Senior Economist in Pictet Asset Management’s Economic Analysis team where she conducts macroeconomic analysis of emerging markets. Anjeza holds a PhD in Econometrics from the University of Geneva - where she also obtained an MSc and BSc in Economics. During her PhD, Anjeza spent time at the University of Southern California, Riksbank and HEC Montreal as a visiting scholar.

About

Karen Lam

Karen Lam joined Pictet Asset Management in 2013 as a Senior Client Portfolio Manager in the Fixed Income Emerging Corporate team and is based in London.

Prior to joining Pictet Asset Management, Karen was an Executive Director at J.P. Morgan Asset Management working as a global rates portfolio manager and later as a senior client portfolio manager covering fixed income total return strategies and emerging market debt funds. Previously, Karen was the lead manager research analyst at J.P. Morgan Private Bank covering fixed income funds.

Karen holds an MBA from the University of Chicago Booth School of Business and an MSc in Epidemiology from Imperial College London.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management. Before assuming his current position in 2009, he was head of the “Macro Research Team” at Pictet Private Wealth Management. In particular, he had economic research responsibility for emerging markets and Japan, and for the development of quantitative models on major asset classes, primarily foreign exchange models. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in econometrics from the University of Lausanne.

Share this article

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.