For non-life insurance companies, bonds are an investment staple. And for good reason. Insurers’ liabilities – current and future expected losses from claims – tend to be of short duration, between two to four years on average.

Which means the ideal return-generating, or liability-matching, asset is one that is exceptionally liquid, produces stable streams of income, and holds its capital value.

The trouble is, fixed income markets are not as dependable as they used to be.

In fact, in the decade since the US housing market crash, fixed income investors have had to abandon several of the beliefs they once held dear. It turns out, for instance, that negatively-yielding bonds are no longer an absurdity. Thanks to sustained quantitative easing, the volume of fixed income securities trading at negative yields has never fallen below USD6 trillion since 2016. (The figure leapt to as high as USD17 trillion in September last year).

Also consigned to history is the notion that developed government bond markets are oases of calm. On one eventful day in May 2018, the yield on Italy’s two-year bond spiked by more than 150 basis points, the sharpest one day sell off in more than 25 years. This was preceded by the US 'flash crash' of October 2015, which saw yields on 10-year Treasuries move up and down by 160 basis points within just 12 minutes. As the US Federal Reserve warns, such episodes will be more frequent in future as passive investing and algorithmic trading gather pace.1

(The extreme moves seen in the wake of the coronavirus outbreak -- equities and corporate bonds selling-off sharply and government bond yields dropping dramatically -- testify to this new, more volatile market climate).

Fixed income investors have had to abandon many of the beliefs they once held dear.

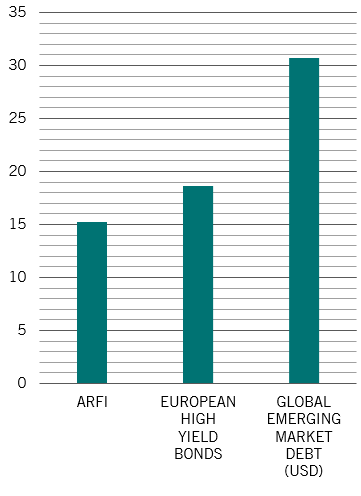

On top of wafer-thin yields and higher bond market volatility, insurance companies face an added complication. The definition of a diversified bond portfolio has also had to be torn up. That’s because the various fixed income asset classes that constitute the global bond market2 have been tracking one another more closely in recent years. The correlation of the returns of US Treasuries, corporate debt and US dollar-denominated emerging market bonds has been higher in the past three years than in the past 10.

It is unlikely that insurers can accommodate this new reality for much longer. Holding a more volatile portfolio, or one that contains a greater proportion of higher yielding but lower quality bonds, is an impractical and potentially risky option. Not least because regulations such as Solvency II have made it costly for insurance firms to hold riskier assets.

But there is an alternative to traditional bond portfolios, and comes in the form of an absolute return fixed income (ARFI) strategy.

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The NAV are available at www.beama.be.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.