[1] Since inception of the strategy on 30.11.2012 to 30.09.2017. Source: Pictet Asset Management and MSCI. Past performance is no guide to the future. The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested.

Defensive equities: a stable path to superior returns

It's possible to secure superior returns by investing in attractively-priced defensive firms that have stable profitability and a prudent approach to growth.

Written by

Laurent Nguyen

Senior Advisor

Slow and steady can win the race, as Aesop’s famous fable showed. The same can be said of equity investing. Experience tells us investors can secure superior returns over the long term by allocating capital to listed companies that have stable profitability, healthy balance sheets and trade at attractive valuations. Strangely, this is at odds with conventional wisdom.

Most investors tend to believe that gaining greater rewards requires taking on more risk. That's why they are often drawn to companies that promise rapid – and perhaps unsustainable – growth.The flipside to this behavioural bias that investors tend to underestimate the potential returns of stable, conservatively-run businesses.

Most investors tend to believe that gaining greater rewards requires taking on more risk. That's why they are often drawn to companies that promise rapid – and perhaps unsustainable – growth.The flipside to this behavioural bias that investors tend to underestimate the potential returns of stable, conservatively-run businesses.

This is precisely the kind of market anomaly that our Quest Global Equities strategy seeks to turn to its advantage. We don’t think glamour pays. We don’t think taking higher risk leads to higher return in the long run. Stocks that promise rapid growth command an unjustifiably high premium that weighs on future returns.

Instead, we believe that investors can achieve superior returns by investing in a diversified portfolio of disciplined, conservatively-run companies bought at the right price.

Preserving capital during a market sell-off has a positive influence on long-term returns.

These businesses demonstrate an ability to generate attractive shareholder returns without taking undue risks. In our view, they are likely to be more resilient to changes in the business cycle and better prepared to face economic downturns.

Unearthing these companies demands comprehensive analysis. Our approach is to take a 360-degree view. We look at a number of business characteristics that combine to lend an equity investment a genuinely defensive profile. It's an approach that is different from many defensive equity strategies, which tend to focus on just one factor, such as stock volatility.

We also recognise, however, that there are times when certain types of defensive stocks trade at an excessive premium. This is why we constantly monitor and assess the valuation of individual defensive attributes and shift our investments accordingly. It's an approach that can deliver over the long run.

While defensive stocks tend to lag in the early stage of a market rally, they typically fall less, sometimes far less, than mainstream equity investments during a decline. Preserving capital during a market sell-off has a positive influence on long-term returns. Because of the compounding effect, the defensive stocks we invest in should outperform the MSCI World Index over the course of a market cycle, both in absolute terms and when adjusted for volatility. What is more, these stocks are more attractive than typical low-volatility stocks as they tend to fall less during a downturn and rise more in up markets.

Unearthing defensive companies

Traditionally, investing in defensive equities meant focusing on companies with very specific attributes, such as those whose shares exhibit low volatility or that pay higher-than-average dividends. But single factor strategies can be vulnerable to shifts in the economic and financial cycle. Some can become crowded, expensive investments. Others are vulnerable to sudden changes in macroeconomic conditions, such as higher interest rates.

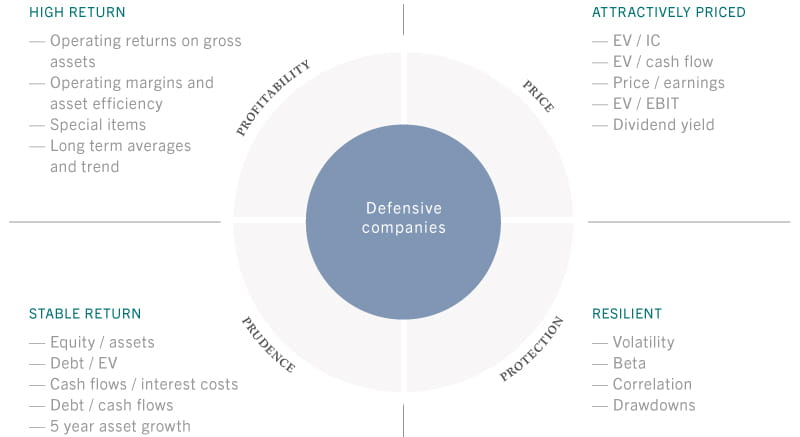

Recognising these problems, we have developed a proprietary multi-dimensional framework that focuses on four key determinants of defensiveness – profitability, prudence, protection and price – what we call our “4P” framework. It provides a lens through which we identify companies that satisfy our comprehensive defensive criteria out of a vast universe.

4P, a multi-dimensional framework

Source: Pictet Asset Management

The Profitability score helps us gauge a business's strengths and competitive advantage. Companies that rank highly on this measure have steady earnings growth, low operational leverage and high cash generation. We find that companies with a strong track record of profitability tend to have more reliable and predictable earnings than firms whose stock valuations are in part based on lofty expectations for profit growth.

Prudence is our gauge for assessing a company’s operational and financial risks. Prudent companies have a lower risk of default and expand their business organically. We invest in businesses that can create and preserve shareholder value by pursuing manageable growth and maintaining a sound financial profile. We measure this by looking at the nature and stability of the company’s cash flows relative to its financial commitments, including interest, dividend or capital spending.

We integrate environmental, social and governance (ESG) aspects in the entire research and investment process with a view to enhance returns. It also serves as an additional layer of prudence.

With the Protection metric we scrutinise how a company behaves over the course of the economic cycle in order to monitor systematic or firm-specific risks. We are looking for companies that have sustainable business models and whose prospects are insensitive to shifts in economic cycles. At the same time, we also analyse a stock’s volatility and its correlation with other equities to understand how it might affect the risk-return profile of the overall portfolio.

Finally, we don’t want to overpay for our investments. Therefore, our Price screen incorporates several reliable valuation models that help us identify the most attractively-priced stocks. Without this screen, portfolio managers could overlook promising investments or choose stocks that risk a capital loss.

The 4P framework is the cornerstone of our investment process. We combine the 4P-based systematic screening with a bottom-up fundamental analysis to identify the best investment ideas and build a portfolio of around 150 companies.

As a result of the 4P approach, our portfolio has variable factor and style exposures, encompassing large cap, quality, value and minimum volatility stocks.

Dynamic, not static

Our starting point is to evenly weight all the 4Ps when we screen stocks. But we make active and tactical weighting changes, based on our analysis of the momentum and valuation of each P, judged against our assessment of current and future macroeconomic and market conditions. We believe this dynamic adjustment protects investors from being over- or under-exposed to any one defensive factor. This, in turn, helps maximise returns.

Here’s an example. In the run up to the British referendum on the European Union membership in June 2016, stock markets were jittery. Investors were largely eschewing higher-growth equities in favour of more defensive sectors such as utilities.

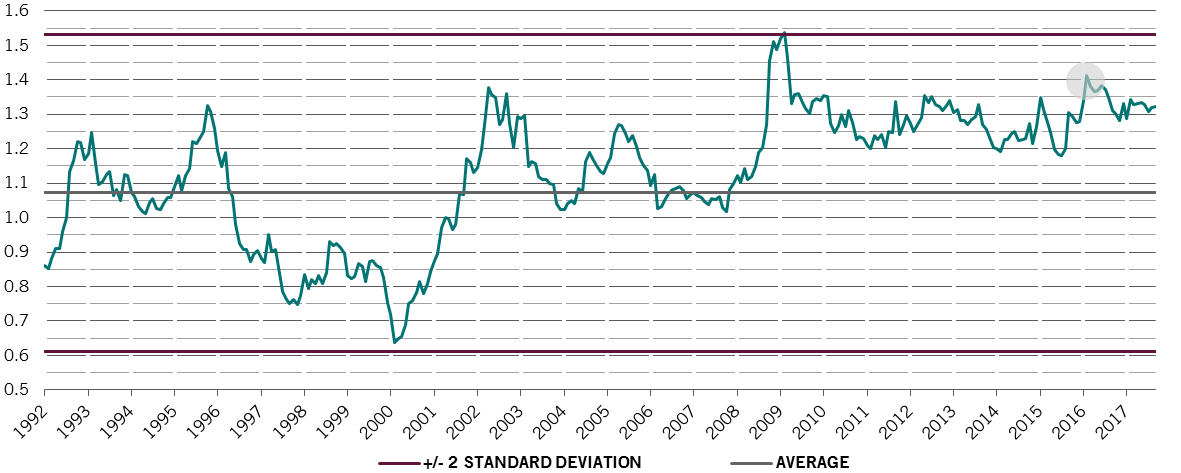

As a consequence, stocks that scored best on Protection in our framework saw an exceptionally strong pre-Brexit rally – so strong, in fact, that they quickly became among the most expensive equities investors could buy. Specifically, our analysis showed that such companies’ price-to-book ratios were some 40 per cent higher than that of the average listed firm – the second biggest gap in 24 years (see chart).

Protection goes to the extreme

Relative valuation, measured by price to book ratio, of companies that rank in the top quartile of the Protection score

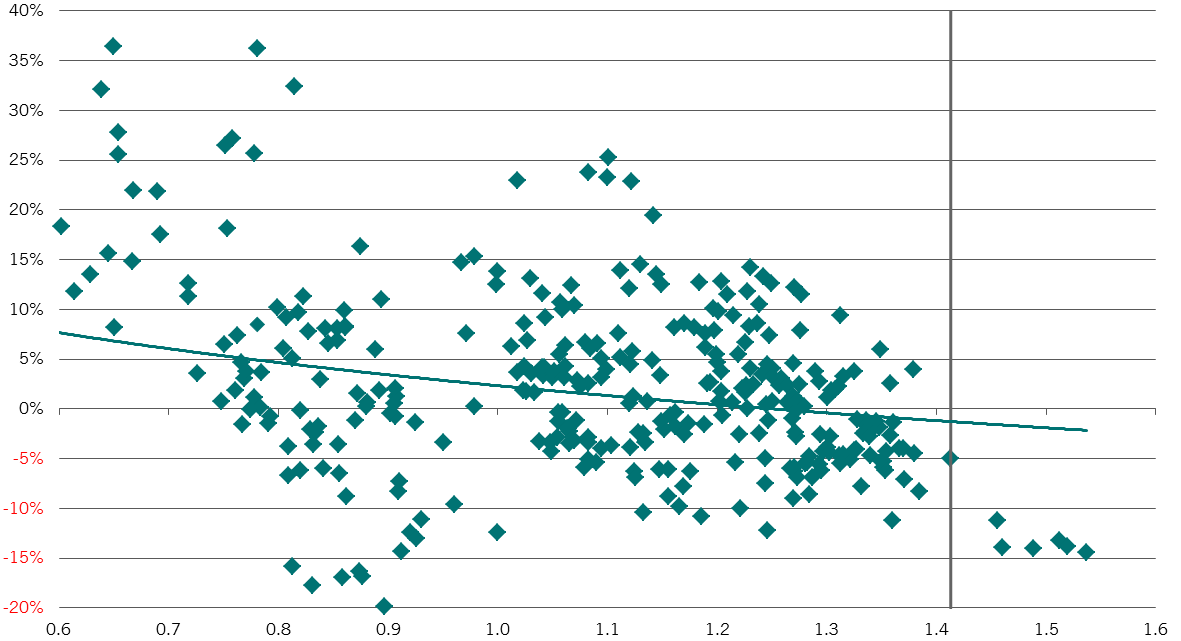

To us, this was a warning sign. Our research showed that when buying Protection becomes this expensive, it can act as a drag on future returns (see chart). We therefore downgraded the Protection weighting to 15 per cent from 25, while upgrading the Price weighting to 35 per cent.

Overvaluation leads to underperformance

One-year subsequent relative performance (%) of top Protection companies based on their month-end price to book ratios relative to market average

The tactical move proved beneficial. In the second half of 2016, a pure Protection portfolio – one consisting exclusively of stocks that scored highest on this metric – would have had a negative active performance of -7.1 per cent while a pure Price portfolio would have outperformed the MSCI World index by about 8.4 per cent.

Had the 4P weighting remained static, investors may have been left overexposed to this expensive Protection element and suffered a loss, which was the case for those in most low volatility funds. For instance, the MSCI World Minimum Volatility Index lost more than 9 per cent relative to the MSCI World in the second half of 2016.

Through this dynamic weighting of the 4P framework and our bottom-up stock analysis, we aim to outperform the MSCI World index over a full market cycle – which usually lasts about five to seven years – by 3 per cent gross of fees on an annualised basis.

In the past five years, our strategy had a lower volatility than the benchmark, while its upside/downside beta was an asymmetric 90 to 73 per cent. This means that on average the strategy captured 90 per cent of a market rally, while suffering only 73 per cent of a sell-off.1

We think our Quest Global Equities strategy can be a key pillar of a global equity allocation. It also helps diversify an existing equity portfolio thanks to it distinctive return profile.

Overcoming biases for long-term return

Behavioural biases are hard to break. Investors chase cyclical and glamourous companies which promise rapid growth, and systematically under-appreciate defensive and stable companies that are attractively-priced.

But biases can hold investors back. We think by choosing these companies with a rounded defensive profile investors can get ahead of the market and achieve sustainable return in the long term.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.