As global equity markets turn more volatile long/short equity strategies can help investors to continue generating attractive returns.

Written by

Steve Huguenin-Virchaux

Head of TR Equities Client Portfolio Managers

Share this article

Global equity markets appear to be at an inflection point. Economic growth is plateauing, interest rates are rising and valuations look stretched. As a result, after nearly a decade of unusually benign conditions, there are signs that markets are returning back to more “normal” behaviour. That could mean higher volatility and lower returns from mainstream stock markets in future.

That’s an environment for which the long/short (L/S) equity investment approach was designed. Such strategies aim to match the returns of markets when they are rising but preserve capital when the investment climate turns sour. They can do this because they can take both long and short positions in securities. In other words, they can invest in companies with the strongest growth prospects and also establish short positions in firms deemed to be suffering a long-term decline in profitability.

The ability of an L/S strategy to mitigate volatility and limit the scale of losses is particularly important. The power of compounded returns means that, for example, a 25 per cent decline in the value of investments requires a subsequent 33 per cent rally to fully recover ground.

In recent years, the ability to do this was arguably less necessary given both the unusually high returns equities generated and the relative calm of the market.

Artificially low interest rates along with quantitative easing on a massive scale kept a lid on stock market volatility, creating the conditions for individual stocks to move up more or less in lockstep with one another.

But we saw the value of the L/S approach emerge at the start of 2018. In February this year, the S&P 500 suffered a peak to trough drop of more than 10 per cent, while the HFRX Equity Hedge Index – which aggregates the performance of long/short strategies – lost only 3.7 per cent.

We believe February’s market slump could be an indicator of the kind of volatility that could ensure as markets revert to type.

Historically, in such times of turbulence, investors have dialled down their equity exposure and turned to bonds. But today that strategy is less likely to work: bonds appear to have lost some of their diversification benefits, tending to both rise and correct in unison with equities in recent years.

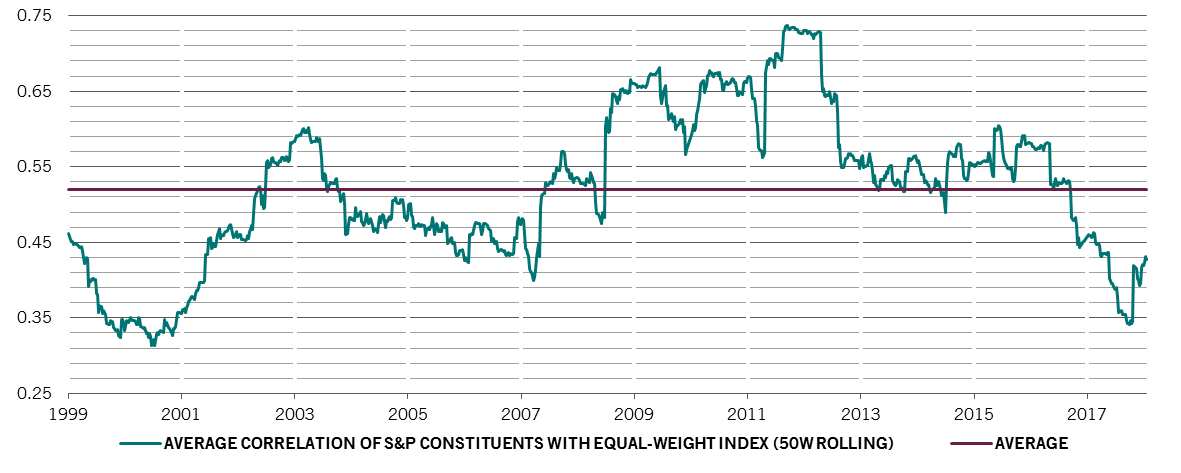

In contrast, the correlation of the returns of the individual stocks that make up the S&P 500 index is at one of the lowest levels of the past two decades (see chart). In Europe, although slightly higher, the correlation has also gone down to reach levels not seen for many years. That is a potentially fertile environment for stock pickers – particularly for long/short managers, who have the ability to generate returns from both strong and the weak performers.

opportunities in divergence

Correlation of S&P 500 constituents with the index, compared to the long-run average

We believe that as central banks withdraw monetary stimulus, this period of higher dispersion is set to continue. And as the era of cheap financing comes to an end, corporate fundamentals will diverge: companies with poor management, flawed business models or low margins will find it harder to stay afloat, which in turn will create more short-selling opportunities.

Long/short managers will thus be able to make full use of their bottom-up analysis and stock picking skills, generating excess returns from both potential winners and losers.

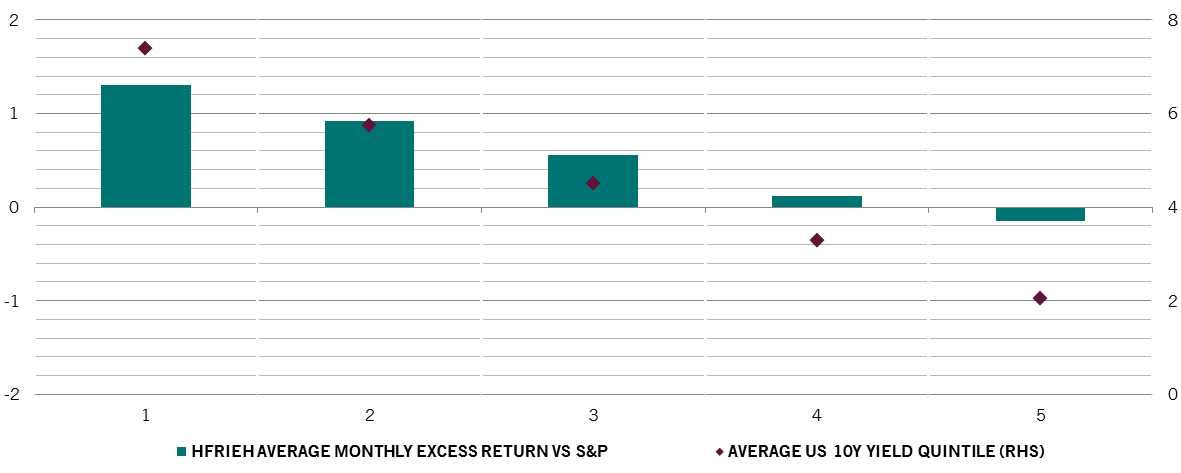

Historically, equity long/short managers have tended to secure greater average monthly excess returns over the market during periods of higher interest rates and higher bond yields as highlighted in the chart below. For instance when the 10 year Treasury yield reached its highest level (first quintile), the average monthly excess return of the HFRI Equity Hedge Index relative to the S&P 500 TR Index also scaled a peak.

hand-in-hand with bond yields

Average monthly excess returns for long/short equities versus S&P 500 stocks during instances when 10 year Treasury yields are rising

Average monthly excess return of the HFRI Equity Hedge Index in USD relative to S&P 500 Total Return Index assuming a beta of 0.45 between the 2 indices. Source: Bloomberg, Pictet Asset Management. Data covering period: 31.12.1989-30.04.2018.

We believe that hedge fund strategies can play one of two roles in a portfolio: they can serve as substitutes or diversifiers. L/S equity strategies can be a substitute for some or all of a long equity allocation and improve its risk-return profile.

Our research also shows that during the two major bear markets of the past 20 years – January 1999 to September 2002 and October 2007 to February 2009 – long/short equity funds offered investors a far greater degree of capital protection.

What’s more, unlike some other diversifying asset classes – such as real estate or private equity – long/short equity portfolios invest in liquid instruments. And investors can be further protected by the fact that Europe’s UCITS mutual funds framework, which lends itself well to L/S equity strategies, offers great transparency and regulatory oversight.

Overall, then, we believe that current market conditions require a more agile approach to equity investing. Including long/short equities as part of a broader portfolio allocation to stock markets can offer a degree of downside protection – insurance that’s likely to become even more important as markets become more bumpy.

About

Steve Huguenin-Virchaux

Steve Huguenin-Virchaux joined Pictet Asset Management in 2008 and is Head of Total Return Equities Client Portfolio Managers & Business Strategy. He also serves as Board member for Pictet AM Offshore Hedge Funds.

Prior to joining Pictet, he worked for Heritage Fund Management, where he was responsible for business development and investor relations for Hedge Fund strategies. Before that, he worked at Capital International, initially as a senior portfolio administrator and later transitioning to the Clients Relations Department.

Steve holds a Master’s degree in International Relations from the Graduate Institute of International and Development Studies in Geneva and also obtained the Certificate of Quantitative Portfolio Management from the University of Geneva.

He is a Chartered Financial Analyst (CFA) charterholder and a Certified Investment Fund Director (CIFD).

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.