Asian fixed income: introduction

Never waste a good crisis.

If there’s one region in the world that has followed this advice to the letter, it is Asia.

Two decades after the region’s currency crash, Asian economies have thrived, profiting from institutional, regulatory and capital market reforms that have boosted the bloc’s international competitiveness.

Emerging Asia is now the world’s fastest growing region, with its economy expanding at just over 6 per cent per year1. It is thanks to these strong fundamentals that Asian bond markets are becoming deeper and more diverse, and a magnet for a growing number of domestic and international investors.

Boasting attractive yields and low volatility, the region’s bonds deserve to be a strategic holding for those seeking both decent levels of income and diversification.

Overview: rich Asian offering

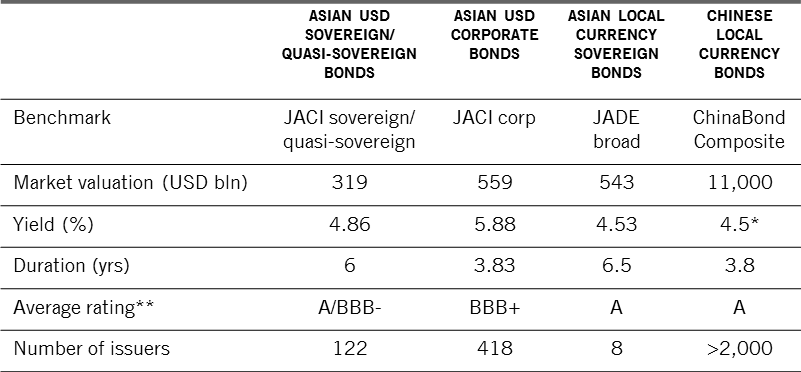

Investors can choose from four sub asset classes within the Asian bond universe: government bonds denominated in local currency or the US dollar, corporate bonds and Chinese onshore debt denominated in the renminbi (RMB) (see chart).

* yield to maturity ** S&P ratings

Source: JP Morgan, ChinaBond. Yield, duration and average rating for Chinese local currency bonds are represented by averages for Pictet-Chinese Local Currency Debt portfolio. Data as of 30.06.2018

- Asian local currency sovereign debt: these instruments are most sensitive to changes in domestic macroeconomic conditions; this market is suited for investors who want to benefit from long-term growth of Asian economies as well as the long-term appreciation potential of Asian currencies. There is also the prospect for local sovereign debt to develop into a defensive asset class over time, as US Treasuries or Japanese Government Bonds have done.

- Asian USD sovereign debt: this dollar-denominated universe allows investors to profit from strong Asian economic fundamentals but without the currency exposure. Investors in this type of bonds should be able to benefit from the likely improvement in the credit profile of the issuers, which should become the primary source of capital gain in the long term.

- Asian USD corporate bonds: this asset class is composed of highly rated instruments; nearly 70 per cent of issuers have a rating of BBB and above. That compares with just 54 per cent for the broader emerging debt market. Most issuers are in a stronger position to service and repay their debt than their peers in other regions, thanks to sizeable cash cushions and low debt. The net debt-to-EBITDA ratio of Asian corporations stands at around 1.7 times, compared with 2.1 times for the emerging world and 2.8 times for the US. What is more, Asian credit should develop into an even richer source of investment opportunities as locally-based companies increasingly switch away from short-term bank loans to longer-term debt financing.

- Chinese onshore debt: Already the world’s third largest bond market, RMB-denominated bonds are growing fast thanks to their attractive yields and because they offer exposure to a currency with potential for strong appreciation. Up until recently, Chinese onshore bonds have been excluded from the flagship EM and global bond indices, but that looks set to change soon. Beijing’s measures to liberalise the capital market should help China’s case for inclusion in major global bond indices, which could generate as much as USD286 billion of fresh inflows into the asset class. What is more, we expect the RMB to evolve into a major international currency over the coming years, which should help attract overseas demand for Chinese assets and boost the value of the currency in the long-run.

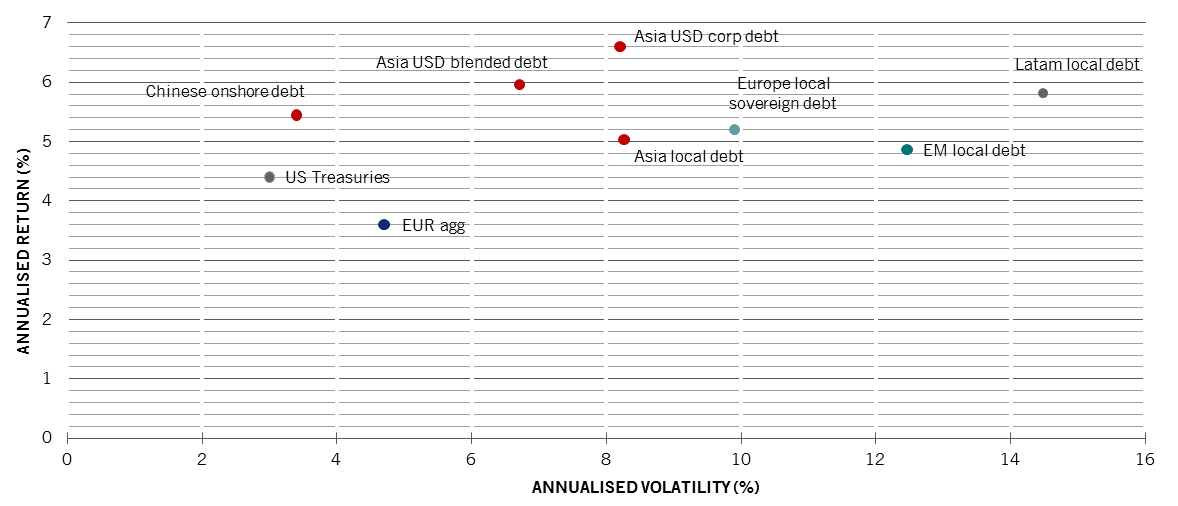

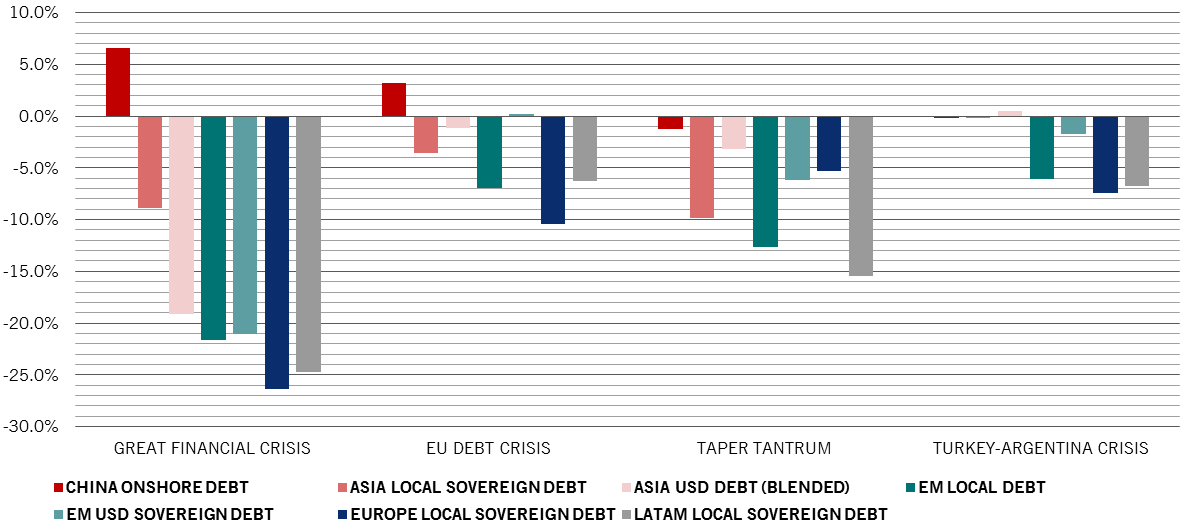

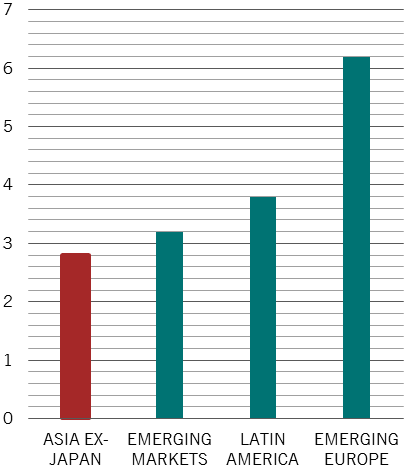

All four instruments tend to enjoy better volatility-adjusted returns than many of their EM (emerging market) and DM (developed market) counterparts (see chart).