Asset allocation: chips off the table

As 2018 draws to a close, there are many reasons for investors to tread carefully. Even though the US Federal Reserve chairman Jerome Powell made an unexpectedly dovish speech at the end of the month, potential stumbling blocks for financial markets abound. These include global trade tensions, Brexit, and Italy-inspired political upheaval in the euro zone.

At the same time, the outlook for the global economy has darkened a shade, liquidity conditions continue to deteriorate and technical indicators are flashing red for many of the major asset classes.

There are, of course, attractive investment opportunities still to be found, particularly after recent market turbulence. But, on balance, we think that the mix of uncertainty about the future and the tough conditions in the present merit a reduction in our exposure to riskier asset classes. We have therefore decided to reduce our equity stance to neutral and upgrade bonds to neutral.

Our business cycle readings have deteriorated for the US, Japan and Switzerland compared to last month. Leading indicators now show neutral or negative economic scores in virtually all regions. The only exception is China, where government stimulus is starting to filter through into more infrastructure spending and retail sales excluding cars are holding up well.

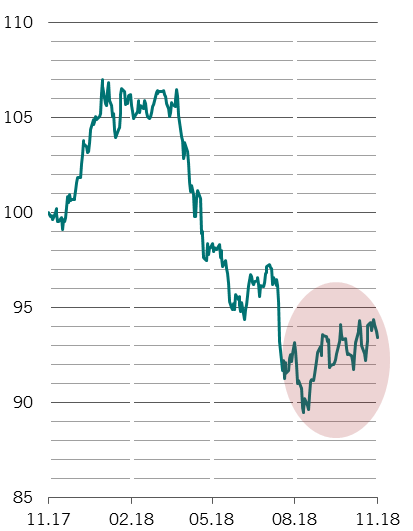

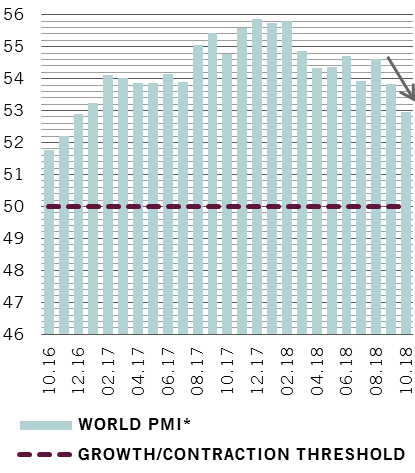

For the world as a whole though, business sentiment is at its gloomiest in two years, according IHS Markit data. The latest surveys imply the world economy will grow by less than 3 per cent next year, which suggests that consensus expectations will have to be scaled back.

World PMI

A particular area of concern is the US housing sector, where activity has slowed markedly, price inflation peaked in the first quarter and 30-year mortgage rates have risen to 5 per cent from a low of under 3.5 per cent in 2016.

Partly to blame is a sharp contraction in liquidity. Over the past 12 months, the volume of credit made available by central and private banks as proportion of nominal GDP in the US, China, the euro zone Japan and UK is has halved to a level equivalent to just 8.3 per cent1.

For the first time since the global financial crisis, we expect that these five major central banks will, on aggregate, be selling down their holdings of the financial assets they accumulated under quantitative easing. And this will have a negative impact on the business cycle, particularly in the US, in the more interest-rate sensitive sectors of the economy, including business investment.

Technical indicators add to the case for caution, with the picture for cyclical equity sectors particularly uninspiring. Meanwhile gold – a traditional safe haven – looks heavily oversold, which could accentuate any price gains should investors become more risk averse.

Valuations support our neutral stance on global equities, which now look neither especially expensive nor cheap: the 12-month forward price-to-earnings ratio for the benchmark MSCI ACWI index is at what we consider to be a reasonable 13.7. Bonds remain expensive in aggregate, although that hides pockets of value, particularly in emerging market local debt.