Emerging Market Monitor - Inflation in Central & Eastern Europe

Inflation across emerging markets is at multi-decade lows. But one region is bucking the overall trend: Central & Eastern Europe. What does it mean for investors?

Written by

Patrick Zweifel

Chief Economist

Nikolay Markov

Senior Economist

Share this article

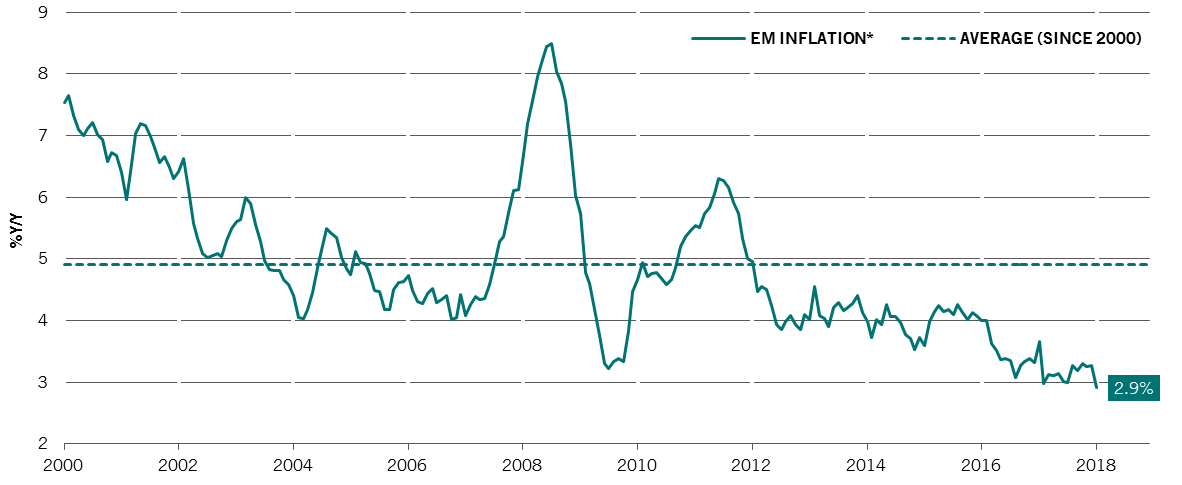

First, some global observations about inflation. Average inflation across emerging markets has fallen to 2.9%, a level not seen since the 1970s, and this is good news for holders of hard currency debt.

FIG. 1 inflation in EMerging markets

Source: Pictet Asset Management, CEIC, Datastream, February 2018. *Based on 30 EM consumer prices indices, GDP weighted.

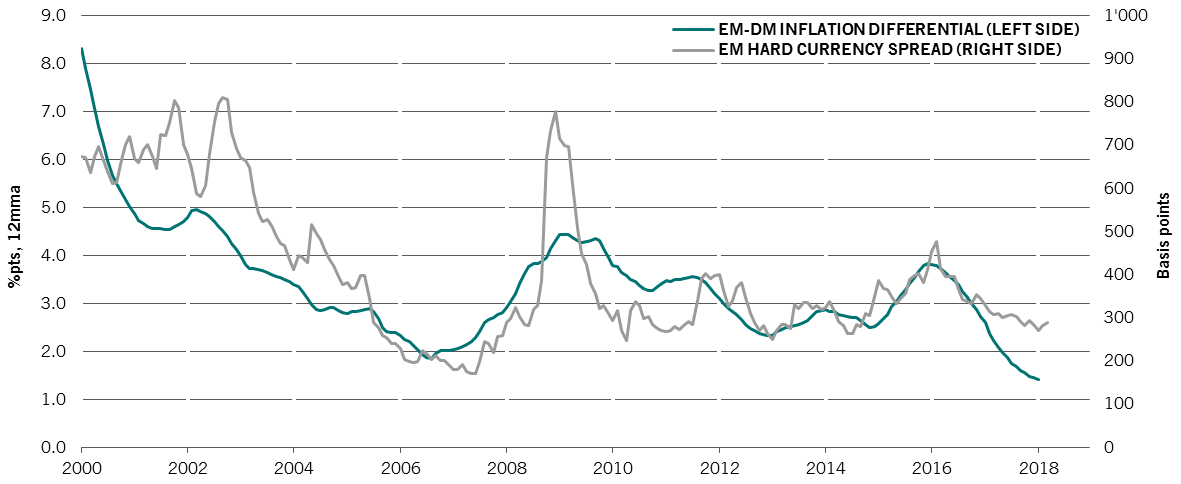

As Fig. 2 below shows, the inflation differential between developed and emerging markets and EM hard currency yield spreads appear closely linked. Even if inflation is expected to pick up modestly in emerging markets, we believe it will rise less than in developed markets, and this supports a further narrowing in emerging hard currency debt spreads.

Fig. 2 - INflation differential

Source: Pictet Asset Management, CEIC, Datastream, January 2018

The exception to the rule...

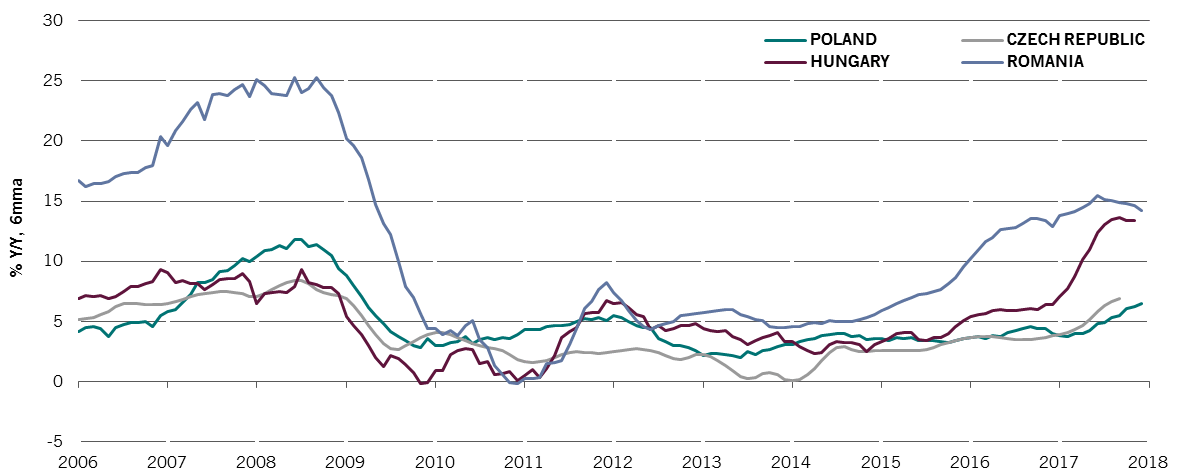

As mentioned, one cluster of countries bucking the falling inflation trend is the Central and Eastern Europe (CEE) markets of the Czech Republic, Hungary, Poland and Romania. This is mainly because of wage growth, which has ticked up in all four countries.

Fig. 3 - Nominal wage growth in the CEE region

Source: Pictet Asset Management, CEIC, Datastream, February 2018

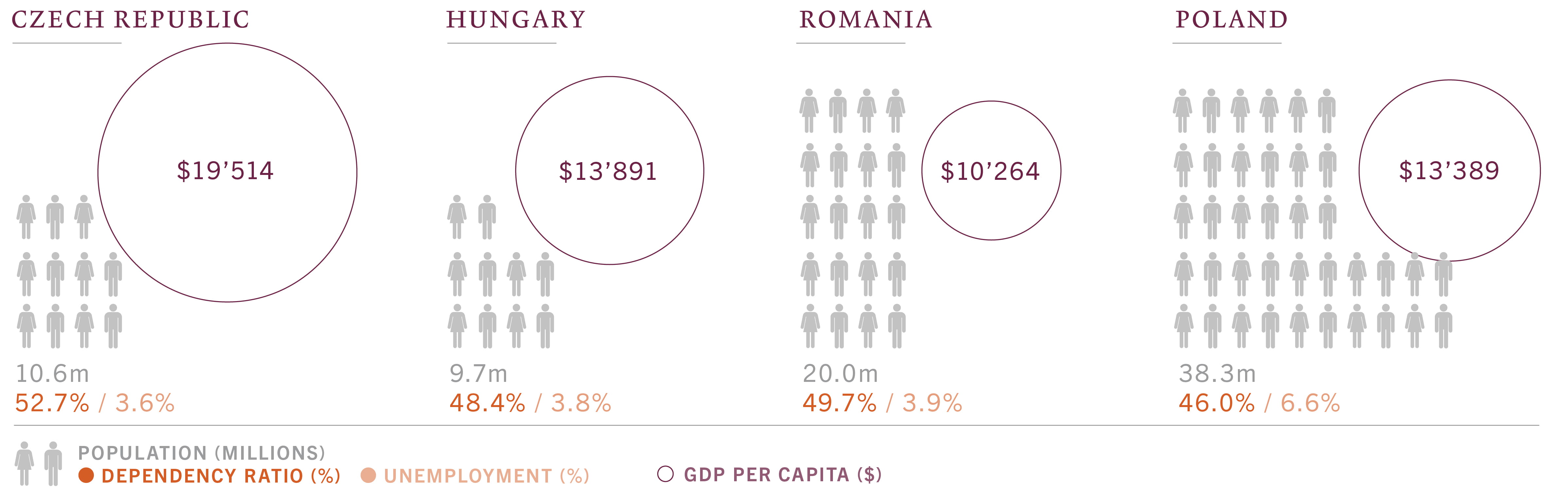

The four markets in the CEE region account for over a trillion dollars of GDP and around 80 million people. Poland is the region’s powerhouse accounting for half of GDP and half of the population. The richest market in terms of GDP per capita is the Czech Republic.

fig. 4 -THE CEE REGION AT A GLANCE

Population, dependency ratios, unemployment and GDP per capita

Source: Pictet Asset Management, CEIC, Datastream

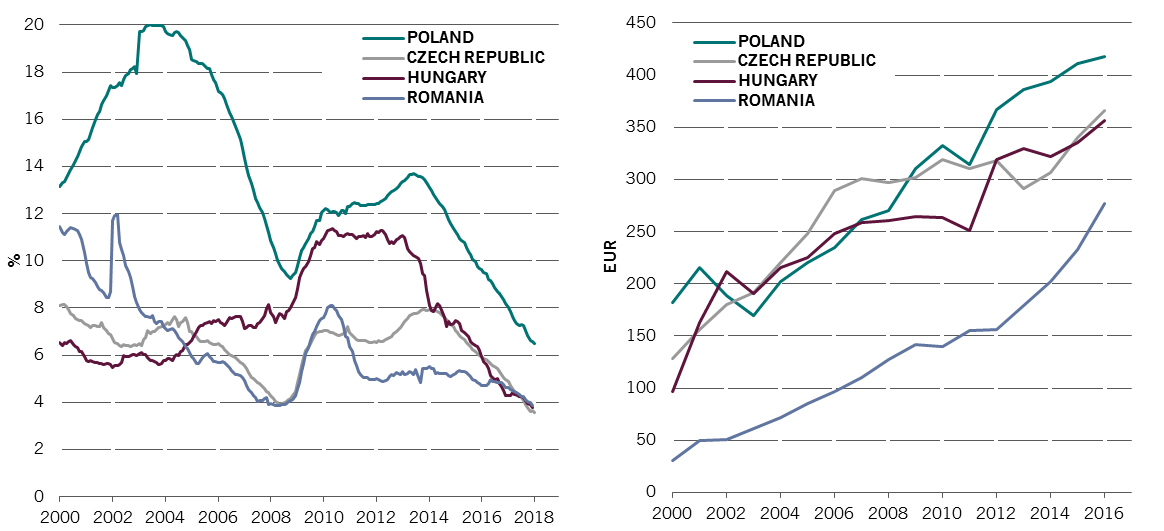

The charts below show two key drivers of wage increases in these four economies: record-low unemployment and increasing minimum wages.

Figs. 5a & 5b -

Left chart - Central Eastern Europe unemployment rates (%) Right chart - Central Eastern Europe minimum nominal monthly wages (EUR)

Source: Pictet Asset Management, CEIC, Datastream, February 2018

You can depend on us...

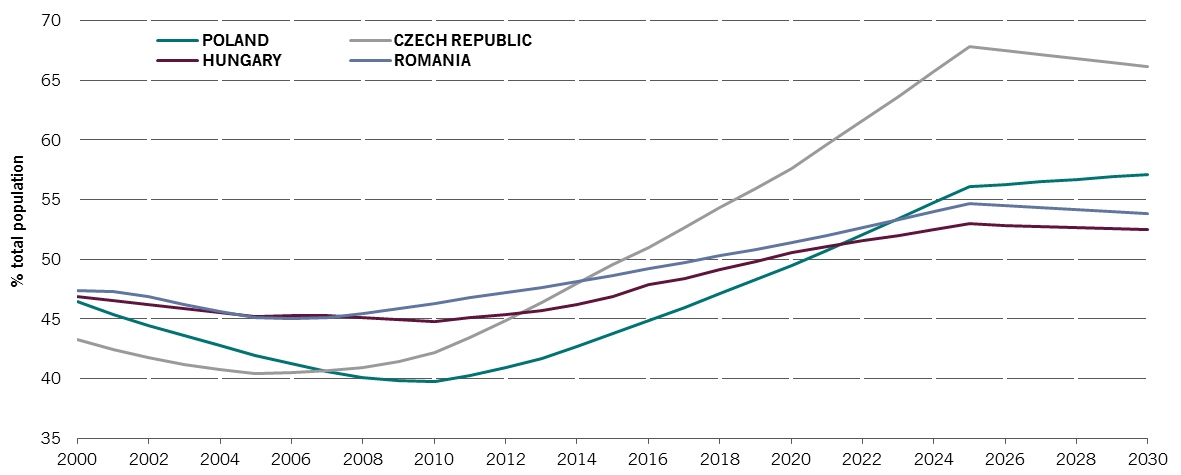

Wage pressure could continue to build in the CEE region as ageing populations and rising life expectancy cause the dependency ratio of non-working to working people to rise across all markets. As Fig. 6 shows this is especially the case for the Czech Republic.

FIg. 6 - RISING Dependency ratios

Dependency ratio is the percentage of population outside of working age: 0-14 year, 65 years +

Source: Pictet Asset Management, CEIC, Datastream, January 2018

Central banks behind the curve

What does this mean for debt investors? Although rising wage growth in the CEE is a sign of strong economic conditions, the risk of central banks falling behind the curve is a threat for the region’s local currency debt.

Overall CEE central banks have been slow to react to inflation. Poland and Hungary in particular have not started the tightening yet. The Czech National Bank was first to hike rates after the removal of the EUR/CZK floor in April 2017.

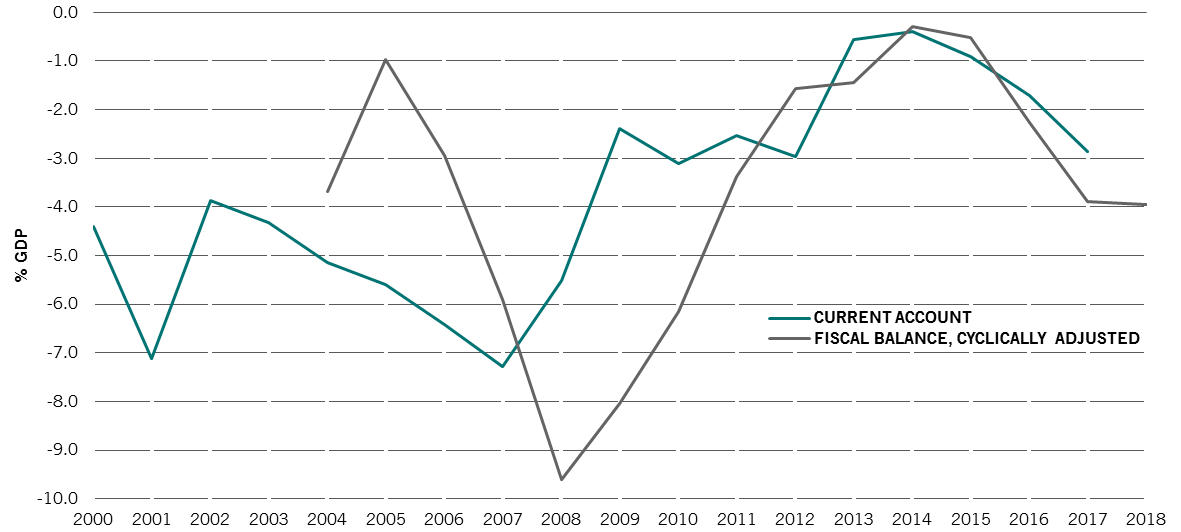

FIG. 7 - TWIN PEAKS - ROMANIA MOST AT RISK

Romania's current account and fiscal balance (% GDP)

Source: Pictet Asset Management, CEIC, Datastream. Current account January 2017, fiscal balance January 2018.

Although the Bank of Romania began hiking rates in February 2018, we believe the country is the most at risk. As Fig 7 shows it is the only market in the region with a ‘twin deficit’ – trade and current account - which is deteriorating. We believe this increases the pressure on CPI inflation through an expected depreciation of the currency, in addition to the rising domestic inflationary pressures. We expect a more rapid pace of rate increases in the year ahead.

THE VIEW FROM OUR EMERGING MARKET EQUITY TEAM

By Christopher Bannon, Senior Investment Manager

Christmas decorations in Vaci Street, Budapest, Hungary

Backing the consumer boom

The CEE region is booming. In our view this is best captured through stocks exposed to consumption and credit, such as banks and consumer companies backed up by strong fundamentals.

Valuations here look reasonable, trading at a slight discount to western European markets. In addition, we believe that forward expectations do reflect strong macro growth dynamics.

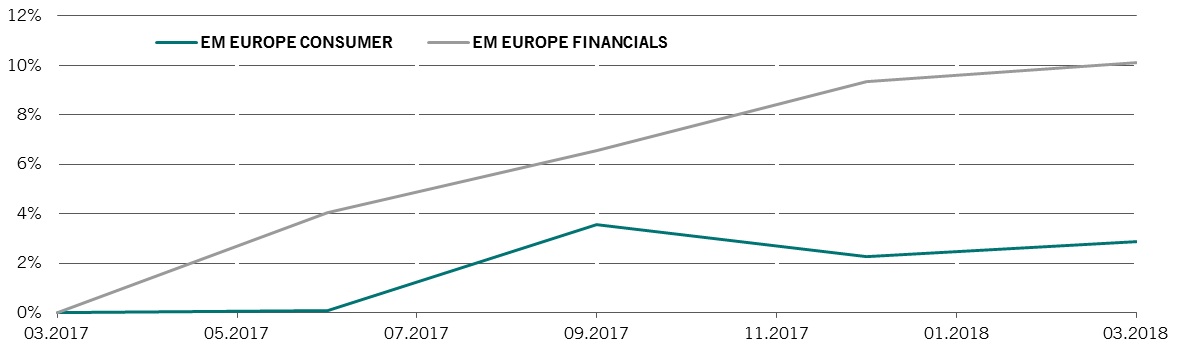

Fig 8. Upside in Consumer and financials

Change to 2019 net income expectations

Source: Bloomberg, March 2018

As Fig. 8 shows, both financial services and consumer sectors have seen their earnings forecasts upgraded quite consistently over the past year.

Despite the overall positive trend, the market has been paying greater attention to company fundamentals and rewarding those with the strongest growth prospects. In our view, the increasing dispersion of returns between the market's winners and losers is creating a fertile ground for stock pickers.

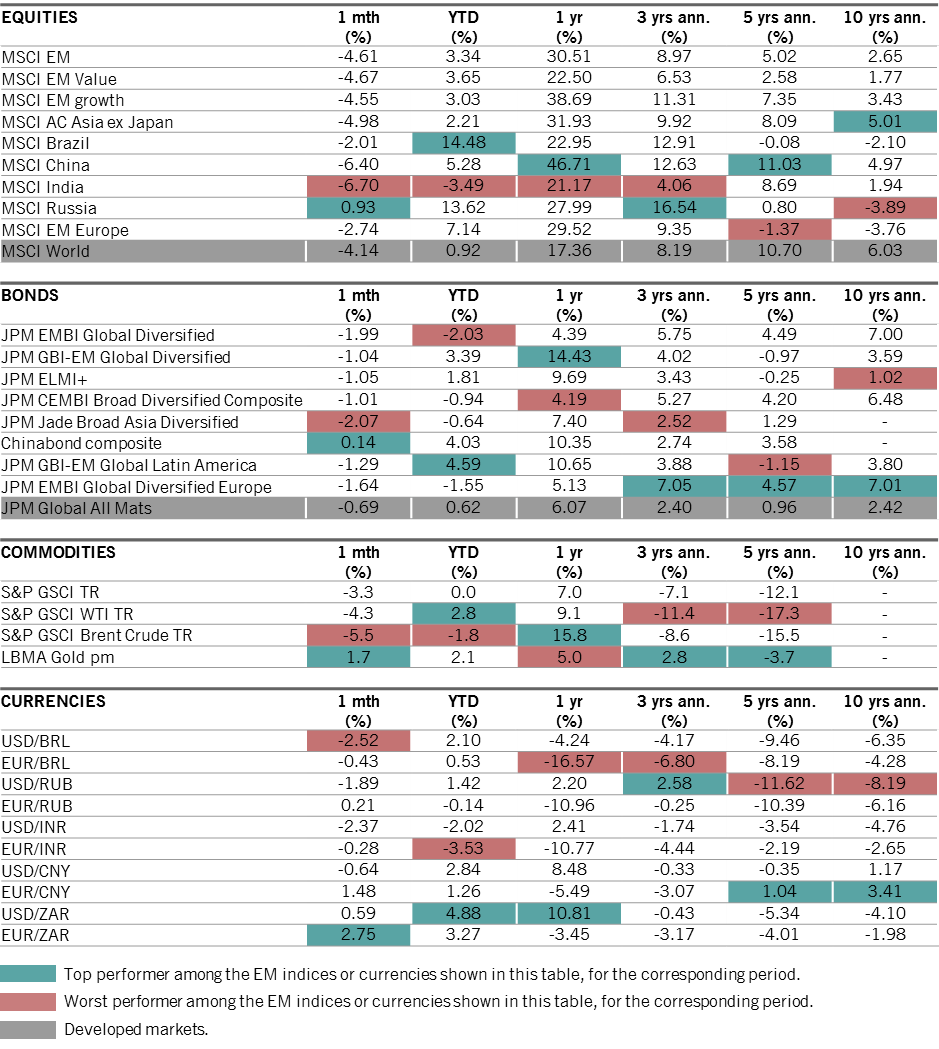

MARKET WATCH

MARKET WATCH DATA

28.02.2018

Source: Datastream, Bloomberg, data as at 28.02.2018 and in USD. Equity indices are quoted on a net dividend reinvested basis; bond and commodity indices are quoted on a total return basis. The currency rates evolution is treated as a performance calculation based on FX rates.

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Christopher Bannon

Christopher Bannon joined Pictet Asset Management in 2007 and is a Senior Investment Manager in the Emerging Markets Equities team, specialising in Emerging Europe and Russia.

Christopher joined Pictet in 2007, initially as a risk manager before moving across to the Emerging Equities Research team in 2011 specialising in the energy sector across global emerging markets. Christopher started his career in 2005 with Citigroup, where he spent 18 months on the corporate actions desk.

Christopher graduated from Trinity College Dublin with a BA (Hons) in Mathematics and Philosophy and he holds an MSc in Finance (graduated with Distinction) from Imperial College London. He is also a Chartered Financial Analyst (CFA) charterholder.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management. Before assuming his current position in 2009, he was head of the “Macro Research Team” at Pictet Private Wealth Management. In particular, he had economic research responsibility for emerging markets and Japan, and for the development of quantitative models on major asset classes, primarily foreign exchange models. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in econometrics from the University of Lausanne.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.