A tale of two emerging market crises

Argentina and Turkey have been at the heart of the recent sell-off. Investors should look to policymakers and governments for clues as to where these markets are headed.

Written by

Anjeza Kadilli

Senior Economist

Nikolay Markov

Senior Economist

Debt not the main issue

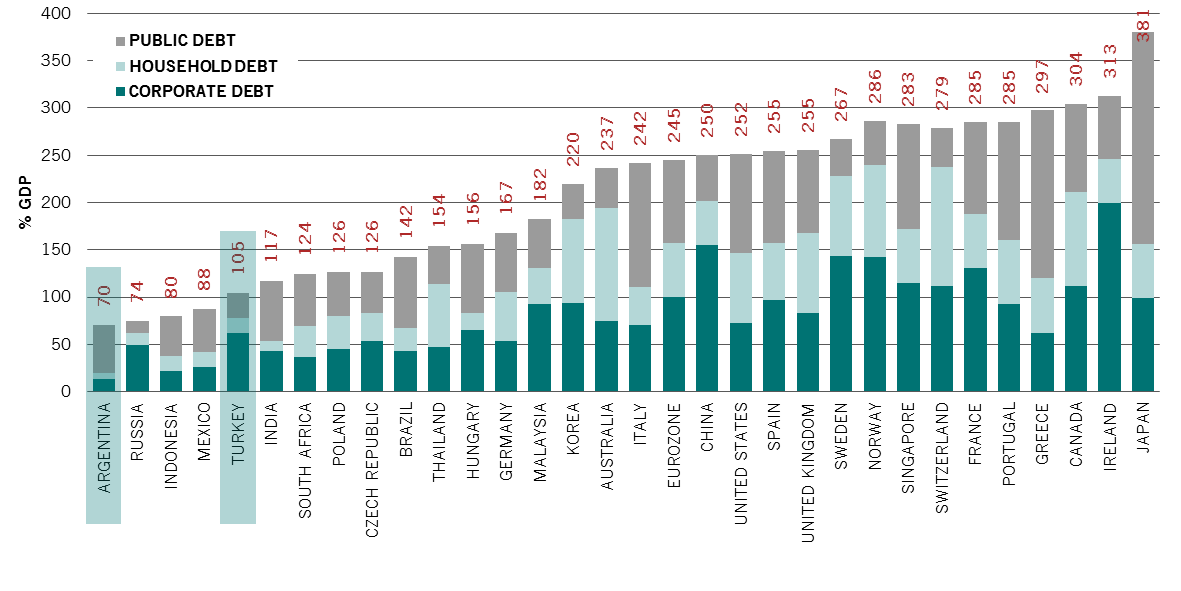

Argentina and Turkey share large fiscal and current account deficits. That said, debt is not the main issue; as Figure 1 below shows, their debt relative to GDP is relatively low.

The main issue is that investors have lost confidence in their ability to control inflation.

Fig.1 - Argentina and Turkey among the least indebted markets in terms of GDP

Total debt by sector for developed and emerging economies

Glass half full

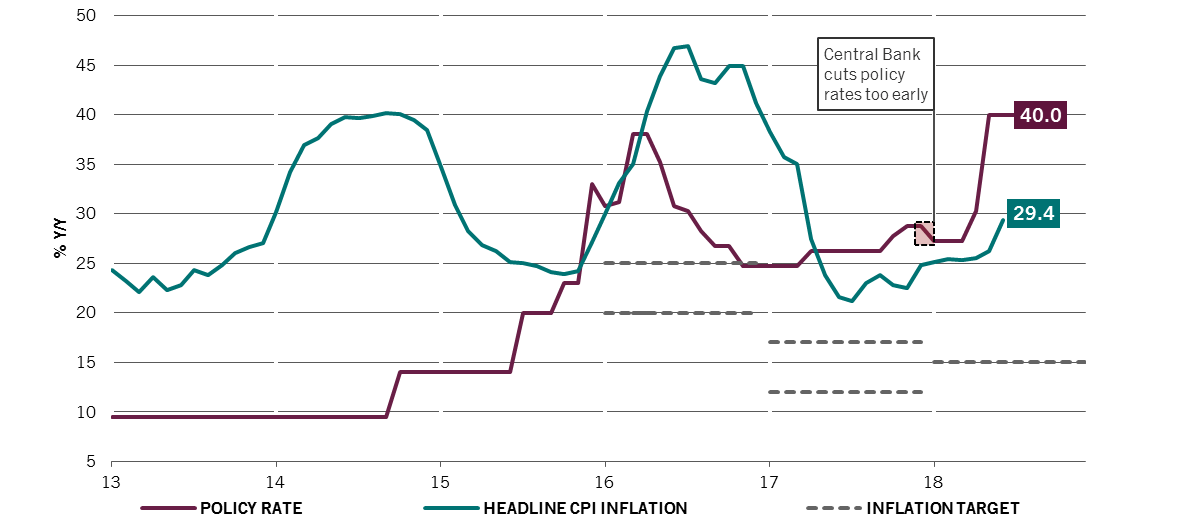

In Argentina, the Macri administration cut policy rates in late 2017, hopeful it would succeed in reducing inflation and mindful of 2019 elections. But it acted too early and caused loss of investor confidence in the central bank, which was forced to raise rates by around 13 percentage points to stem the currency's decline.

Fig.2 - Argentina's central bank cut policy rates too early

Argentina's CPI inflation, target range and policy rate

Source: Pictet Asset Management, CEIC, Datastream. Data as at 31.07.2018

This, together with other policy mistakes, cost the governor of the central bank his job, and saw the country burn through significant foreign currency reserves. Growth forecasts have almost halved since, and Argentina had to request to be bailed out by the IMF.

However, we believe that the worst is over if the government commits to fighting inflation over the medium term. In our view, necessary fiscal reforms are justified but will require political stamina to implement, especially as they will in themselves be inflationary.

We also believe they need to establish a more credible target range for inflation, higher than their current 15%.

Glass half empty

We are a lot less optimistic about Turkey under the rule of re-elected President Erdogan.

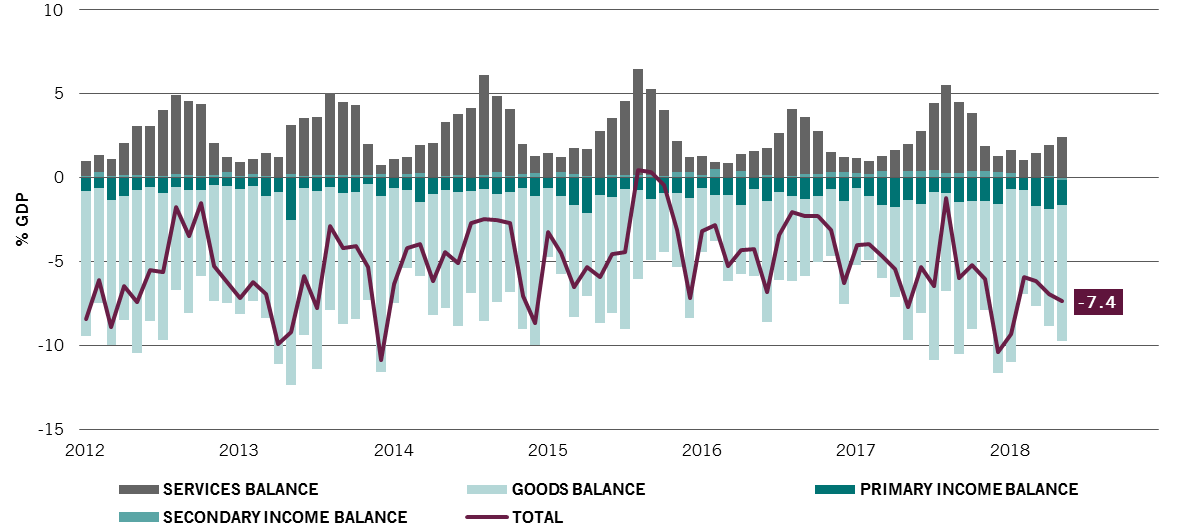

Firstly, as the chart below shows, there is a large and chronic current account deficit. Turkey's private sector (both households and corporates) is highly leveraged due to high domestic consumption and a low savings rate. The country has no choice but to finance its current account deficit mainly through foreign investments, and in USD, EUR or JPY as external investors' confidence in the lira has plummeted.

Fig.3 - Turkey's Current account

Breakdown by % GDP

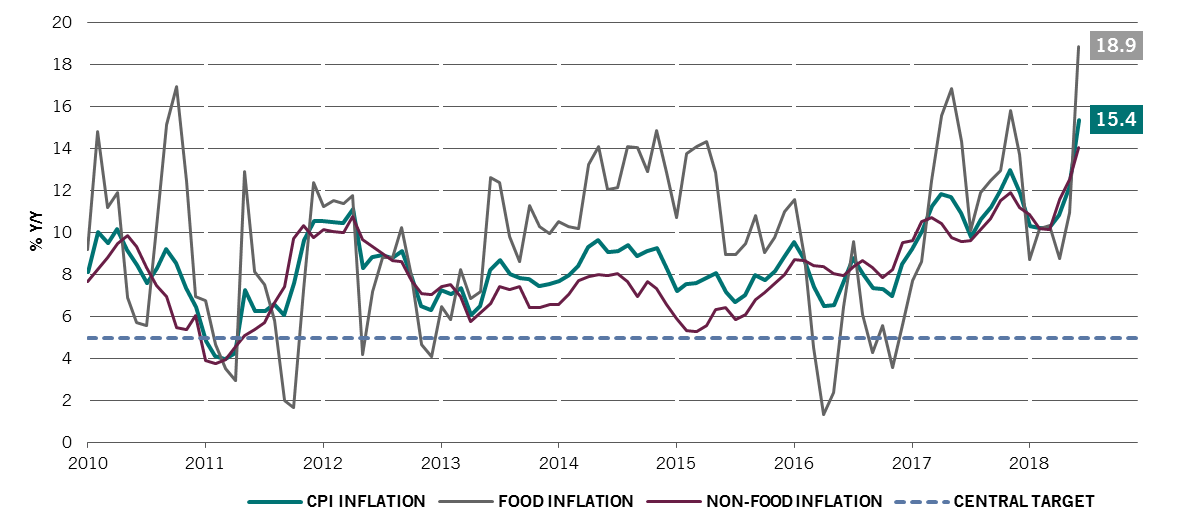

In addition to this external imbalance, the major domestic shortcoming is high inflation (see Fig.4 below), above 15 percent, and on a very steep trend. This is due to the lira's chronic weakness (down 56 percent against the dollar year to-date1) as well as rising energy prices.

With inflation expected to rise further, as the lira continues to depreciate, tighter monetary policy is urgently needed. However the Central Bank (CBRT) has disappointed by refraining from raising rates at its July meeting.

Fig.4 - Turkey's major domestic shortcoming is high inflation

Turkey's headline CPI, food & non-food inflation

Unlike in Argentina, we have limited confidence in Turkey's political regime to make the right calls for the economy. A focus on growth-enhancing measures instead of inflation control appears to be undermining monetary policy.

What's more, the decision by President Erdogan to appoint his son-in-law to head the new finance & treasury ministry raises concerns about the independence of the central bank.

In conclusion we think Turkey’s macro vulnerabilities, coupled with political concerns, put the country close to a breaking point. In our view, all the macro ingredients are now present for a full-blown balance of payments crisis.

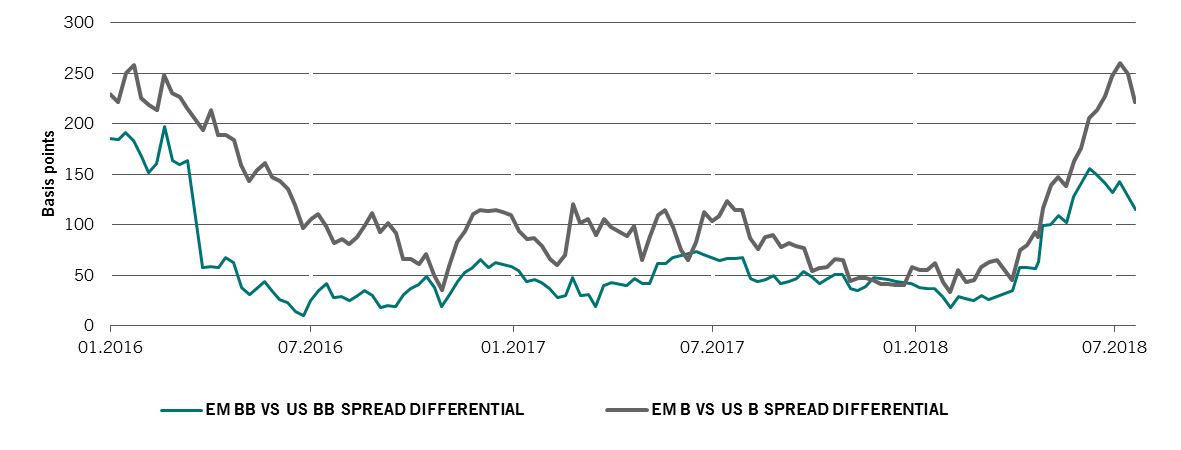

CHART FROM OUR EMERGING CORPORATE BONDS TEAM

By Karen Lam, Senior Client Portfolio Manager

As the chart below shows, high yield spreads in emerging markets have widened whilst in the US they continue to grind tighter.To us, brewing crises in Argentina and China have caused indiscriminate selling in the EM bloc. This creates opportunities for investors to buy the high yield credits of emerging markets that have suffered unduly, at particularly attractive levels compared with US high yield.

Fig.5 - EM High yield looks good value?

EM B & BB differential with US B & BB (OAS differential, bps)

MARKET WATCH

MARKET WATCH DATA

31.07.2018

READ More about emerging markets

After the fall

Emerging market bonds have suffered in recent months but fears of a renewed currency and debt crunch are overblown.

August 2018

Where are emerging market currencies headed?

The sell-off in EM currencies since mid-April is not comparable to the 2013 taper tantrum. Has it gone too far?

July 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.