Absolute return fixed income: transforming bond portfolios

Bond investors could be forgiven for feeling a little disoriented. In the decade since the US housing market crash, they have had to abandon several of the beliefs they previously held dear. It turns out, for instance, that negatively-yielding bonds are no longer an absurdity.

Thanks to sustained quantitative easing, the volume of fixed income securities trading at negative yields has never fallen below USD6 trillion since 2016. (The figure recently leapt to as high as USD17 trillion).

Also consigned to history is the notion that government bond markets are oases of calm. On one eventful day in May 2018, the yield on Italy’s two-year bond spiked by more than 150 basis points, the sharpest one day sell off in more than 25 years. There was also the US 'flash crash' of October 2015, which saw yields on 10-year Treasuries move up and down by 160 basis points within just 12 minutes. As the US Federal Reserve warns, such episodes will be more frequent in future as passive investing and algorithmic trading gather pace.1

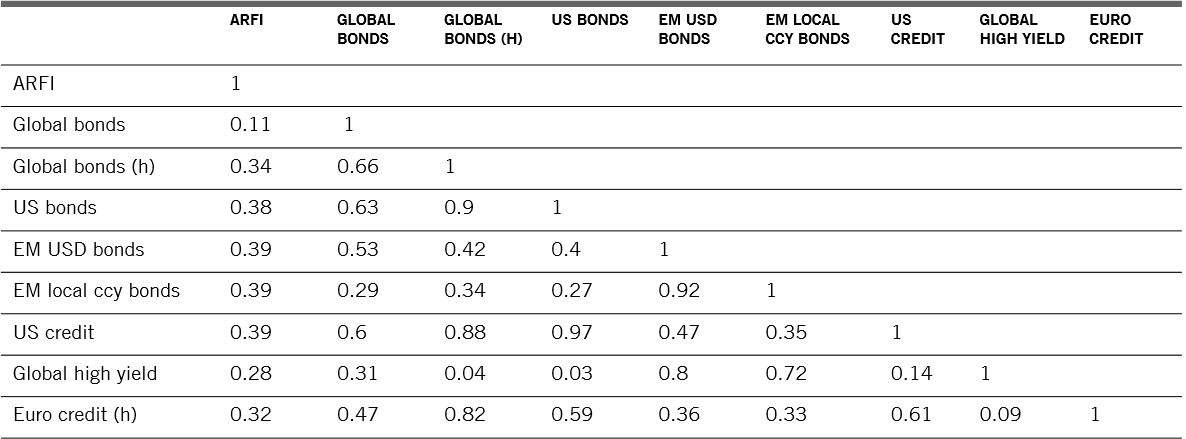

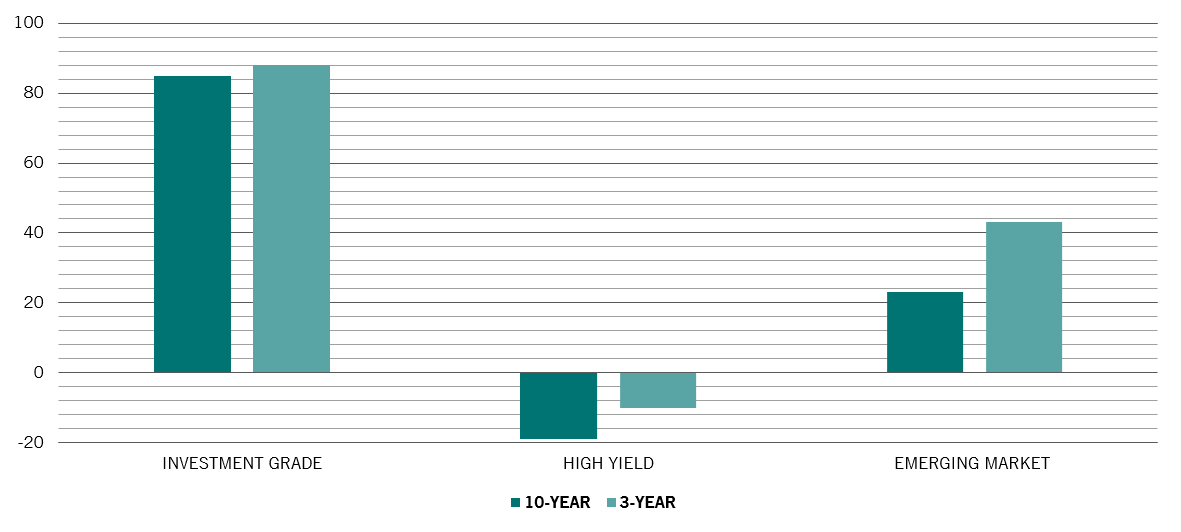

Bond investors face an additional complication. The definition of a diversified bond portfolio has also had to be torn up. That’s because the various fixed income asset classes that make up the global bond market2 have been tracking one another more closely in recent years. The correlation of the returns of US Treasuries, corporate debt and emerging market bonds has been higher in the past three years than in the past 10 (Fig. 1).

Investors can of course accept this new reality. They can simply resign themselves to owning a more volatile portfolio.

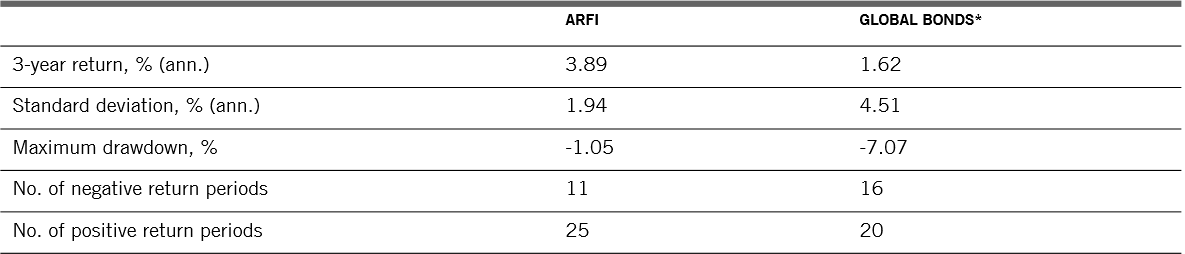

But there is an alternative. And it comes in the form of an absolute return fixed income (ARFI) strategy. Untethered from bond benchmarks, and free to deploy advanced risk management techniques, ARFI strategies are designed to deliver returns independent of the fixed income market.

For these reasons, they can serve as a buffer for - and complement to - a traditional fixed income portfolio.

Correlation of returns vs US Treasuries: investment grade, high yield and emerging market US dollar bonds

Source: Bloomberg; data covering period 30.06.2009-31.07.2019 and taken from Bloomberg Barclays US Credit Index, the Bloomberg Barclays US High Yield Index and the Bloomberg Barclays US Dollar Aggregate Emerging Market Bond Index.

Typically, ARFI funds target a specific level of return over a specific time-frame, expressed as a percentage point gain over a commercial lending rate or inflation.

To the investment managers running the ARFI strategies at Pictet Asset Management, delivering on this goal requires a multi-faceted approach to portfolio construction.

First, the investment universe needs to be broad. Investments should be chosen from the widest possible range of easily-tradeable bonds, currencies and derivatives. This makes it easier to construct a diversified portfolio composed of assets whose returns don’t move in tandem.

Second, more attention should be paid to the structural trends that influence bond returns than cyclical, and more volatile, factors such as economic growth and inflation.

Third, every investment idea must have a corresponding hedge in place to ensure the most favourable trade-off between risk and prospective return.