War and no peace

The effects of a full-scale trade war will extend far beyond the US and China threatening stagflation worldwide.

Written by

Luca Paolini

Chief Strategist

Patrick Zweifel

Chief Economist

When trade breaks down, everybody loses.

So investors should brace themselves for some fallout from the latest tit-for-tat trade dispute between China and the US, in which Beijing announced retaliatory tariffs in response to Washington’s move to increase duties on USD200 billion of Chinese goods.

Our calculations show a full-scale trade war between the world's largest and second largest economies has the potential to tip the global economy into a recession and lead to a sharp decline in world stocks.

Our model shows that if a 10 per cent tariff on US trade were fully passed onto the consumer, global inflation would rise by about 0.7 percentage points.

This, in turn, could reduce corporate earnings by 2.5 per cent and cut global stocks’ price-to-earnings ratios by up to 15 per cent.

All of which means global equities could fall by some 15 to 20 per cent. This, in effect, would turn the clock back on the world stock market by three years. US bond yields may fall, but the scale of decline will be limited due to an inflationary impact from tariffs.

Washington and Beijing may still be able to reach a deal at the June G-20 meeting. But should they fail, the planned tariff increases would cause both economies to suffer: we estimate that existing trade measures would reduce China’s growth by 0.5 per cent and the US’s by some 0.2 per cent.

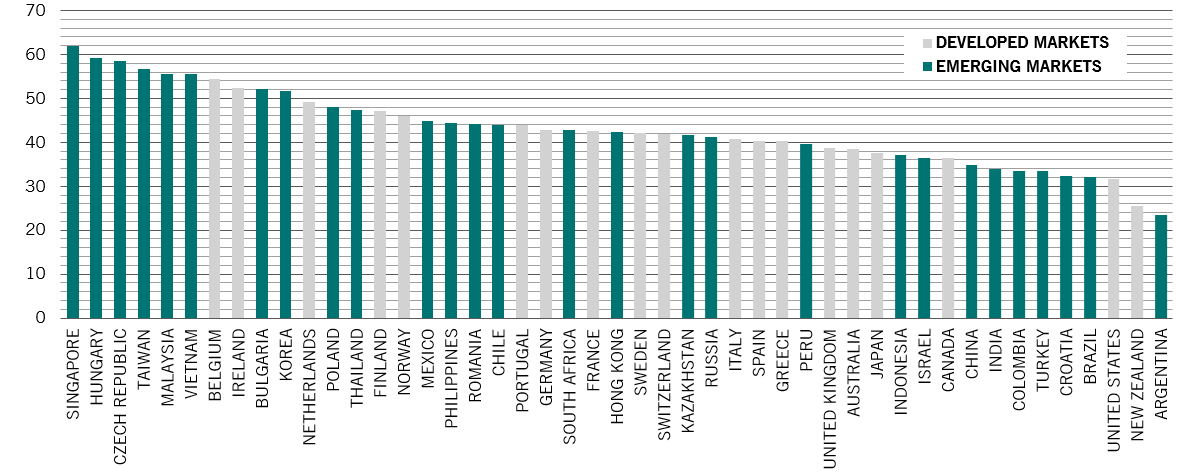

To make matters worse, the impact of a trade war will be felt far beyond the world's largest two economies. Open economies such as Singapore and Taiwan in Asia and Hungary, the Czech Republic and Ireland in Europe are potentially more vulnerable than the US and China (see chart).

globalised economies at risk

Global value chains participation rate*, % share in total exports

As for equity markets, Wall Street would suffer more from an escalation in the trade war than other stock markets, contrary to conventional wisdom.

This is because the US is the most expensive market in our valuation model and its sector composition is more sensitive to changes in economic conditions. On a 2019 price to earnings basis, the US market trades about 30 per cent higher than its European, Japanese and emerging market counterparts.

Cyclical stocks, and, in particular, expensive sectors like consumer discretionary and IT, will probably suffer the most, while shares of Chinese exporters should also come under pressure.

Investors shouldn’t bet on the US Federal Reserve providing additional support beyond what is already anticipated – financial markets have already priced in the prospect of a 25 basis point interest rate cut by the end of this year.

The picture that emerges from our analysis is similar to what investors have previously experienced. The history of financial markets shows that the erection of trade barriers is bad for equity markets: the S&P 500 fell 10 per cent in the three months after US President Richard Nixon imposed a 10 per cent tariff on imports in mid-1971.

As experience unequivocally shows, no one wins a trade war.

more from multi asset team

Barometer: Beware of exuberance

Exuberant global equity markets suggest optimism on economic growth and corporate earnings. Such expectations are likely to be disappointed.

May 2019

Bad omen: what the yield curve says about stocks

The inversion of the US yield curve strengthens the bear case for the economy and stock markets.

August 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.