How every aspect of the thematic portfolio construction process is geared to helping investors secure better returns from their equity investments.

Share this article

Why do we believe Pictet Asset Management’s Thematic Equity strategies have the potential to generate investment returns that are superior to mainstream stocks? There are a number of reasons.

Stock returns fuelled by powerful, long-term trends

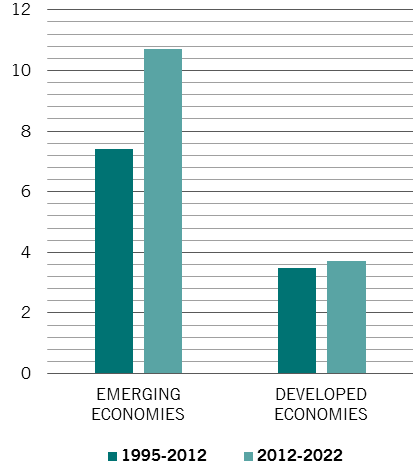

On the up: health spending rises worldwide

Rate of growth in health expenditure, %

Source: World Bank, Boston Consulting Group

The first is that returns from thematic equities stem from trends that are both long term in nature and largely unaffected by the ups and downs of the economic cycle.

In the health industry, for example, many companies have benefited from a persistent rise in health care spending worldwide. This is due to a major structural trend, the rise in life expectancy of the populations of the developed world. As Fig.1 shows, investment in health is rising at an accelerating pace, particularly in the emerging world. Experience shows this is unlikely to be derailed by any slowdown in the broader economy.

In the clean energy industry, meanwhile, the transformative power of climate change continues to drive investment in alternative sources of power. The technological advances that are emerging as a result of this wave of investment are helping slash the cost of renewable power. Production costs for onshore wind and solar power are expected to fall by 40 per cent and 60 per cent respectively by 2040.

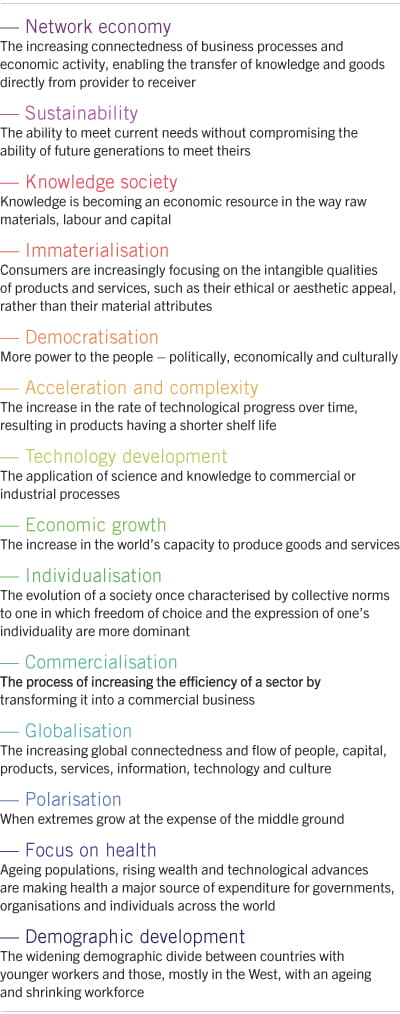

At Pictet Asset Management, we dedicate significant resources to the study of the non-economic megatrends that are reshaping the investment landscape. The 14 trends we have identified (see Fig. 2) form the basis of each of our thematic equity strategies.

Megatrends underpinning thematic equity strategies at pictet asset management

Source: Copenhagen Institute for Future Studies, Pictet Asset Management

Specialised companies better placed to deliver better returns

The second positive attribute that thematic stocks share is specialisation. The companies we invest in are attractive because they’re specialists in a particular field, not generalists whose activities span a broad range of industries or sectors.

And specialisation tends to be associated with higher returns.

There is a large body of evidence showing that the stocks of specialised firms do better than those of large, diversified companies over the long run. Essentially, large firms suffer from what is known as the “conglomerate discount”. Or, put another way, broadly diversified companies are worth less than the sum of their parts.

A study by the Boston Consulting Group (BCG) found that more complex the business, the more inefficient its investment. And, more importantly, the same study also established that wasteful investment acted as a drag on company stock prices.

By contrast, specialised firms – sometimes known as “pure play” companies – typically have a much clearer view of their strategic priorities and concentrate spending in areas that promise the strongest growth. Their capital allocation is more efficient which, in turn, builds a premium into their share prices over time, the BCG research found.

The companies we invest in are attractive because they're specialists in a particular field not generalists whose activities span a broad range of industries.

The upshot for investors is clear: a portfolio composed of the stocks of specialised companies – firms with three or fewer large divisions - should do better than a portfolio of diversified firms over the long run, other things being equal.

Our thematic strategies are designed to take advantage of this tendency. For each thematic strategy we manage, there are explicit rules for the construction of the portfolio. Each stock must have a high “thematic purity” for it to qualify as a potential thematic investment. Thematic purity is a proprietary, numerical indicator of how specialised a company’s activities are.

The higher the rating, the more specialised the firm. If, for example, a company within our Pictet-Water strategy is found to have a purity of 50, this means that half of its enterprise value is derived from marketing products and services that cater to the water industry. The average purity of the companies in our thematic portfolios is at least 65.

Specialist investment managers, not generalists

The specialist skill of our investment managers is another distinguishing feature of Pictet AM's thematic approach. Each thematic strategy is managed by a dedicated investment team, which carries out its own research and constructs its own portfolio. Every team member is a portfolio manager, sharing responsibility for the management of the strategy.

By dedicating all their attention to a clearly-defined group of stocks, investment managers develop distinctive, specialist expertise. This gives thematic equity investment managers a valuable advantage over traditional global equity funds, which work rather differently.

Most mainstream global equity funds are run by managers that are supported by several analysts, whose task it is to generate lists of their best ideas within their designated industry sectors. Often, portfolio managers struggle to process the vast amounts of data emanating from the thousands of stocks that form their universe.

An additional problem is that global or regional equity funds rarely confine themselves to the very best investment ideas their analysts have identified.

Thematic equity investment managers focus on a narrower range of companies and industry segments... this detailed knowledge can simplify the investment process, producing a more focused portfolio.

By contrast, thematic equity investment managers focus on a narrower range of companies and industry segments. This means they are able to build specialist expertise. And this detailed knowledge can simplify the investment decision making process, producing a more focused portfolio whose sources of return and risk are not only distinct but also more clearly understood. This, in turn, can increase the probability of generating better returns. There is ample evidence that selecting stocks from within specific industries – rather than across a broad range of sectors – can deliver better returns.

Thematic stocks don't feature in mainstream indices

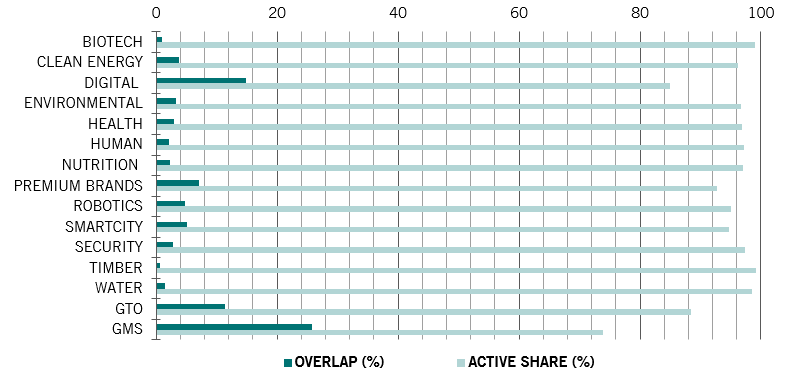

Companies that qualify as thematic investments share another attractive attribute: they do not feature prominently in traditional stock market indices. This has important investment implications. The stocks that find their way into the vast majority of the world’s equity funds are, by and large, constituents of major indices such as the FTSE 100 or the S&P 500 Index.

The result: a portfolio that is destined to generate sub-par returns.

By contrast, thematic equity strategies invest in specialised firms that are not represented in established benchmarks. Essentially, the approach is index agnostic.

Source: Pictet Asset Management, MSCI, Bloomberg, as of 31.08.2018. Overlap = sum of all overlapping fund holdings with index, adding up the min of the two weights. *GEO is an abbreviation for the Global Environmental Opportunities strategy, GTO is an abbreviation for Global Thematic Opportunities and GMS is an abbreviation for Global Megatrend Selection. Data taken from USD share classes of each strategy.

Built to deliver

So with specialist investment managers investing in specialised companies in dynamic industries, we believe we can build a portfolio that draws on the very best of human ingenuity. It’s what sets our actively-managed thematic equity funds apart. It’s also what can help investors get the most from their equity investments.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.