Asset allocation: equities are a turn off

A powerful rally across global stock markets since the start of the year has lifted equity valuations to levels that are at odds with our downbeat expectations for corporate profit growth. This has prompted us to cut equities to underweight and upgrade cash to overweight.

Stocks have almost fully recovered the losses sustained during last year’s fourth quarter panic thanks to policy U-turns in both the US and China.

The US Federal Reserve put the brakes on its aggressive liquidity squeeze, by halting its rate hike cycle and flagging a potential end to its balance sheet reduction. Slowing economic growth forced the Chinese to turn their attention from campaigning against the country’s shadow banking sector, to re-starting credit growth and injecting fresh fiscal stimulus. And meanwhile, the trade war between the two countries was nudged off the front burner.

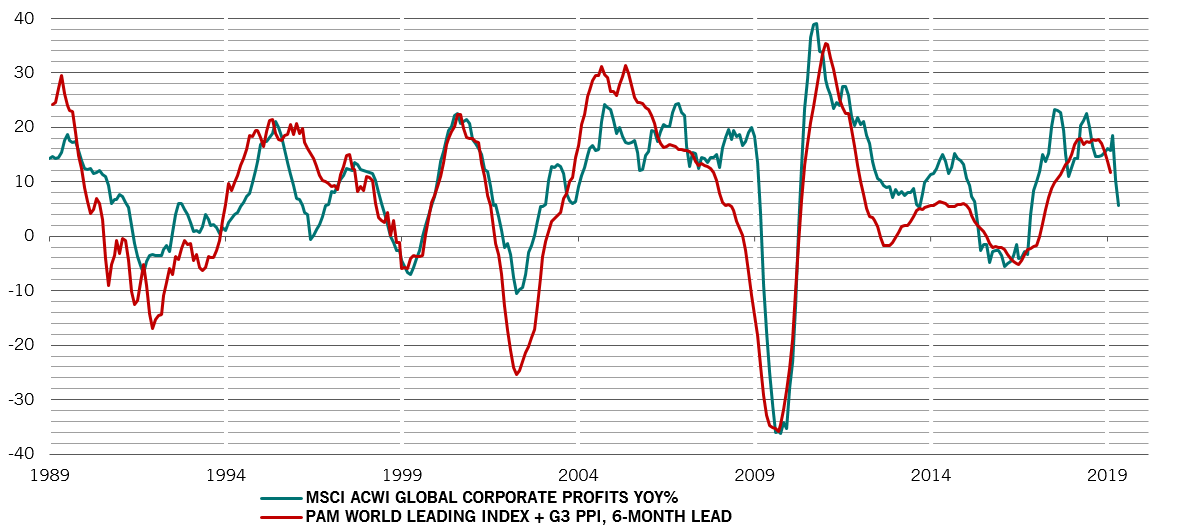

While it’s true that a softening of attitudes could pave the way for a healthier economic environment later this year, we remain cautious. Corporate profit margins are under increasing pressure from higher wages in an environment where firms are reluctant to raise prices. And with profits looking more vulnerable than analysts are willing to acknowledge, there’s scope for some negative surprises in the coming quarters.

April 2019

Our business cycle indicators highlight a deterioration in developed economies’ prospects. Gloomy sentiment surveys could well be overstating the case, but it’s clear growth is slowing.

Our leading indicators suggest that developed economies will grow by just 1.8 per cent this year from 2.2 per cent in 2018. Emerging market economies are doing considerably better. Growth should come in at 4.6 per cent for the full year – and would be stronger if the two big problem countries, Turkey and Argentina, were stripped out.

For all this, the slump in global trade appears to have bottomed out and there are some signs of modest recovery. As ever, the Chinese government is determined to support the country’s economy. It plans to inject stimulus equivalent to 3.8 per cent of GDP in the form of infrastructure, public spending and trade measures in 2019. That might be relatively modest compared to past measures, but it’s also likely to be increased should the need arise. Something to watch out for is the degree to which the Chinese authorities favour tax cuts over infrastructure spending.

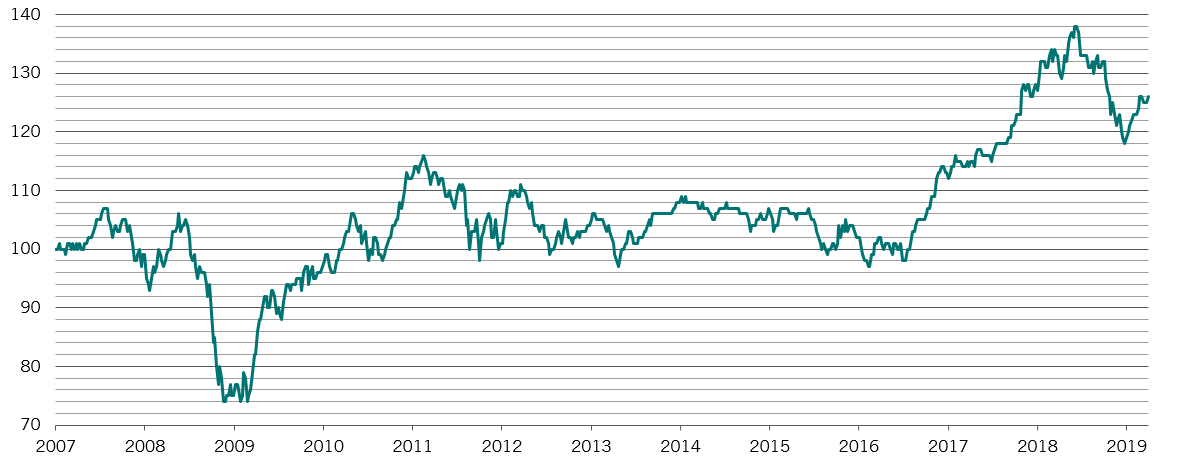

Global corporate profits vs world leading index

Our liquidity scores suggest a stabilisation in credit conditions after last year’s sharp tightening of the monetary reins. Investors should expect a mildly negative follow-through from previous policy moves, though. For instance, the Fed will be shrinking its balance sheet by another USD200 billion before calling a halt to its quantitative tightening programme. But an end to a squeeze is in itself stimulatory – there’s evidence that changes matter more than trend. Meanwhile, China, which now represents more than half of the liquidity flowing through the global financial system, is loosening policy again. And the European Central Bank appears to be on the cusp of launching another infusion of long-term bank credit.

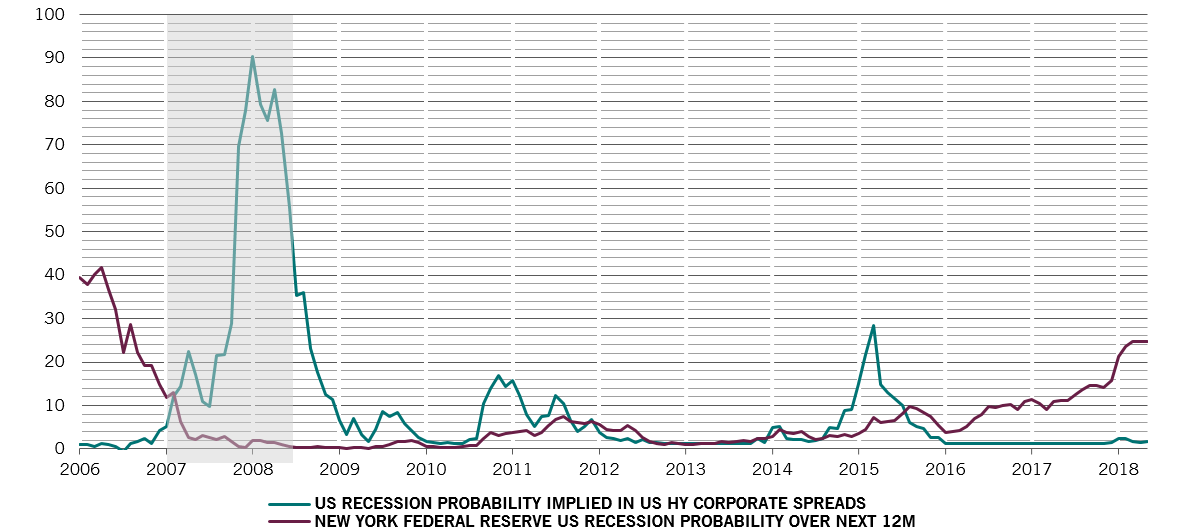

Our valuation analysis suggest that global equities are broadly fairly priced – conditional on earnings growth evolving as the market expects. True, analysts are more cautious than they were, with Japanese companies in particular subject to sharp earnings downgrades. Even so, we’re less optimistic than the market generally about the prospects for corporate profits. At the same time, markets seem to be under-pricing the risk of a recession. That’s particularly true for cyclical equity sectors and assets like US high yield credit. Indeed, bonds overall are looking expensive.

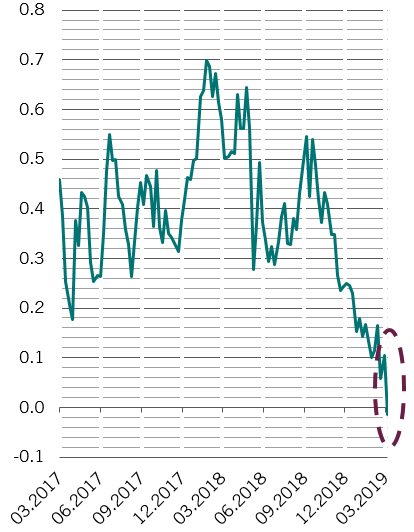

Technicals paint a broadly positive picture for fixed income, though they’re supportive of most asset classes. The exceptions are some emerging market currencies.