Asset allocation: fighting a slowdown

Policymakers have so far been successful in preventing a sharp global economic slowdown. The US Federal Reserve and European Central Bank have opened the monetary taps, while some emerging governments have provided fiscal stimulus, with Europe and Japan likely to follow suit with more public spending.

However, this doesn’t mean the world economy is out of woods yet. The missing piece in the global stimulus puzzle is China – where rising inflation and a build-up of corporate debt pose a dilemma for Beijing, which is under pressure to support the cash-starved parts of the economy hit by the trade war.

It therefore makes sense for investors to avoid the most expensive areas of the financial market. We maintain our neutral stance on equities and overweight cash. We also remain underweight bonds – European fixed income in particular is an unattractive, overvalued asset class offering limited potential for return in the coming months.

December 2019

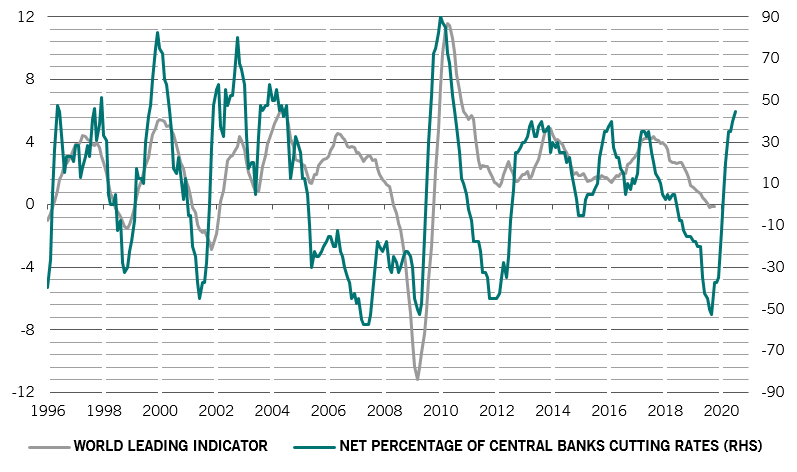

Our business cycle indicators show global economic conditions are slowly improving.

Our world leading indicator has picked up three months in a row to hit its highest in a year, thanks largely to an acceleration in emerging economies.

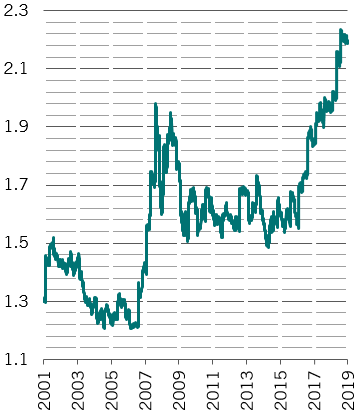

Encouragingly, this comes at a time when monetary authorities are increasingly shoring up growth: the proportion of central banks cutting rates has reached around 40 per cent on a net basis – a figure last seen at the height of the financial crisis (see Fig. 1). That said, we still expect global output to expand at 2.7 per cent next year, which is below potential and this year’s reading.

World leading indicator is GDP weighted. Central bank data is based on 40 central banks, with an 8 month lead. Source: Pictet Asset Management, CEIC, Refinitiv, data covering period 01.01.2000 to 01.12.2020

Our liquidity analysis shows central banks will provide monetary stimulus equivalent to a modest 2 per cent of GDP over the next half year, thanks primarily to the Fed and the ECB.

China has largely been absent from these efforts. This is because Beijing must walk a policy tightrope – economic growth has cooled to the weakest in nearly 30 years, while a recent jump in pork prices has pushed consumer inflation to an almost eight-year high.

According to our valuation readings, equities are neither expensive nor cheap at a global level. However, investors should find attractive opportunities in certain sectors and regions. We prefer stocks in the euro zone and emerging markets, where we expect corporate profit growth to accelerate next year. We also see value in health care and financial stocks.

Technical indicators remain unchanged, supporting our neutral stance on equities. These signals are however positive for emerging market assets – equities and local currency debt in particular.