Asset allocation: a central bank backstop

The global economy is cooling. Concerns about a full-blown trade war between the US and China have led to a significant deterioration in business confidence and economic activity, particularly in the developed world.

It's not all doom and gloom, though. Central banks are once again taking action to support growth.

The US Federal Reserve has signalled a halt to rate increases; it might also slow the pace of sales in its bond portfolio. What is more, China has implemented monetary stimulus on top of fiscal measures to stabilise economic growth. Together, the actions of the world’s most powerful central banks should help calm investor nerves following the market rout at the end of 2018.

Still, central bank action cannot completely eliminate investment risks: tensions between the US and China will linger for some time to come.

Taking all this into account, we have decided to maintain a neutral stance on equities and bonds.

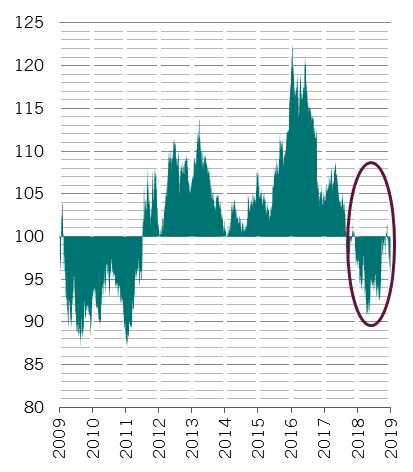

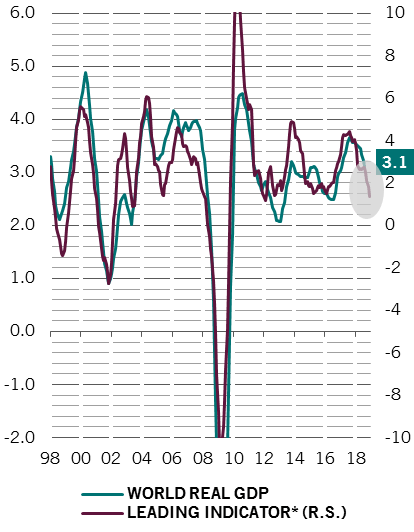

Our business cycle analysis shows economic growth is slowing in the developed world.

Our leading indicators point to real annualised global GDP growth of 2.6 per cent by end-March – that would be half a percentage point lower than the pace seen in the preceding six months to September.

The impact of Sino-US trade tensions is largely to blame. Exports and industrial production are falling sharply even though real interest rates and inflationary pressures are low.1

The US economy is experiencing a sharp slowdown, with its manufacturing activity in December registering the biggest monthly drop since late 2008, when the economy was in the throes of a recession.

The euro zone seems to be going from bad to worse – its industrial production is contracting at an annual rate of 3.2 per cent while Italy fell into recession for the first time in five years.

Emerging economies are faring much better, thanks to efforts by China to stabilise growth. Beijing has implemented a package of monetary, fiscal and trade measures to underpin the economy; the size of the stimulus is equivalent to 1.1 per cent of GDP. Latin America is also a bright spot. Growth there is accelerating, with Brazil’s new president Jair Bolsonaro injecting fresh optimism with his pro-market reforms.

World real GDP and leading indicator both going down

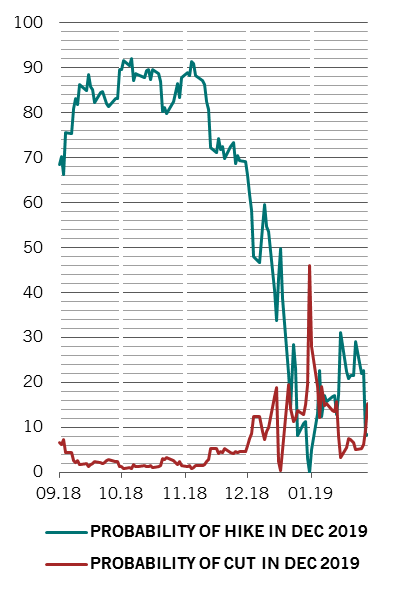

Our liquidity readings show monetary authorities in the US and China are beginning to respond to a growth scare.

Most notably, China’s monetary authorities have implemented as many as 15 new measures in the past four months to underpin growth and improve the flow of credit to households and small companies. On top of cutting reserve requirements, or the amount of cash that banks have to hold as reserves, the People's Bank of China is setting up a central bank bill swap (CBS) programme, designed to encourage banks to replenish capital through perpetual bond issuance and spur lending.

Our readings for Europe are less encouraging, however. There, the European Central Bank has stopped buying new assets at a time when the region’s fragile economy faces risks from Brexit and US-China trade tensions. Making matters more complicated, any attempt by the ECB to resume its bond buying campaig before President Mario Draghi leaves office in June is likely to face formidable political hurdles.

Our valuation scores remain neutral for riskier asset classes, although a number of asset classes look cheap.

UK stocks are among the most attractive asset classes. Not only does the UK market boast a large number of large-cap defensive companies, but it also trades at a high dividend yield of 5 per cent, compared with the global average of 3 per cent.2

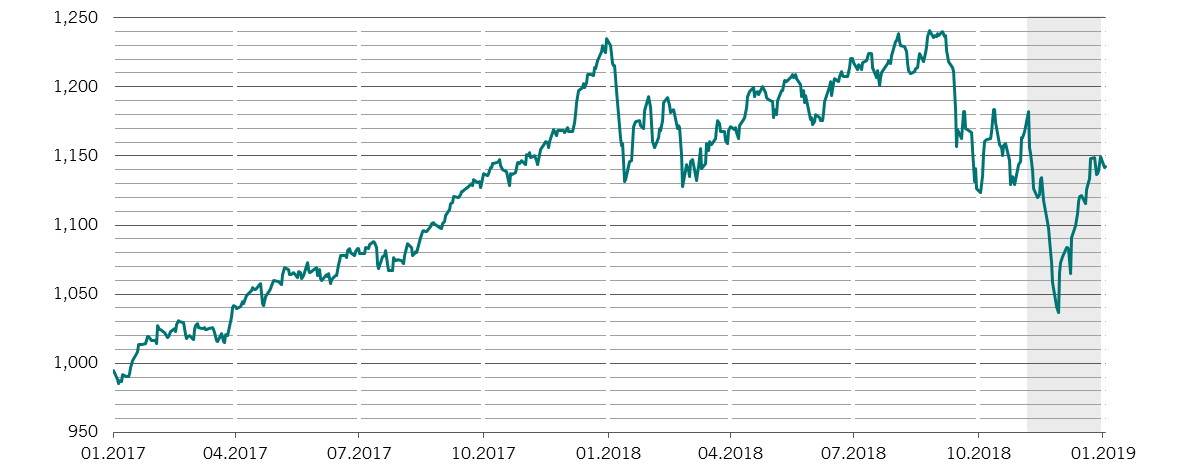

US stocks, by contrast, are overvalued. Even after a recent sell-off, US stocks remain expensive based on their cyclically-adjusted price-earnings multiples. Moreover, we expect more corporate earnings downgrades from analysts. Our forecast of 2019 for 3 per cent earnings per share growth in the US is half the consensus level.

In fixed income, emerging local currency debt offers the best value, especially as the region’s currencies trade at around 25 per cent below what we consider to be a fair value. German bunds are the most expensive bonds on our scorecard.

Our technical and sentiment analysis also supports a neutral stance on equities. Equity flows indicate that investors have been cautious in rebuilding their positions after the year-end sell-off, while our indicators point to continued volatility in the equity markets in the weeks ahead.