Asset allocation: looking to play it safe

Corporate profits are barely growing. Almost USD15 trillion of debt trades at yields below zero. And trade disputes are rumbling on. There is, then, not much for investors to be enthusiastic about. Not in the near term at least.

Our own global leading indicator suggests economic conditions will remain sluggish over the next few months. Our forecasts for world GDP growth have been falling since the summer; we now expect the global economy to expand at a sub-3 per cent pace compared to just above 3 per cent at the end of June. Such muted economic readings offset the positive signals that emerge from our assessment of liquidity and technical developments.

With this in mind, we remain underweight bonds and equities and overweight cash.

October 2019

Our business cycle readings don't give much to be optimistic about. Economic growth will slow a bit further before plateauing: our leading indicators suggest GDP will expand by around 2 per cent in early 2020, compared to the current rate of 2.7 per cent.

Trade is the economy's biggest problem. Although consumer demand is holding up, export orders are shrinking as a result of tariff hikes and other protectionist measures.

The impact is particularly visible in the two countries at the forefront of the dispute. In the US, weak manufacturing has pushed the ISM index to its lowest level in three years, and employment has also softened a little. In China, industrial production growth has slowed to a record low.

One bright spot is Europe. Our leading indicator for the euro zone has been positive for three months running, underpinned by healthy consumer spending.

Household demand is particularly strong. Even though retail sales edged down slightly consumer confidence is still very high and labour market conditions have improved. And lending to the private sector, a bug bear for the region, continues to gather speed.

Liquidity conditions are neutral to positive for riskier asset classes. The situation in Europe is encouraging, thanks to the European Central Bank’s recent interest rate cut and restart of its asset purchase programme, under which it will buy EUR20 billion in securities per month. In China, however, the monetary policy taps have not opened by as much as many investors had hoped.

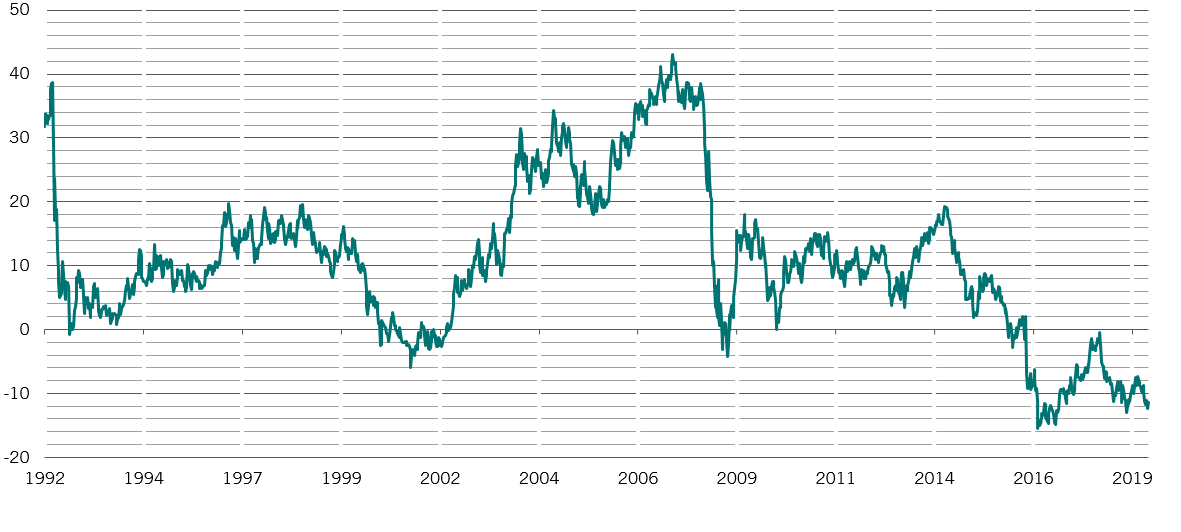

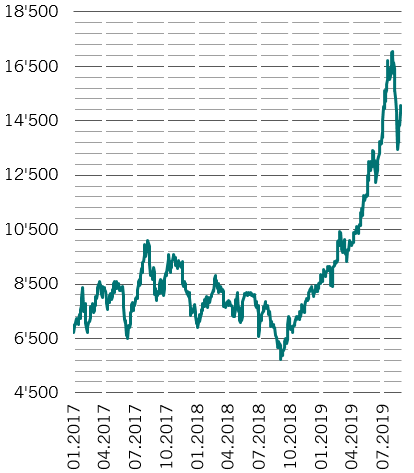

Negative yielding bonds, in USD bn

Our valuation models show global equities are fairly priced. Yet this masks wide divergences among regions.

The US is one of the most expensive equity markets. With a cyclically-adjusted price-to-earnings ratio of 29 times, US stocks are poor value both in absolute terms and relative to peers. On a global basis, value stocks are attractive relative to growth stocks.

In fixed income, government debt and credit are at trading at some of the loftiest valuations seen over the past two decades.

One positive signal for equities comes in the form of technical indicators. As the year enters its final quarter, stocks should benefit from seasonal effects – the final three months of the year are generally kind to equity markets. Another plus is investors' unusually bearish positioning, which limits the scope for any sharp fall in stocks. At the moment, market positioning is very cautious, as evidenced by our analysis of net long positions in safe haven currencies (Swiss franc, Japanese yen and gold) versus those in a basket of traditionally riskier ones.