China: a balancing act for bond investors

China's growing bond market offers attractive opportunities. Absolute return strategies can make the most of these while using hedges to protect against potential volatility.

Written by

Patricia Schuetz

Senior Client Portfolio Manager

The year has only just begun, and China is already dominating the headlines: its trade dispute with the US rumbles on; Beijing is once again acting to shore up growth; and tech companies are blaming slowing Chinese sales for earnings stumbles. All of which raise the critical question of whether investment opportunities arising from these developments outweigh the risks.

For us, as bond investors, it is a matter of finding the right balance between risk and prospective return – something that the Pictet-Absolute Return Fixed Income strategy specialises in by combining long-term strategic allocations with offsetting investments that act as a hedge against short-term risks.

As fixed income specialists, we have always been attracted to the long-term potential of China. While growth there is bound to be slower in future, it should also be more stable as the economy slowly rebalances away from commodities towards services, and as the exchange rate is liberalised. China is moving swiftly up the manufacturing value chain from quantity to quality. Its bond market is increasingly mature, diverse and international while the renminbi is touted as a reserve currency of the future. Further boosting the market's appeal is the fact that Chinese bonds offer relatively high yields and returns that don't correlate especially strongly with those of other asset classes.

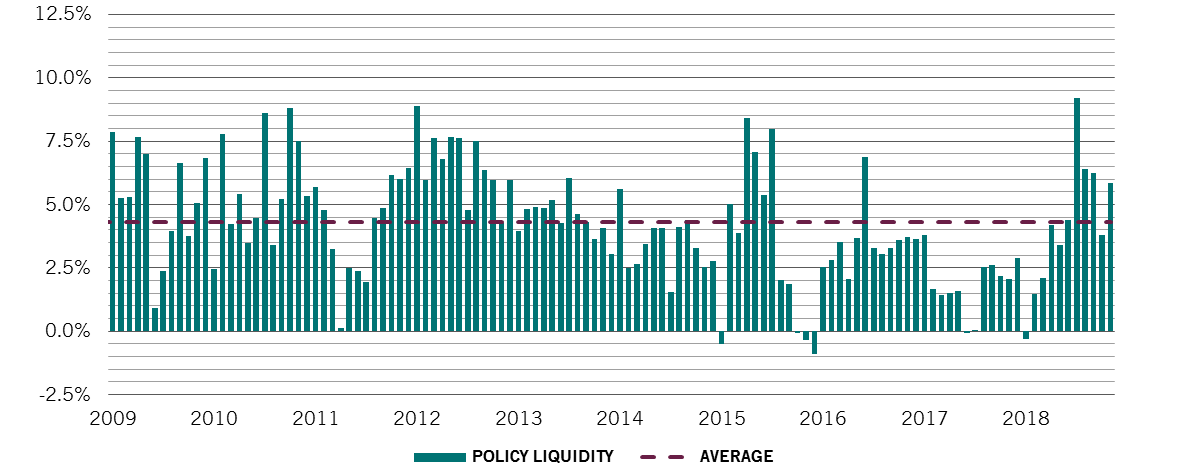

What is more, the government has in recent months pledged to adopt a looser fiscal policy alongside coordinated efforts to support domestic demand and GDP growth. It is cutting taxes for companies and households, as well as investing heavily in infrastructure. The People’s Bank of China is the only major central bank still administering monetary stimulus (see chart) and is expected to pump well over USD200 billion into the economy during 2019. Our economists forecast that Chinese gross domestic product (GDP) will grow by 6.4 per cent this year – twice as fast as that of the world as a whole, and more than three times faster than developed economies.

turning more accommodative

People's Bank of China liquidity flow, 6m moving average, as % of nominal GDP

Where China succeeds, other emerging markets also tend to benefit. This supports our broadly positive view on dollar denominated emerging market corporate debt. We also see several specific opportunities within China's dollar bond market itself, where any weakness in the currency – such as that seen in mid-2018 – would potentially provide attractive entry points.

Chinese asset managers, which are seen as strategically important to the country, will be among the key beneficiaries of the stimulus measures. So will property companies, whose capital structures are already showing an improvement.

Crucially, we believe that valuations for corporate bonds issued by companies in these sectors don’t reflect this potential.

Always prepared

However, long-term potential aside, emerging markets are well-known for bouts of short-term volatility and China is no exception.

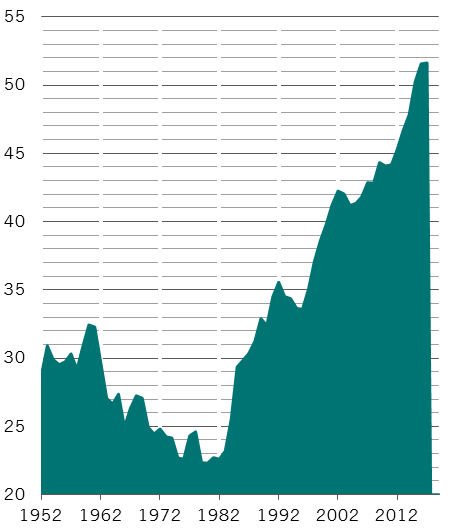

service boom

China's services sector, % of GDP

This is where our philosophy of balancing risks comes to the fore. And diversifying risk at every opportunity is a cornerstone of our investment process for the Pictet-Absolute Return Fixed Income strategy. To achieve this, we examine risks and correlations both within our individual investment themes and across the portfolio as a whole.

In broad terms, turbulence in emerging market debt tends to be accompanied by weakness in developing economies’ currencies. For us, holding a short position in a basket of such currencies represents an effective counter-balance to a long investment in emerging corporate bonds. We believe it is crucial to actively manage this currency position, though, given the idiosyncrasies of the countries concerned.

At the moment, holding short positions in Asian currencies offers a particularly compelling hedge against any temporary economic weakness in China.

We have also invested in Chinese sovereign credit default swaps (CDS) – instruments which insure against any deterioration in a bond issuer’s creditworthiness – to secure additional protection for our Chinese property positions. The possibilities for hedging our exposure are growing as the investment universe within China expands. For us, this makes the investment arguments even more compelling.

We have long believed that China’s transition from a manufacturing powerhouse to a more open and services-led economy will create diverse opportunities. Using all the investment tools available and focusing on balancing risks, we believe our approach to investing in China can both capture long-term value and limit the risks short-term volatility, thus ensuring the best possible risk-return balance for our investors. Such a flexible approach is outside the remit of many traditional fixed income strategies.

read more

Demystifying absolute return fixed income

There are alternatives to traditional bond funds. Investors worried about higher interest rates should consider them.

January 2018

A class apart: emerging Asia's fixed income market

Why investors seeking a stable and attractive source of return within a diversified bond portfolio should head to emerging Asia.

December 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.