[1] Wuhan University and Chinese Academy of Labour and Social Security Sustainability 201911 1418; doi:10.3390/su11051418

[2] Based on a difference between total social finance ex-equity and nominal GDP growth. Source: Pictet Asset Management Refinitiv and CEIC

[3] Trailing 12-month default rate to April 2019. Source: Bank of America Merrill Lynch

Silver lining for renmimbi bonds

Why China's demographics will speed up the internationalisation of the country's local currency debt market.

Written by

Cary Yeung

Head of Greater China Debt

China’s ageing population may become a problem for the world’s second largest economy but it could help transform the USD13 trillion bond market into an international asset class.

To understand why, it's important to look at the relationship between demography, saving and a nation's balance of payments position.

In China, the proportion of the people of working age – those aged between 15 and 64 – peaked about a decade ago at 64 per cent and will decline to 52 per cent by 2030, according to UN projections.

As the population grows older, its overall spending increases – mainly on health care and retirement. Indeed, pension expenditures have been growing at a faster annual rate than pension revenue since 2012.

And the median annual shortfall in China’s pension gap is expected to reach RMB1.41 trillion in 2050 from the current RMB50 billion1.

To plug that gap, the country will need to draw in its savings; they are expected to fall below 40 per cent of GDP by 2030 from a peak of 46 per cent.

This, combined with an increase in the country's spending, mean it is only a matter of time before China finds itself running a current account deficit – consuming more than it produces.

That will be an important development for China's debt market.

For when that happens the country will have to finance that deficit by borrowing more from abroad. In other words, it will turn from an exporter of capital to an importer.

Aware of this looming change, Beijing has been implementing a series of measures designed to liberalise capital markets and attract overseas investment.

And crucial to these reforms is the opening up of China’s onshore bond market.

Moves by global index providers to incorporate Chinese bonds in their mainstream benchmarks create a binding need for investors to include the asset class.

Since the 2017 launch of the “Bond Connect” programme which allows foreign investors to trade in Hong Kong without onshore accounts, Chinese authorities have also introduced the “Delivery versus Payment” settlement feature that has significantly reduced settlement risks.

Beijing has also given foreign institutional investors a three-year tax exemption on bond interest until November 2021. Furthermore, the People’s Bank of China plans to relax rules on repo and other derivatives trading for foreign investors.

These steps, along with additional proposed measures to open up the market, will ensure that RMB bonds become a bigger feature of international portfolios.

Foreign ownership of such bonds rose to a record USD271 billion in the first quarter from USD160 billion at end-2018. This was partly in anticipation of moves by global index providers to incorporate Chinese bonds in their mainstream international bond benchmarks.

The Bloomberg-Barclays’ Global Aggregate bond index began featuring Chinese RMB bonds in April, a move that should encourage other providers to follow suit. All in all, China’s index inclusion is likely to generate inflows of almost USD300 billion in the coming years.

International investors currently hold just under 3 per cent of the asset class, but the Peoples Bank Of China (PBOC) expects this figure to more than triple to 10-15 per cent over the next decade.

Correlation and currency

RMB bonds possess distinctive characteristics, which is why their addition to an international fixed income portfolio can alter its risk and return dynamics.

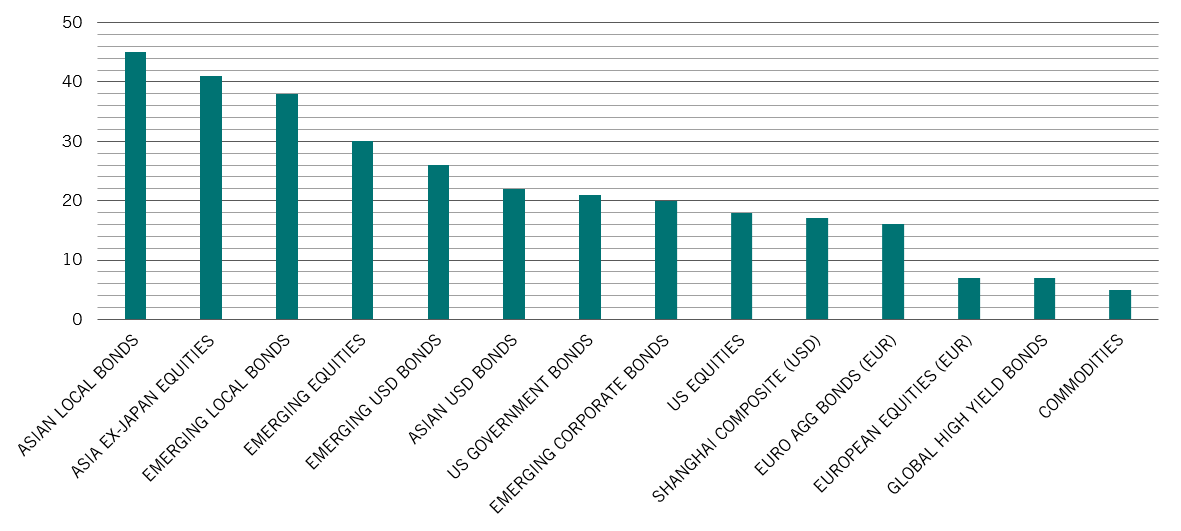

As Fig. 1 shows, the returns of RMB bonds do not correlate especially strongly with any major global asset class – whether bond or equity.

Fig. 1 independent mind

Chinese onshore bonds' correlation with other asset clases (%, 100 = perfect correlation)

RMB bonds’ yields are also higher than those on sovereign developed debt.

The yield on five-year Chinese government bonds stands at 3.1 per cent, compared with 1.9 per cent for US Treasuries, -0.24 percent for Japanese Government Bonds and -0.67 per cent for German Bunds with the same maturity.

Investors in onshore RMB bonds should also benefit from the potential of the Chinese currency to evolve into an international currency. This structural trend should see the RMB appreciate over the long term, providing onshorebond investors with an additional source of return.

Indeed, the internationalisation of the RMB is already taking shape in Asia.

The region has effectively evolved into what we call the RMB bloc as China’s neighbouring trade partners settle contracts in the Chinese unit.

The “redback” is now an important anchor for Asian currencies. Our economists estimate that the RMB’s fluctuations explain as much as 15 per cent of shifts in Asian exchange rates, compared with zero in 2006. The RMB bloc represents some 23 per cent of world GDP, compared with just 5 per cent in 2006.

This suggests the RMB should command a 13 per cent of global central bank reserves, seven times higher than the current figure.

China’s One Belt One Road infrastructure programme, through which the country promotes RMB-based lending and trades, should also help accelerate the RMB's internationalisation, as will increased capital flows into the country’s financial market and the opening up of its insurance and banking sectors.

Overcoming risks

It is clear that the Chinese onshore bond market is becoming an essential asset for international investors to have in their diversified portfolios. But investors need to be discerning.

A recent default by Chinese retailer Neoglory on its exchange-traded bond is a timely reminder of the risks for companies in highly-indebted sectors.

That said, we don’t see systemic refinancing risks in the asset class. Chinese authorities are implementing policies designed at slowing down the growth of corporate debt (see Fig. 2).

These targeted measures allow Beijing to reduce debt from past stimulus sprees, while providing support to small and private companies – most vulnerable to the negative impact from the US-China trade war.

Fig. 2 on target

Targeted policy measures to reduce private sector debt

The gap between credit growth and nominal GDP has narrowed to 1 per cent in 2018 from 7.3 per cent in 20142.

Also reassuring is that China’s default rate, at less than 1.5 per cent, is below that of many developed and other emerging markets3.

The onshore RMB-denominated debt market is likely to expand rapidly in the coming years to satisfy the changing needs of the world’s second largest economy. For these reasons, it has become too big for international investors to ignore.

More stories on China

Chinese local currency debt: coming of age

China's onshore renminbi-denominated bond market is an emerging asset class of global significance.

October 2019

A class apart: emerging Asia's fixed income market

Why investors seeking a stable and attractive source of return within a diversified bond portfolio should head to emerging Asia.

December 2019

When trackers won't do: investing in China A-shares

Chinese A-shares offer exciting investment opportunities - but it's also a market strewn with potholes. That's why an active approach makes most sense.

April 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.