Emerging markets' sunny prospects

EM economies are already outpacing their developed counterparts. And they'll benefit most from a rebound.

Written by

Mary-Therese Barton

Chief Investment Officer Fixed Income

Alper Gocer

Head of Emerging Markets Fixed Income

Forget the recent market upheavals, emerging market (EM) bonds are in something of a sweet spot. Indeed, the coming year could well prove to be the reverse of a rather grim 2018.

That positive appraisal boils down to two factors. First, although the global economy has been slowing, emerging economies are doing relatively better than their developed counterparts. Second, policies are being put into place around the world to re-ignite growth. Historically, EM assets tend to outperform in both of these economic environments.

Lex forex

The world leading indicator, which does a good job of anticipating what’s likely to happen to global growth, has been on a sharp downward trend since its 2017 peak. But while the outlook for emerging markets has also weakened, the bulk of the global slowdown is accounted for by developed economies.

The US Federal Reserve’s series of rate hikes through to last December, US President Donald Trump’s belligerence over trade, shifts in global demand for cars, as well as more localised problems like Italy’s and the UK’s fractious politics caused developed economies to shift into lower gear.

By contrast, the bulk of the EM slowdown has been concentrated in Turkey and Argentina – countries that have suffered self-inflicted economic injuries.

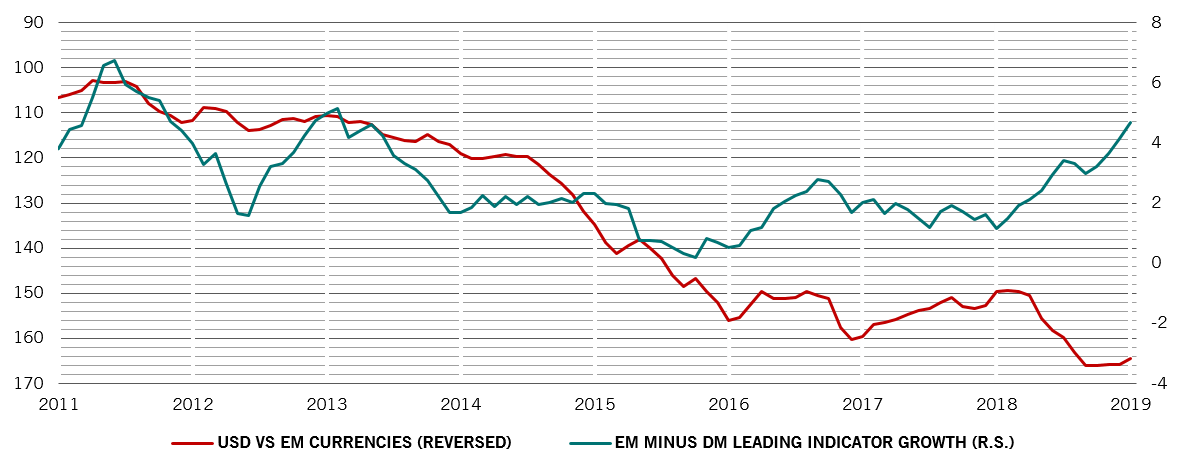

As a result, EM economies’ growth premium over their developed counterparts has opened up considerably over the past year to where the gap is now at its widest since 2013. (See chart)

open wide

Differential between EM and DM leading indices (y-o-y % change) vs. USD/EM exchange rate* (01.01.08 = 100)

That’s important because in those periods when the global economy has been slowing unevenly but developing economies have outperformed, EM currencies have appreciated against the dollar – at a rate of 1.7 per cent a year on average, according to our analysis.

That trend is even more pronounced for EM currencies of larger developing nations such as China, India, Korea, Russia and Brazil among others. On average, these currencies have gained an annual 4.7 per cent against the dollar, with Latin American and East European currencies tending to do best.

EM currencies could also benefit from US developments.

The Fed has pulled the emergency brake on its tightening policy. Not only has the central bank stopped hiking rates – there’s a growing expectation that its next move will be to cut – but it is prematurely ending the reduction of its balance sheet. This dovish turn should kick-start US growth later this year. But for now, it could signal an end to the dollar’s unrelenting strength.

As it stands, EM currencies are at close to their most undervalued against the dollar for at least the past two decades. Together these factors should help boost EM currencies and, therefore, EM sovereign bonds priced in local currencies – a substantial proportion of the return on this debt tends to be driven by foreign exchange movements.

Ready for a rebound

It’s not just the Fed that’s started to started to respond to the global slowdown. The European Central Bank is resuming its targeted longer-term refinancing operations for banks in an effort to shore up the flat-lining euro zone economy.

But once again, China is the major source of aggressive policy stimulus. The People’s Bank of China has chopped back banks’ reserve requirement ratios five times during the past year in an effort to reignite lending, with further cuts expected over the coming months. At the same time, the Chinese government has sharply expanded infrastructure investment, having cut it back during 2018.

Fundamentally attractive

More generally, EM bonds should be supported by improved local conditions. Prudent macro-economic policies and, in particular, EM central banks’ relative hawkishness suggest EM economies should be less volatile than in the past.

Meanwhile, global trade tensions are perhaps less of a cause for alarm than they might once have been. As EM economies have become richer, they’ve also become less dependent on exports, with domestic demand picking up some of the slack. And as countries like China have become increasingly developed, they’ve also taken on higher value-added manufacturing, with the effect of domesticating ever more of the supply chains that had hitherto been spread across a number of countries.

Once again, China is the major source of aggressive policy stimulus.

There’s also considerable potential for investment across the emerging universe to rebound with a lessening of trade tensions.

Among EM countries, we find Brazil particularly attractive. There, the new government’s reform agenda has helped to turn the focus back onto the country’s positive fundamentals. Indeed, we like Latin America generally.

By contrast, economies with big imbalances – not least Turkey and Argentina – are likely to remain vulnerable to sharp reversals.

All of which suggests that after the turmoil of 2018, most EM countries should benefit from their relative strength, together with realistic prospects for a broad-based rebound later this year.

related articles

Time for EM currencies to strike back?

The growth deceleration in emerging markets will be much less pronounced than in DM according to our leading indicators. This growth gap in favour of EM supports a recovery in EM currencies.

February 2019

Are weak retail sales a bad omen for EM?

Growth in EM retail sales has slumped in the last six months. Should investors be concerned?

March 2019

Emerging markets - Where to find growth in 2019?

Latin America is the only EM region set to do better than last year. We look at the countries with the strongest prospects.

January 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.