High yield – but not as you know it

Europe's evolving high yield bond market offers income-oriented investors new possibilities – without the need to take on a high level of risk.

Written by

Prashant Agarwal

Senior Investment Manager

European investors face a conundrum. On the one hand, they need to protect their portfolios in the face of lacklustre economic growth, continued sabre-rattling on trade and the rise of populism.

On the other, the available pool of defensive income-generating assets is shrinking, particularly within Europe's sovereign and high-grade bond markets. Despite the end of European Central Bank’s quantitative easing programme, yields on government debt and other high quality fixed income securities are near zero or even negative when inflation is taken into account.

The question, then, is how can investors secure enough income without taking on excessive risk? European short-term high yield debt may not be the obvious answer, but we think in the current climate it's a viable option. And for several reasons.

Strong fundamentals

For one thing, the quality of European high yield bond market has improved significantly in the past decade. It is now a liquid and diverse asset class, featuring companies operating across a wide range of industries. Today, some 71 per cent of the universe is made up of BB-rated bonds – just one notch below investment grade; this is up from 54 per cent in December 2008.

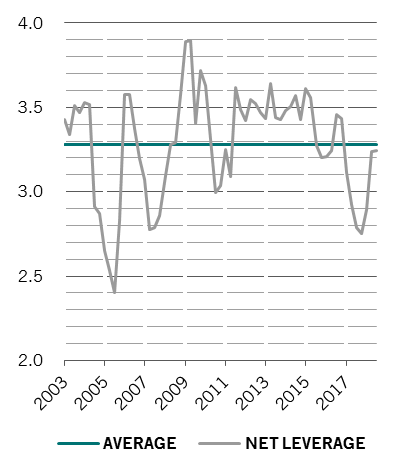

comfort level

European high yield – net leverage as proportion of EBITDA

Non-investment grade European companies have in the main been very cautious about borrowing since the 2008 crisis. At just 3.2 times earnings before interest, tax, depreciation and amortisation (EBITDA), their net leverage is below the 15-year average (see chart). Other indicators of indebtedness – including the free cash flow to debt ratio and interest coverage – also look healthy relative to history.

Moreover, default rates among European high yield bond issuers are running at just 1.5 per cent compared to 13 per cent during great financial crisis, and are expected to remain low over the coming year.1

Of course, if there is a recession, companies will find it harder to refinance their obligations and default rates will creep higher from the current low levels. But the fallout should be limited given that many European high yield issuers have already refinanced most of their near-term debt, shifting the maturity wall – the point when the majority of debt will need to be paid back or refinanced – out to 2022.

Furthermore, recent central bank action has reduced the probability of a recession occurring in the first place. The US Federal Reserve has signalled a pause in interest rate hikes. The ECB, meanwhile, has pledged to keep rates on hold until 2020, and has unveiled a new Targeted Longer-Term Refinancing Operations (LTRO) stimulus programme to support banks' lending to businesses across the euro zone.

Sweet spot

The combination of low interest rates and slow but steady economic growth is generally positive for high yield bond markets.

And by focusing on shorter maturity debt in particular, investors have the potential to secure higher levels of income without the volatility normally associated with the asset class.

Indeed, investing in shorter duration non-investment grade bonds is a strategy that has proved its mettle – both during the market turbulence at the end of last year and over the longer term.

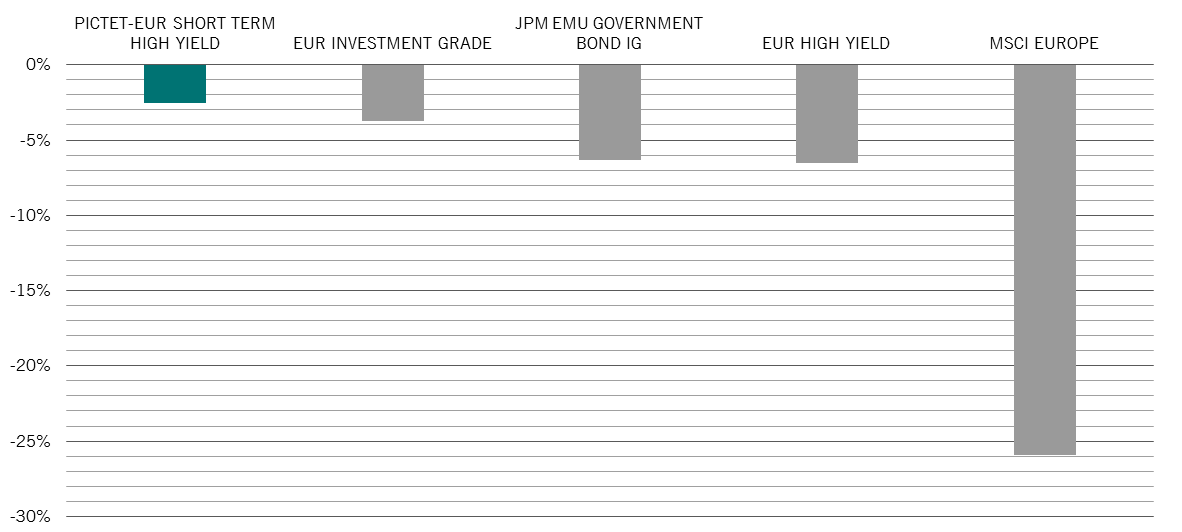

Since its inception in 2012, the Pictet-EUR Short Term High Yield strategy’s maximum peak to trough decline – or "drawdown" – has been much smaller than that for the broader high yield and investment grade universes, as well as for the equities market (see chart). It has also achieved a lower annualised volatility of returns over that period than any of the other investments in the comparison.

caution pays off

Maximum drawdown by strategy/asset class, % of absolute value

The resilience of short-term high yield debt is helped by the diversity of the market, which enables us to express a wide range of investment views.

Brexit is a case in point. Even though the UK is mired in uncertainty over its departure from the European Union, we continue to believe it is still a powerful economy with many strong businesses. To reflect both these considerations, we have tilted our portfolio towards non-cyclical businesses, confining our UK holdings to bonds that will mature over the next two years.

The recent calming of tensions between Italy's populist government and the EU is another development that investors can benefit from via the short term high yield bond market. We are looking to modestly increase our holdings in short term Italian corporate bonds as we believe their valuations underestimate the potential for a brightening in Italy's prospects. Here, we would also consider relatively longer maturities – three or four years rather than one.

Focusing on the final legal maturity of the bonds rather than on their duration – a measure more traditionally targeted by portfolio managers – helps to further reduce portfolio volatility. It is an important distinction because most high yield bonds are callable, with duration measured to the first or subsequent call date. That carries extension risk: if a company’s position deteriorates, it will not take up the call option, leaving the bond holder with more risk. Looking at the final maturity rather than duration can thus help to achieve more stable returns.

To sum up, high yield need not always mean high risk. With support from increasingly dovish major central banks, stable corporate fundamentals and a manageable near-term maturity wall, we believe short-term high yield debt offers a rare opportunity to generate an attractive income stream with limited volatility.

limiting risk: pictet eur short-term high yield strategy in action

Strong performance track record

Strategy returned -0.80 per cent in 2018, compared to -3.6 per cent for the broader European high yield market.

Modified duration of 1.7 years

Longest maturity positions – of four to six years – make up just 10 per cent of the portfolio and are spread over 20 to 30 issuers to further limit risk.

Focus on strong credit quality within universe

Debt rated CCC or below accounts for less than 3 per cent of the portfolio – versus maximum allowed 10 per cent.

more on fixed income

China: a balancing act for bond investors

China's growing bond market offers attractive opportunities. Absolute return strategies can make the most of these while using hedges to protect against potential volatility.

January 2019

Demystifying currency hedging in fixed income

Investing overseas means investing in a foreign currency too. That can make life a little more complicated particularly for bond investors.

February 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.