The office of tomorrow

Offices in a post-pandemic world will likely change in appearance, but they will remain key to cities – and commercial real estate portfolios.

Written by

Zsolt Kohalmi

Deputy CEO & Global Head of Real Estate

In March 2020, the City of London turned, virtually overnight, from a bustling hub of smartly-dressed office workers into an eerie ghost town. For the half a million employees in the financial district, working from home went from the occasional to routine. Eight months on, with many offices in London – and around the world – still largely empty, the question is whether we are living through a temporary shift or something more permanent.

The answer, we believe, is both. Undoubtedly, there will be an effect on office demand. After all, the pandemic has shown, to the surprise of both employers and employees, that we can work quite well from home – full time and en masse (at least for a few months).

People have appreciated not having to commute, the greater flexibility and the potential to spend more time with their loved ones.

But that’s not to say the office will disappear. It will simply transform into something new.

Innovation and comfort

As time has gone on, some of the drawbacks of working from home have become more obvious.

There are growing concerns – voiced, among others, by Andy Haldane, Chief Economist at the Bank of England – about the potential negative impact of long-term working from home on creativity and innovation. Nobody has come up with an effective way of replicating those chance encounters at the coffee station over Zoom.

The office also fulfils an important social need, with surveys suggesting employees are missing work socialising and mental health is suffering as a result. It turns out work socialising provides the antidote to personal socialising near the home.

For many, working conditions at home are also suboptimal due to lack of space, privacy, proper furniture and/or technology. With the divide between home and office blurred, some are working longer hours – perhaps in part because without the face-to-face it can take more meetings to create the same level of output. Nor has remote working proved to be a green card for relocation to other, potentially cheaper places. Tax and cyber security complications prompted companies to ban employees from moving to other countries, while a number of businesses – including Facebook – have moved to adjust pay based on employees’ location.

A selling point

That’s not to say things will – or should – go back to what we had before. Office workers expect to work 1.6 days a week from home in future, on average, while their employers see the number at around two days.1

Researchers at leading US universities have found that businesses are looking to the offices of tomorrow as an add-on to virtual work, with a focus on promoting “the ability to create weak ties and serendipitous conversations”.2 That will require better common areas, dedicated co-creation spaces and fewer fixed desks.

Office buildings will be more differentiated, with companies trying to really show their employees the benefits of coming to work. Selling points might include originality of the building, good natural light, windows that open to natural air, state of the art ventilation systems, outdoor space, and facilities such as gyms, electric bike racks, charging stations and showers. In a post-pandemic world, the amount of space per employee may become a significant consideration. This has decreased by over half over the past two decades, but now as a result of the pandemic, the value of personal space will increase significantly.

Good environmental credentials will become ever more important – to meet companies’ sustainability targets and employee demands, as well as to embrace tougher government regulations.

Location will be another key consideration. The offices most at risk of being shut are those situated in fringe locations, as well as those serving types of businesses – such as call centres – where there is limited scope for either socialising or innovation. Some of these buildings will likely be converted to housing, accelerating a trend that was already in place pre-pandemic in the UK and several European countries.

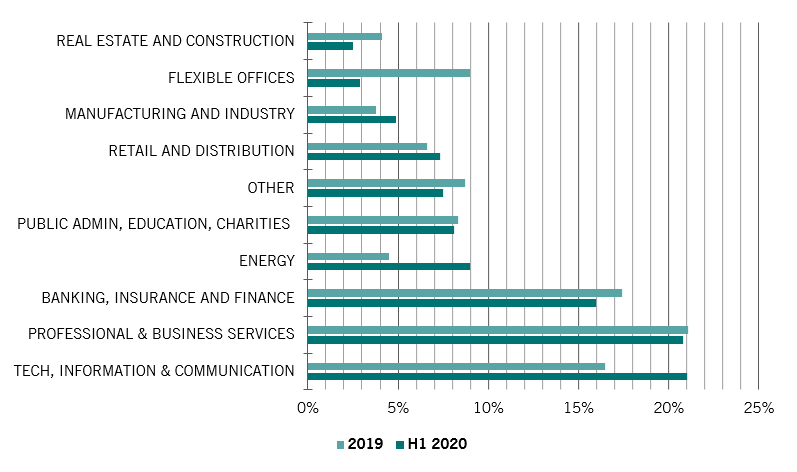

Fig. 1 - Tech in the lead

European office take-up by sector, % of total

Central office locations will likely remain in demand, particularly in areas favoured by technology companies. Although overall office take-up in Europe dropped by almost a third in the first half of 2020, year-on-year, tech sector’s share fell only 18 per cent as a number of big names pressed on with office plans.3 In London, for example, Google has bought an office and extended its lease on another one for a decade, Netflix agreed a deal that will treble its office space in the UK capital, while TikTok is in talks to upgrade to larger headquarters. Lift-share giant Uber and payment platform Adyen, meanwhile, secured new premises in Amsterdam.

While professional and business services may not be able to match tech’s rapid expansion, the sector includes many big, stable companies that will need to retain large offices in city centres. Such firms have to plan five, 10 or even 20 years ahead and the signs are that big office spaces are very much part of their future. Legal firm Baker McKenzie, for example, pre-let 151,800 sq ft in the City of London while accountant KPMG signed up for new offices in Munich. More broadly, circa 14 per cent of employers are increasing office space (in part to allow for social distancing), while 25 per cent are reducing it, according to Barclays and YouGov.

Even before this shift in occupier demand, there was already a shortage of modern, fit-for-purpose office space in key locations. As the economic scarring of the lockdowns becomes more pronounced, and the furlough schemes unwind, there will undoubtedly be weaker demand for certain locations, while the stronger assets may see a surprising resilience in their rental levels. This has been the case to date, and as in many areas the pandemic will result in bifurcation of performance between office assets in our view.

This bifurcation in office demand will create opportunities for value add property investors. By investing in commercial offices and facilitating a significant transformation – making it more environmentally friendly, facilitating innovation and collaboration, embracing technology – there is the scope to achieve better returns than by purchasing buildings that have already been overhauled.

We believe offices will remain a key part of our cities and our lives in a post-pandemic world. We also believe they deserve a space in diversified property portfolios. Some other real estate sectors, such as last mile logistics (which facilitate the final stages of online shopping deliveries) or pockets of residential, may provide higher growth. However, offices offer important potential for stable long-term income streams and – in the current environment – a particularly compelling opportunity to add value through modernisation and development.

read more about real estate investment

Post-pandemic cities

Coronavirus will change the shape of our cities, but the tide of urbanisation is unstoppable.

June 2020

Building a sustainable real estate portfolio

The property industry is the largest emitter of CO2. By making buildings more sustainable, we can help the environment and boost returns.

August 2021

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.