Private markets offer an attractive alternative route to investing in the tech sector.

Written by

Pierre Stadler

Head of Thematics - Private Equity

Share this article

Who will be the next Apple, Amazon or Facebook?

That is a million (or perhaps trillion) dollar question for prospective investors. Many in the investment community could be forgiven for casting envious glances at the baby-boomer generation, whose pension savings have been lifted by the tech sector’s outsized returns of the past several years.

But there should be plenty more such investment opportunities in future. Software, for example, remains the fastest-growing sector globally, with an expected compound annual growth rate of 15.6 per cent through to 2024.1 And, while Internet use has surged, its expansion will continue, with 41 per cent of the world still without access to the web.2 Then there’s 5G. Together with the Internet of Things, the next generation of wireless technology promises to take connectivity into uncharted territory.

As digital technologies become a bigger part of our lives, a new cohort of disruptive companies will emerge. Some of these firms will become household names. Others will have a lower public profile but still provide strong investment returns. Many will fail.

Indeed, while the opportunities are vast, investors in the tech sector need to tread carefully. To begin with, regulation is a big risk. Governments and anti-trust authorities are clamping down on data privacy and looking at new ways to tax the sector.

Valuations also require great scrutiny. The digital revolution – given added momentum by the effects of the Covid-19 pandemic – has propelled tech stocks to remarkable levels. Relative to their own history, valuations for listed tech stocks are higher than for virtually any other sector. The price-to-earnings ratio for constituents of the MSCI ACWI Tech index has surged to 25, compared to a 10-year average of 15.7

Yet listed tech companies – expensive or not – are no longer the only option for investors. The private sector is an increasingly attractive alternative. Not only are valuations more reasonable, but private firms also account for a bigger proportion of the investible universe.

Private companies are certainly proliferating – seemingly at the expense of their listed counterparts. Since 2000, the number of listed companies in the US has fallen to 4,000 from 7,000. And, those that do list do so at a more mature stage – the median age of a company going public in the US has risen from an average of seven years in the 1980s to 11 years between 2010 and 2018.

This is particularly true in tech. Here, the availability of private capital has enabled companies to delay listing for longer. In the US alone, private equity and venture capital investment into software has more than tripled since 2010 to USD96 billion.3 Staying private for longer suits tech firms because small, rapidly growing companies tend to have significant intangible assets. Typically they do not want to disclose their early stage research publicly and therefore favour a closed group of shareholders. They can also benefit from private investors’ greater flexibility in assessing the value of those intangible assets.

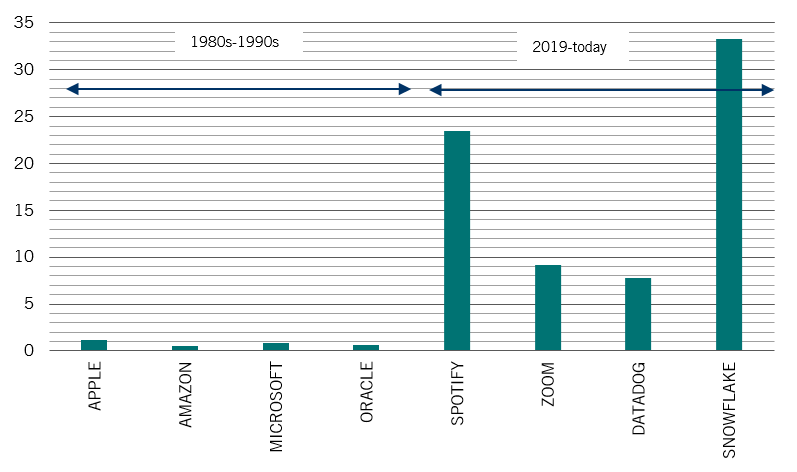

Consequently, by the time of the IPO, tech companies tend to be more mature, potentially past the period of ultra-fast growth – and high investment returns. So while Amazon, Apple and Microsoft all listed more than a decade ago with valuations of under USD 1.5 billion, recent IPO stars have been valued at much, much higher levels – including music streaming service Spotify at USD26 billion, cloud-based data warehouse firm Snowflake at a USD33 billion, video-conferencing provider Zoom at USD9.2 billion and cloud monitoring specialist Datadog at USD7.8 billion at IPO (see Fig. 1).

Valuation at IPO of selected major tech companies (USDbn)

Source: Capital IQ, Pictet Asset Management

Crucially, as companies stay private for longer, a growing share of their investment value is created prior to listing. Investors in private markets have much greater scope to nurture the businesses they invest in, increasing its chances of success. Research from the US Committee on Capital Markets Regulation has found that PE buyouts generally have a positive effect on both productivity and job growth in target firms.4

In leveraged buy-out (LBO) deals, the ability to own a majority stake in investee companies allows for less distraction from minority shareholders or equity analyst recommendations. In venture capital (VC) deals, meanwhile, founders will be looking for value added partners, i.e. investors that are more than just financial partners and that can bring a true expertise and often contacts. This is in stark contrast to the big listed names where even the largest of investors hold only a tiny fraction of the shares and thus have limited say on the board.

Star sub-sectors

Indeed, it is through the private sector that investors can best access what we consider to be the five most promising segments within the technology industry. These are:

Enterprise software – Companies have a strong incentive to become more digital in order to streamline processes, reduce costs, futureproof their business models and, increasingly, attract employees who seek greater flexibility in terms of working environment. Software has a key part to play in this shift. And given more than 90 per cent of software companies are private, there is a lot of choice for PE investors.5

Consumer Internet – During the Covid-19 pandemic, people moved their work, study, shopping, exercise and leisure activities online. We expect this trend to continue, particular as the younger, tech-savvy generation grows up and commands increased consumer power.

Fintech – From personal banking and investing to business accounts and international transactions, finance is becoming ever more hi-tech, and is no longer the preserve of a small group of large banks. New capacities brought by software as a service, or banking as a service will completely redesign the value chains of the incumbent financial services actors.

Cyber security – Cybercrime is growing rapidly, in complexity, in number of incidents and in terms of the scale of each attack. This has been further exacerbated by the rise in working from home, which involves the increased use of private devices. Cybersecurity is now a much bigger part of corporate IT budgets, and data privacy is another key growth area.

Industry 4.0 – Industry is embracing technology, from software to hardware. Automation, for example, is being embraced across the whole manufacturing and supply chain process, including logistics and packaging, as well as the design of the buildings and the tools.

Across these areas, we believe that private markets offer a rich selection of investment opportunities, and the potential of very attractive risk-adjusted returns.

PRIVATE EQUITY INVESTMENT IN TECH – THE PICTET WAY

Experience across both tech and PE

At Pictet, we already have a long track record of thematic investing, including in tech themes such as robotics, smart city, security and digital. We also have more than three decades of expertise to private markets, with access to top-tier private equity tech managers.

Strong focus

We target high conviction investments in five key segments to create a diversified portfolio of private tech companies.

Risk control

We invest across a wide range of vintages (from early stage venture capital to buyouts) to reduce exposure to the economic cycle. Mixing direct and fund investments enables us to limit single name risk.

Pierre Stadler joined Pictet in 2007 and is a member of PAA’s private equity Investment Committee. He leads the Private Equity Thematic Investment Team and co-leads PAA’s secondary investment activity. In his previous responsibilities at PAA, Pierre was responsible for the selection and monitoring of North American GPs. In 2014, Pierre spent four months on a secondment, working within the Carlyle Global Financial Services Partners team in New York. Pierre holds a Master of Arts in Accounting and Finance from the University of St. Gallen (HSG) and a Bachelor of Arts in Management from the University of Fribourg (Magna cum Laude).

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.