[1] We use the DuPont framework for calculating RoE: net profit margin x asset turnover x financial leverage

[2] Source: Worldscope, Pictet Asset ManagementSum of Net Income (before extraordinary) divided by sum of Common Equity for all listed companies comprising the top 99 per cent of market cap in the US, Developed ex US and Emerging regions. Annual data in USD. RoE of MSCI World Index stands at just under 12 per cent.

[3] Asset turnover ratio ex-financials. Sum of Revenues divided by sum of Total assets for all listed non-financials companies comprising the top 99% of market cap in the US, Developed ex US and Emerging regions. Annual data in USD. Source: Worldscope, Pictet Asset Management

Emerging market stocks: where the profits flow

Why investors could be severely underestimating the profitability of emerging market companies.

Written by

Laurent Nguyen

Senior Advisor

Gabriele Susinno

Senior Client Portfolio Manager

Emerging market (EM) equities deserve to feature more prominently in investors’ portfolios while allocations to developed market stocks need to be dialled down.

That is a view we have held for some time, not least because our economists expect EM countries to outgrow their developed peers by more than 3 per cent per year over the next half decade.

But there is another strand to our investment thesis: valuations.

Our analysis shows that investors are paying almost twice as much, on average, for the return on equity (RoE) generated by developed world stocks than for the same level of RoE from emerging world stocks.1

What is more, every incremental improvement in earnings prospects is more richly rewarded in developed markets than developing ones.

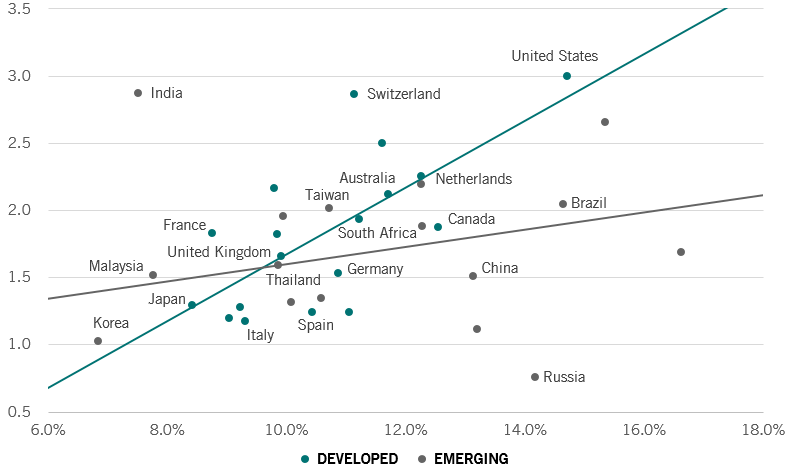

This can be seen clearly in the figure below, which shows that the trendline for prospective RoE versus price-to-book value is flatter for EM firms than for developed market companies.

We consider this an anomaly that will disappear over time.

EM profitability: underappreciated

Return on Equity (RoE) by valuations (Price to Book ratios)

Our view is reinforced by the fact that RoE among developed market firms is already close to its long-term average of 11-12 per cent, and unlikely to move higher.2

RoE in the developed world has in fact remained steady for the past 40 years, in part because of a decline in asset turnover.

Our calculations show that companies based in advanced economies are becoming less efficient in using their asset base to generate sales.

Forty years ago, companies would generate USD1.2 worth of sales for every dollar of assets they owned. That ratio has since fallen to 0.7.3

The rush of companies buying up rivals’ assets in M&A deals is partly to blame.

more from our Quest team

Value stocks: not always a bargain

History shows 'value' stocks can deliver superior returns during an economic slowdown. But true value is hard to find.

March 2019

The link between defensive stocks and ESG

Why financially robust companies also tend to have strong ESG credentials.

August 2019

Defence in depth: building a more resilient portfolio

Deploying multiple lines of defence can help investors build a truly resilient portfolio of stocks.

August 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.