Comparing absolute return fixed income and multi asset credit

July 2021

Marketing Material

MAC and Absolute Return Fixed Income: better together?

Multi Asset Credit (MAC) and Absolute Return Fixed Income strategies have long competed for investor attention. But does choosing one over the other make sense?

Written by

Andres Sanchez Balcazar

Head of Global Bonds

Share this article

At a time when interest rates are either ultra-low or even negative, positive inflation-adjusted returns are in short supply. To achieve them, bond investors have turned to strategies that have the flexibility to invest in different types of fixed income, the most popular of which are multi asset credit (MAC) and absolute return fixed income (ARFI).

Both have plenty to commend them. But they should not necessarily compete for investors’ capital.

We would argue that it doesn’t have to be a case of one or the other. In fact, combining the two can improve a bond portfolio’s diversification and increase its overall risk-adjusted returns over the long run. That’s because MAC strategies tend to do particularly well when interest rates and bond spreads are stable, while ARFI portfolios outperform during periods of credit stress or when interest rates are volatile.

Universe and diversification

MAC strategies tend to have a tilt towards high yield rather than investment grade bonds. This helps them perform especially well when market volatility is low and yield spreads between corporate and government bonds are narrowing. Their overall credit investment remit, however, can be very broad; some portfolios include investments in private debt and loans. This means MAC strategies traditionally offer greater diversification than a direct allocation to high yield credit. It is the freedom to allocate capital across credit sectors that gives portfolio managers the opportunity to secure excess returns. Not only can they shift between investment grade and high yield, but also within those broad sectors into loans, subordinated bank debt and more.

By comparison, the ARFI universe tends to be, by design, much broader, embracing the full fixed income toolkit; the investment styles and the sources of excess return or ‘alpha’ are more diverse than for MAC strategies. In many cases such portfolios also invest in credit, but often do so alongside currencies, interest rate products and derivatives. Probably the most common feature of ARFI strategies is the incorporation of capital protection/risk mitigation trades. The aim here is to improve risk-adjusted returns, but it also means that absolute return strategies tend to lag during bull markets in credit spreads.

ARFI strategies also use all the investment tools available, including derivatives, to manage risk – keeping the desired exposure while hedging out unwanted risk – across the full spectrum of fixed income sectors. This makes ARFI strategies less sensitive than MAC strategies to the overall direction of the credit market. For example, an ARFI strategy can protect against the risk of inflation and rising rates by taking a negative duration position.

As ARFI strategies usually have a lower allocation to high yield debt than MAC portfolios, they tend to have lower solvency capital requirements (SCR), making them more attractive as investments among insurance companies that are subject to Solvency II regulations.

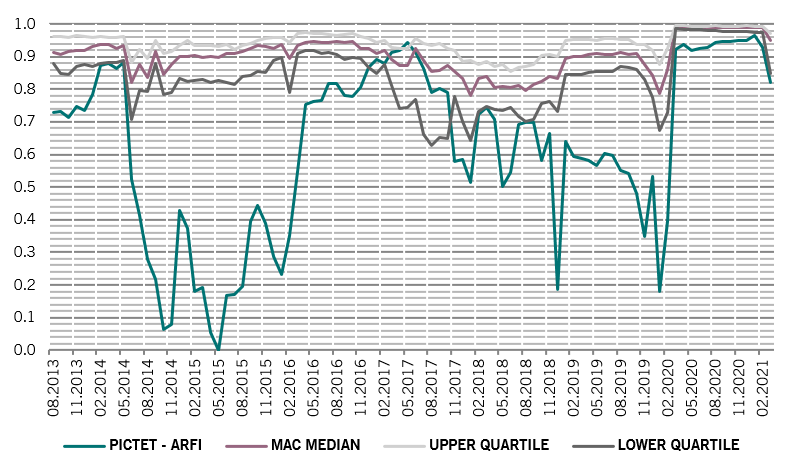

Fig. 1 - Diverse approaches

Correlation between Pictet-Absolute Return Fixed Income and the MAC universe

Rolling 1-year regression correlation between Pictet-Absolute Return Fixed Income vs. the International Fixed - Multi Asset Credit (Net) universe (monthly calculations) in USD. Data covering period: 31.08.2013-31.03.2021.

Source: Mercer.

The differences between the two strategies mean that correlation of the returns generated by ARFI and MAC strategies tends to be relatively low, and certainly much lower than between the returns of the different funds within the MAC universe (see Fig. 1). Combining the two strategies could thus offer diversification benefits compared to investing in just one.

Liquidity versus returns

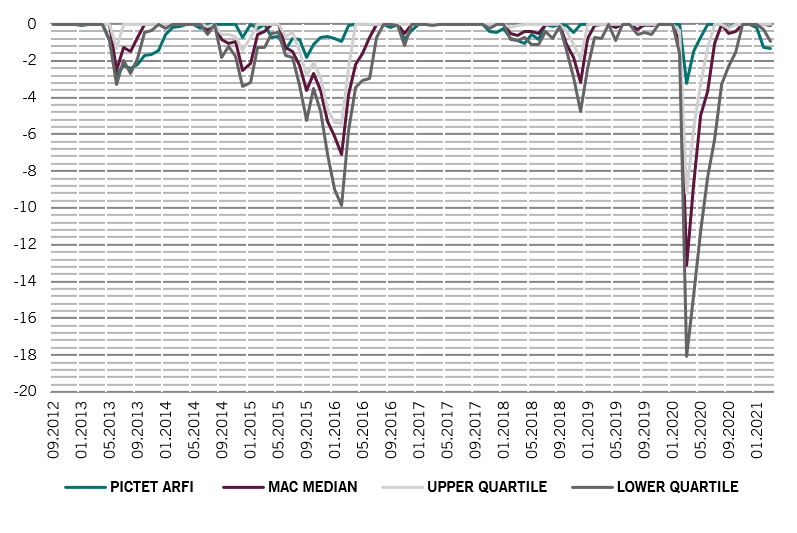

As a rule of thumb, credit investments and emerging market bonds tend to be less liquid than developed market sovereign debt and currencies. Thus, MAC strategies – which invest heavily in such assets – are usually less liquid than their ARFI counterparts, particularly if they have allocations to loans or private debt. This makes the risk of a sharp drawdown – or a sizeable peak to trough capital loss - more significant for the MAC strategies. This is particularly challenging during periods when market liquidity evaporates, as was the case in March 2020 and December 2018 (see Fig. 2). This is also the case even when comparing the top quartile MAC strategies with Pictet-Absolute Return Fixed Income.

Fig. 2 - Downside protection

Drawdown in USD

Comparison with the International Fixed - Multi Asset Credit (Net) universe (monthly calculations). Data covering period: 30.09.2012-31.03.2021.

Source: Mercer.

On the flip side, by capturing this liquidity premia, MAC strategies tend to deliver higher returns, on average, than their ARFI peers over the course of a market cycle.

For a typical MAC strategy, up to 80 per cent of performance would be attributed to movements in yield spreads. By comparison, the Pictet-Absolute Return Fixed Income strategy aims to diversify the sources of return evenly between spreads, rates and currencies. By doing so, Pictet targets a liquid portfolio at all times.

The source of return also tends to be different, with MAC taking a more bottom-up approach and ARFI tending to place more emphasis on top-down, macroeconomic factors in portfolio construction. In our ARFI strategy, for example, only about 10 per cent of overall performance comes from security selection.

Manager diversification matters

One downside of the ARFI approach is the fact that the strategies are not homogenous, and success is highly dependent on manager skill. Due diligence is thus paramount. The same can also be said of MAC, where return dispersion within the universe is similarly high.

Both are dependent on portfolio managers' timing when rotating between different investments. In fact, this is arguably more important for MAC strategies given that such portfolios concentrate investments in a narrower range of sectors and are less liquid.

Best of both worlds?

Despite their differences, MAC and ARFI vie for the same type of investor – one who is looking for a flexible approach that generates returns even in the current climate of low yields and low credit spreads. Yet, there are enough differences for the two types of strategies to be complementary. MAC can offer access to more exotic and less liquid securities that offer the prospect of higher yield. A well-balanced ARFI strategy, meanwhile, can harness strong macroeconomic trends while reducing risk and yet still delivering positive real returns.

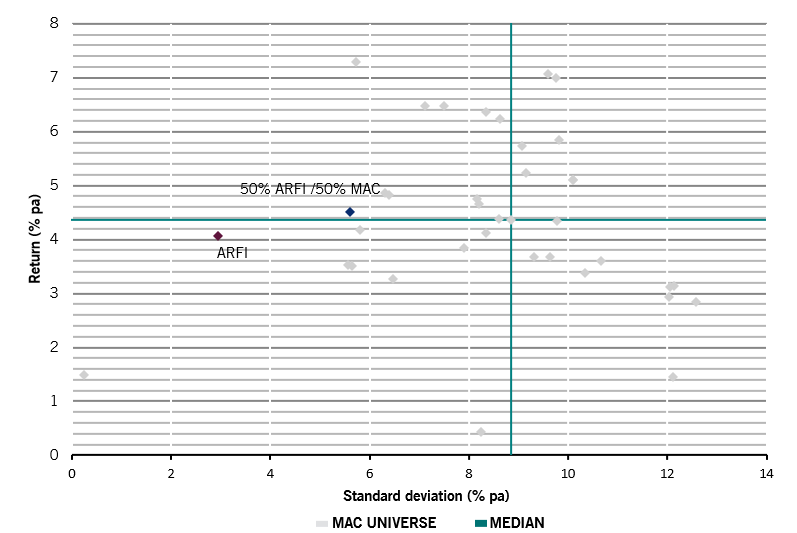

By combining the two and selecting the managers that play to each strategy’s strengths, investors can thus achieve better risk adjusted returns than by focusing on either one in isolation (see Fig. 3).

Fig. 3 - Better together?

Return and standard deviation in USD (after fees)

Comparison with the International Fixed - Multi Asset Credit (Net) universe (monthly calculations). For illustration purposes, the chart does not show extreme outliers; however these are included in the median calculations. Data covering period: 31.11.2017-31.11.2020.

Source: Mercer.

Andres Sanchez Balcazar joined Pictet Asset Management’s Fixed Income team in 2011 and is Head of Global Bonds. Before joining Pictet, he was a senior portfolio manager for Western Asset Management Company LTD for six years. During this time he was responsible for global, European and absolute return fixed income portfolios. Previously, he worked for five years as a global and European portfolio manager with Merrill Lynch Investment Managers. Andres started his career in 1997 at Banco de la Republica de Colombia, where he provided macroeconomic analysis on the US, Europe and Japan. Andres holds a degree in Economics from Universidad de los Andes and a Master's in Management from HEC Paris. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.