Investing overseas means investing in a foreign currency too. That can make life a little more complicated, particularly for bond investors.

Written by

Mickael Benhaim

Head of Fixed Income Investment Strategy & Solutions

Share this article

The post-pandemic divergence in central bank monetary policies has triggered sharp fluctuations in financial markets.

In what former Bank of England Governor Mervyn King describes as the age of "radical uncertainty",1 such volatility has presented challenges for investors, especially those who invest internationally.

Allocation to overseas assets opens up a world of investment opportunities that are unavailable at home. It also makes a portfolio more resilient by diversifying risks. But it comes with additional complications.

This is because on top of the underlying asset, investors also buy into the currency in which an international security is denominated.

And currencies are tricky beasts – because they can be volatile and unpredictable. They have the potential to influence portfolio returns, sometimes positively, sometimes negatively.

The impact of currency swings is felt most keenly among investors with international bond portfolios. Since fixed income securities return less, often far less, than stocks over the course of a market cycle, a 5 per cent fall in the US dollar, say, would have a bigger effect on euro zone-based international bondholders than on equity investors.

But currency moves this year have been of the sort that happen once in a generation. The yen, for example, lost a fifth of its value against the dollar to hit a 32-year low, while sterling slumped to a 37-year trough against the greenback. The euro fared better in comparison, but still fell to its weakest in 20 years against the US currency.

This means for US-based investors, any gains in the underlying fixed income assets would have been easily wiped out by foreign exchange moves if they did not hedge their currency risks.

This year may be exceptional. Still, experience shows that the world's major currencies, such as the euro, move up or down by approximately 10 per cent per year, which makes them 30 per cent more volatile on average than US government bonds. but half as volatile as equities.2

This is why fixed income investors in particular may want to consider hedging their currency risk.

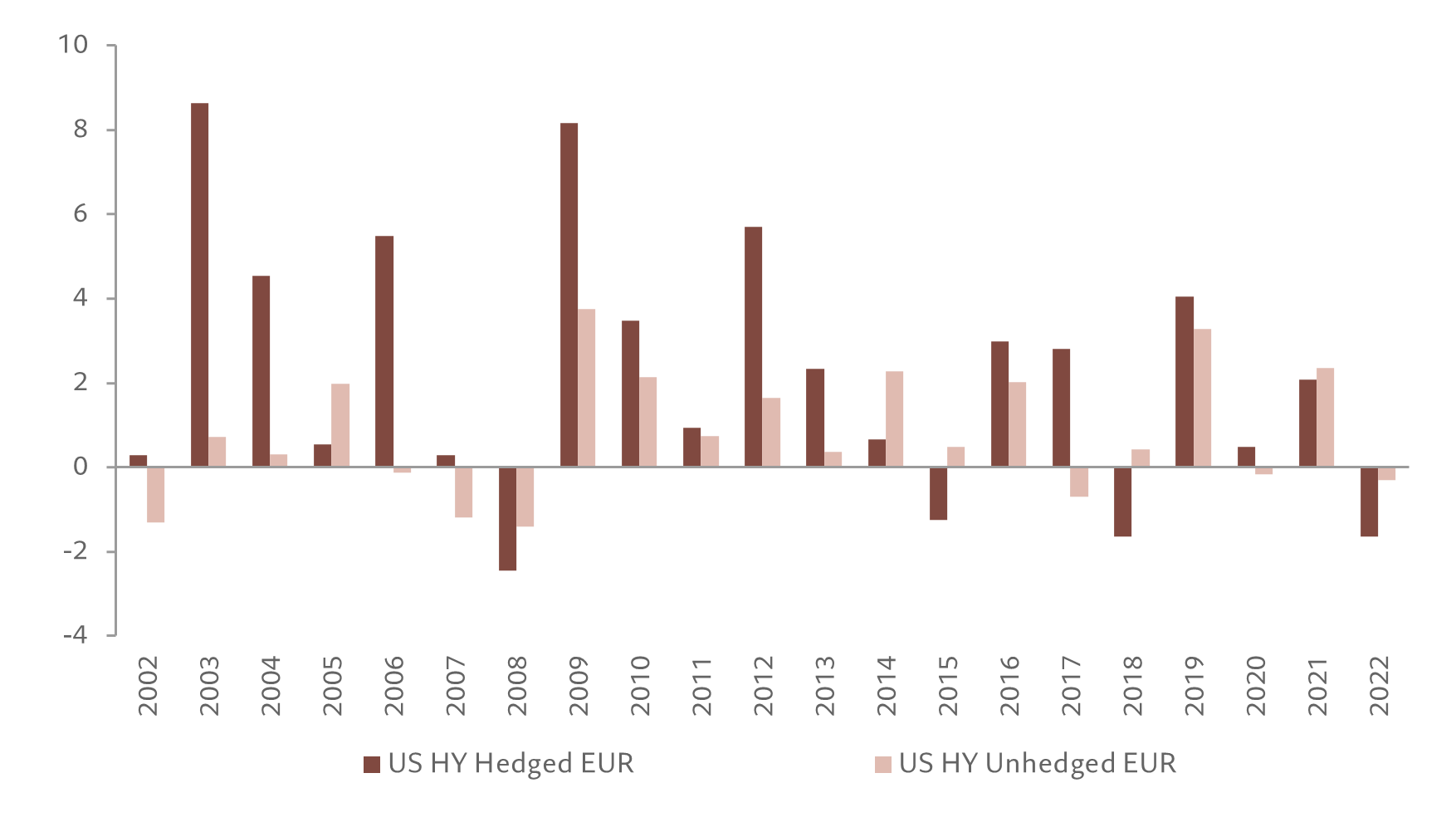

Take the example of a euro zone-based investor holding a portfolio of US high yield bonds. Over a long-term horizon and on a risk-adjusted basis, the investor would have secured a higher and more stable return had they used a currency-hedged investment vehicle rather than a portfolio that did not offer protection from exchange rate movements.

Fig. 1 Securing better risk-adjusted return

Annual risk-adjusted performance of US high yield, based in EUR, hedged vs unhedged (%)

Bloomberg Indices US High Yield 2% Issr Cap TR Index (Unhedged EUR/Hedged EUR) Source: Bloomberg, data covering period 31.12.2001-05.12.2022

But currency-hedged bond investments – which use instruments known as forward exchange forward contracts (a more detailed explanation is below) – don’t always deliver better returns.And performance doesn't always depend on an investor's time horizon.

A currency can, in fact, appreciate or depreciate for an extended period of time – months, or even years – sometimes moving way beyond what economists consider to be a fair level.

This means that investors who opt to insure themselves against adverse moves in exchange rates also forego the opportunity of securing positive returns from currency trends that go in their favour.

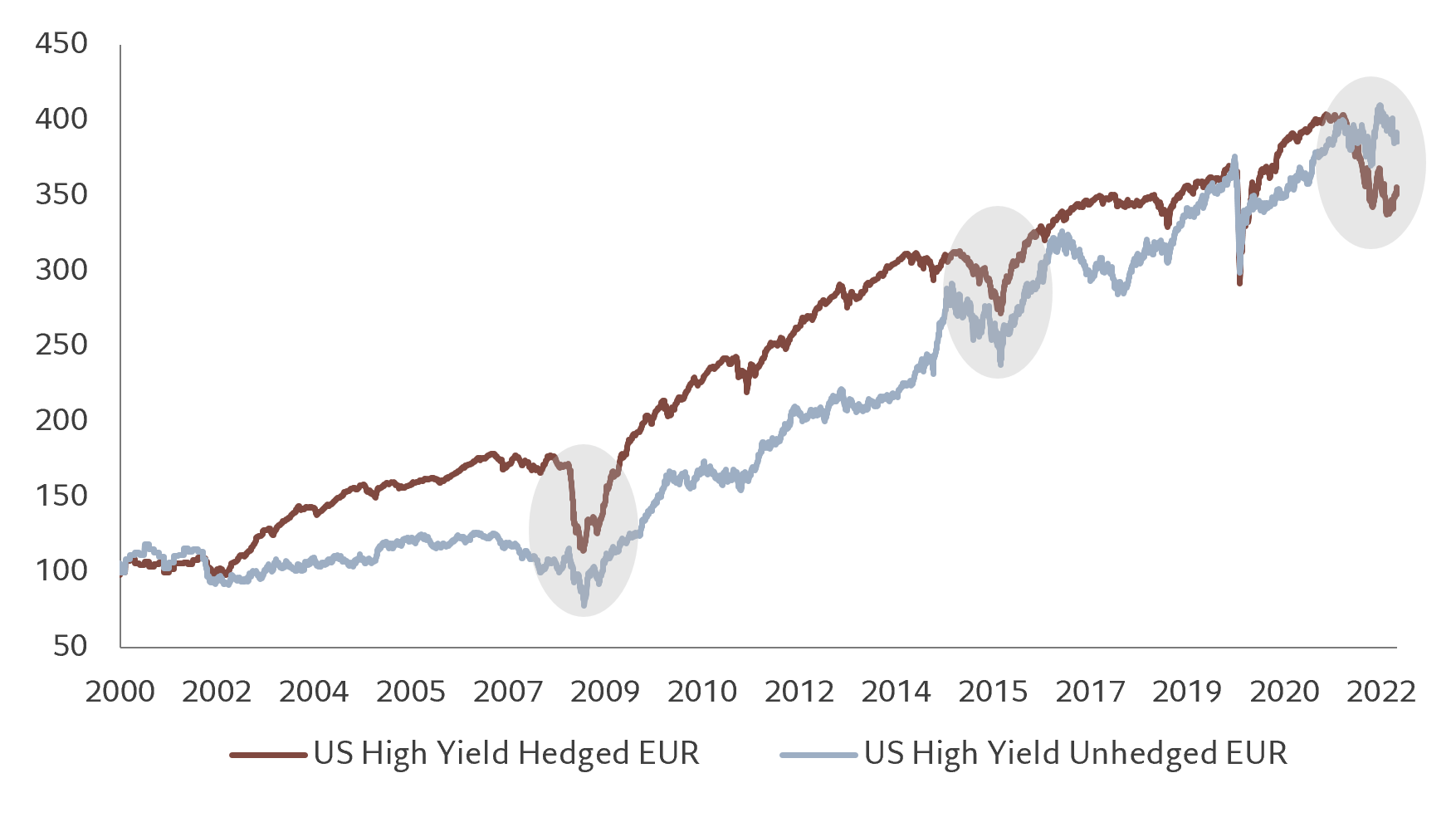

As shown in the Fig. 2, during risk-off periods, safe-haven flows into the dollar tends to result in a negative correlation between risky assets and the dollar. In these market conditions, EUR-based investors in the unhedged version of US high-yield debt has outperformed the hedged counterpart.

Fig. 2 Hedging bets

Bloomberg US High Yield 2% Issr Cap Total Return Index Unhedged EUR vs hedged, indexed

Source: Bloomberg, data covering period 29.12.2000 – 05.12.2022

This year's violent moves in the FX market also highlight why currency hedging can sometimes be counterproductive in fixed income.

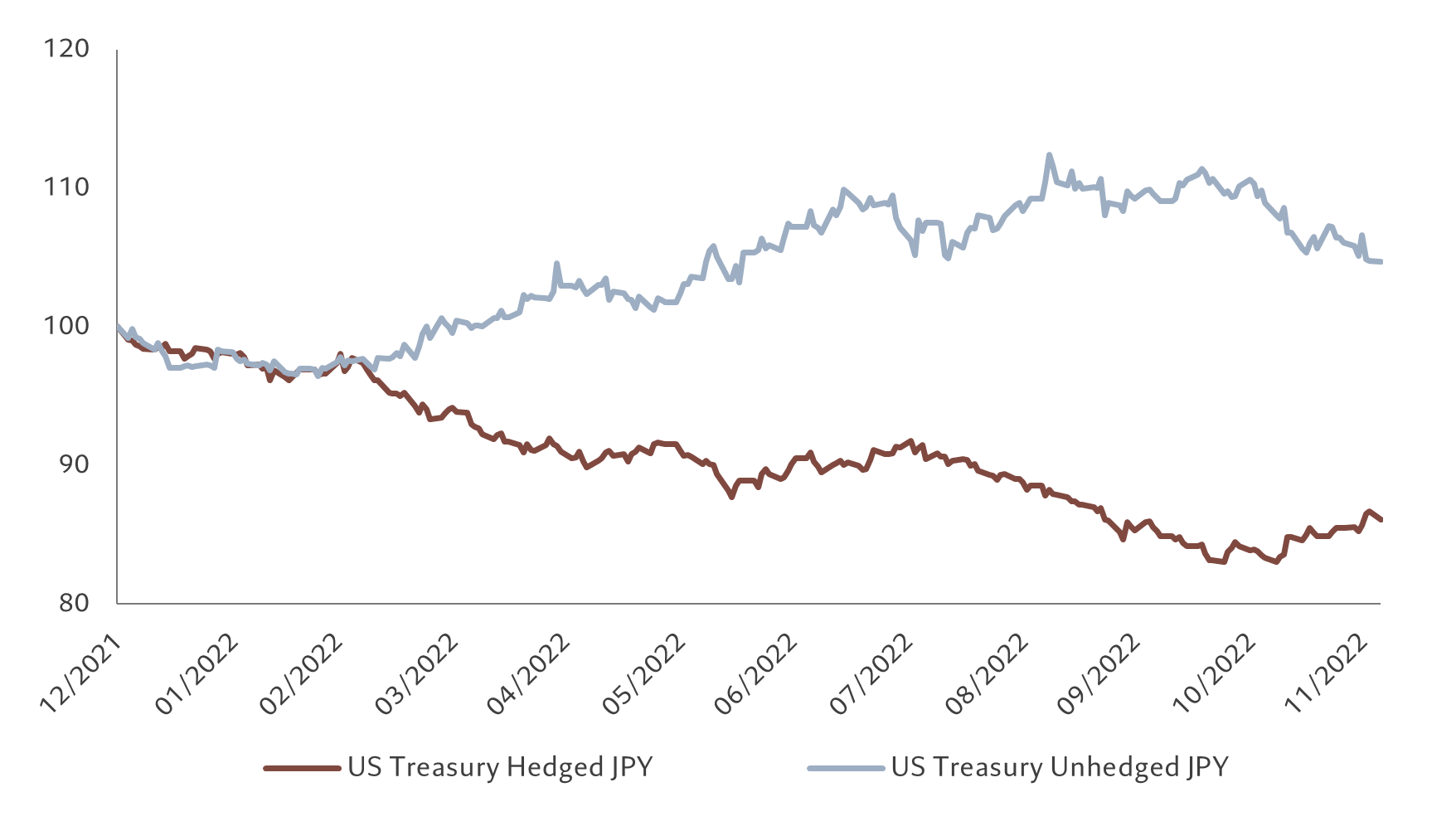

For Japanese investors in US Treasuries, currency hedging didn’t make a big difference in performance in the first couple of months of this year (see Fig. 3). But as the dollar appreciated significantly against the yen, non-hedged investments outperformed their hedged counterpart.

Fig. 3 Brutal moves

Performance of US Treasuries, based in JPY, hedged vs unhedged, indexed

Bloomberg US Treasury Total Return Index Hedged JPY. Source: Bloomberg, data covering period 31.12.2021 – 05.12.2022

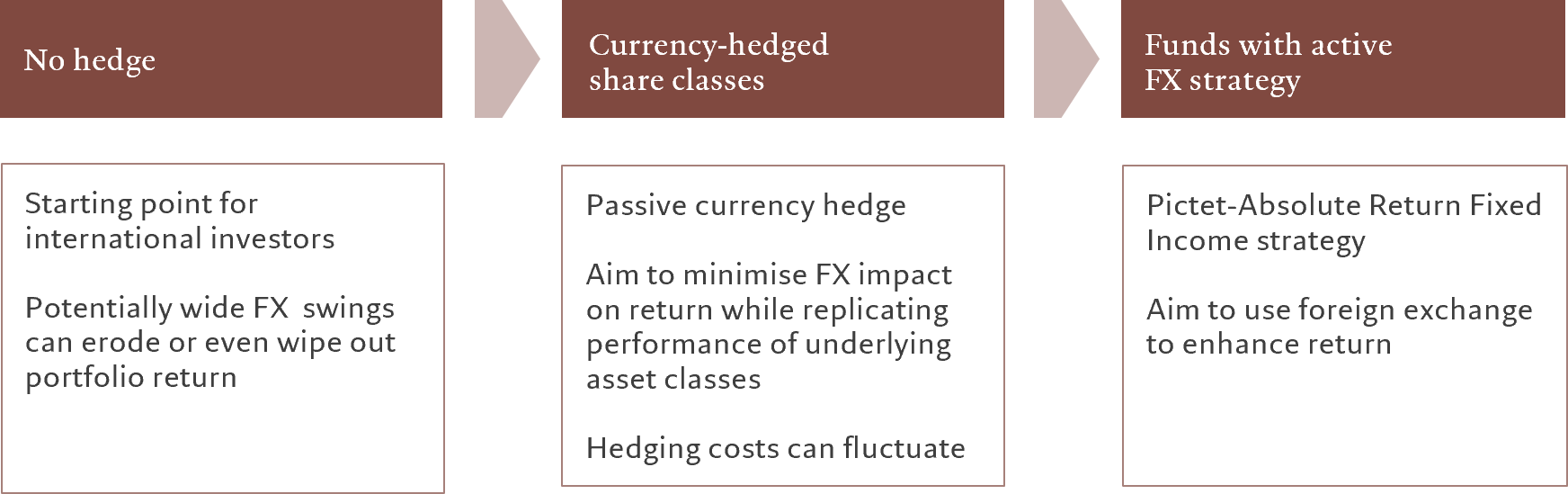

Currency hedging choices

There are various ways for investors to manage their currency exposure (See Fig. 4).

Fig. 4 Currency hedging at a glance

Source: Pictet Asset Management

A popular option is to outsource the task of currency hedging to a third party, typically the fund administrator, via currency-hedged share classes.

Currency-hedged share classes aim to minimise the impact of currency swings on the portfolio return.

Investors get peace of mind, in exchange for a fee that works much like a premium on an insurance policy.

Such vehicles allow investors to gain access to types of investment that aren't traditionally available in certain currencies – such as emerging market debt in euros or US high yield bonds in the Swiss franc.

Investors who have a strong conviction in the future trajectory of their base currency can easily switch from one share class to another, while staying fully invested in the underlying asset class.

It is important to remember, however, that currency-hedged share classes cannot completely eliminate the risks associated with movements in exchange rates. The cost of currency hedging for can fluctuate too (see Fig. 5), which also has an impact on portfolio returns. The cost of a currency hedged investment vehicle has three components to it.

Interest rates: a currency hedge uses instruments known as foreign exchange forwards. These are contracts in which two parties are obliged to exchange a pre-determined fixed amount of (foreign) currency for another (base) currency at a specified future date. The cost of these contracts – or the future exchange rate at which the transaction takes place – is primarily determined by the difference in the interest rate of the base currency and the foreign currency. This pricing mechanism dictates that the currency with the lowest interest rate will change hands at higher exchange rate in the future. So, if interest rates in the US and euro zone were exactly the same, the hedging cost would be close to zero and a EUR-hedged share class of a portfolio of US bonds would return the same as its USD counterpart. But if US interest rates were to rise and those in the euro zone were to fall, the currency hedging cost would rise for EUR-based investor.

Admin fee: investors are required to pay the cost of managing a hedged share class, typically 5 basis points per year. This is usually incorporated into the fund administration fee.

Transaction costs: market spreads, known as euro/dollar basis swap, mean there is a cost to enter into spot, forward or swap contracts. The more illiquid a currency pair, the higher the cost. Transaction costs typically rise towards the year end due to thin liquidity.

Example of an active approach

Many global bond portfolios treat currencies as distinct sources of return and risk. They deploy what are known as currency overlay strategies to benefit from both long and short-term trends in the foreign exchange market as well as swings in currency hedging costs.

Pictet Asset Management runs a number of fixed income strategies that actively manage currency exposure in this way. Broadly speaking, our aim is to identify and invest in unjustifiably cheap currencies to enhance portfolio returns.

For example, our emerging fixed income strategies took underweight positions in central European currencies in the third quarter of 2022 as they came under most pressure from high inflation and the European gas supply issues. At the same time, they were overweight in selected Latin American and Asian currencies. These positions contributed positively to the portfolio’s return.

In more recent months, they have started to unwind these positions to take a more neutral view on emerging currencies as the Federal Reserve appeared closer to the end of its tightening campaign, while keeping some underweight positions in selected central European currencies.

Investment managers of the Pictet-Emerging Local Currency Debt strategy, meanwhile, made investments in the Argentine peso in the latter part of 2018 in the belief the currency was due a sustained rebound after its recent sharp fall. The currency investment contributed positively to the portfolio's return as the peso gained nearly 10 per cent against the dollar in the final three months of 2018.

Currency hedging: blessing and curse

What’s less well understood about the foreign exchange market is that the mechanics behind the calculation of currency forwards can, at times, render certain bond markets completely out of bounds for foreign investors.

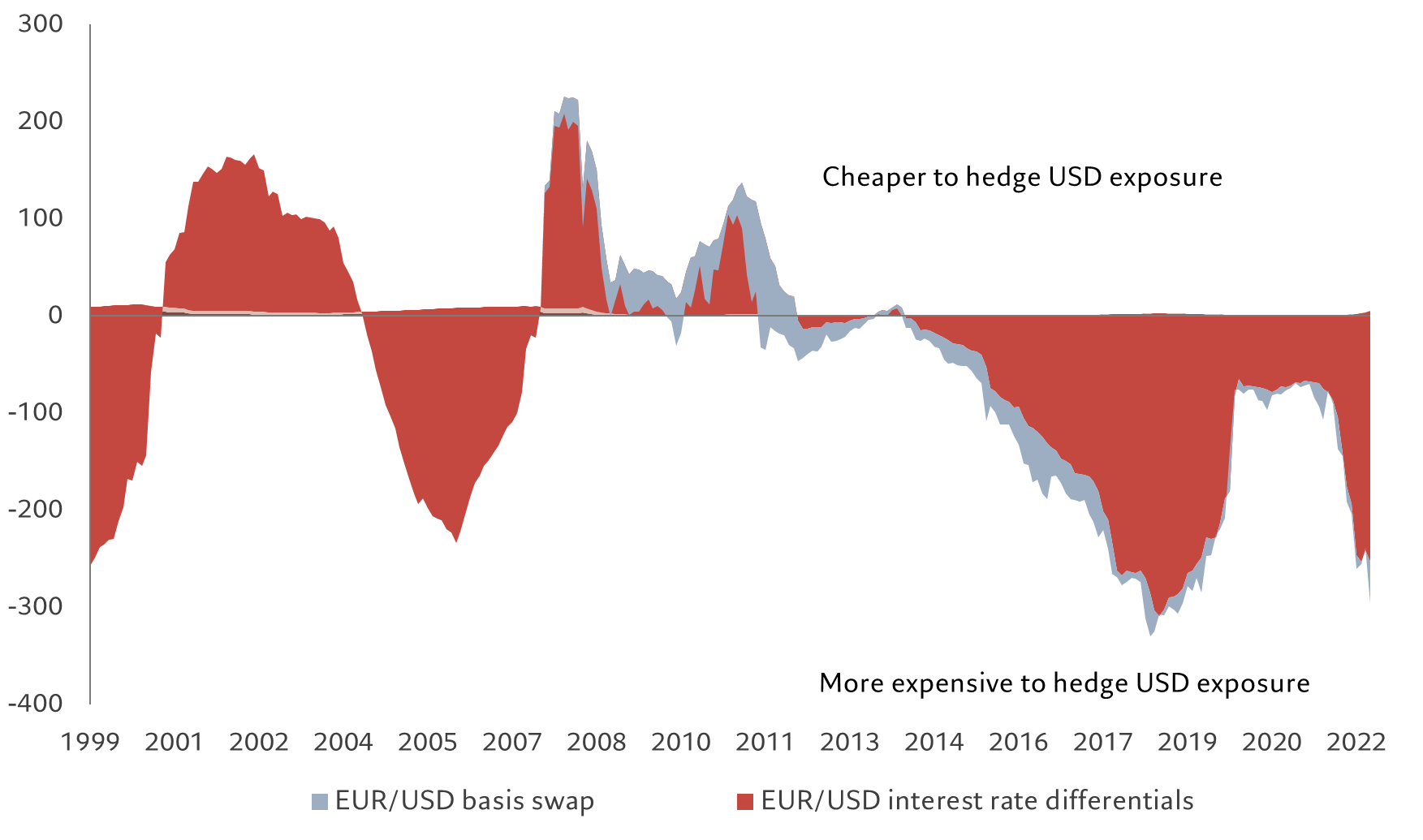

That’s currently the case for euro-based investors looking to invest in US government bonds. Because US interest rates have been rising faster than those in the euro zone, the cost of hedging a 10-year US government bond, currently yielding some 3.70 per cent, into euro has risen to prohibitively expensive levels (see Fig. 5). Using a EUR/USD currency hedge in this instance would take the effective yield of the note to levels below zero. By comparison, the 10-year German government bond yields around 1.7 per cent. While this quirk is problematic for euro-based investors, it is a represents a potentially rich source of return for dollar-based investors, who effectively receive a premium when the hedge any euro-denominated bond investments back into the dollar.

Exchange rate fluctuations, then, can greatly impact the return from fixed income portfolios. If you thought currencies were a zero sum game, think again.

Fig. 5 cost breakdown

Average cost of currency hedging in EUR/USD (in basis points, annualised)

*Difference between three-month USD Libor and Euribor **Euro/dollar 3-month cross-currency basis swap. Source: Bloomberg, Pictet Asset Management, data covering period 31.12.1999 – 30.09.2022

Mickael Benhaim joined Pictet Asset Management’s Fixed Income team in 2006 and is the Head of Fixed Income Investment Strategy & Solutions. Prior to assuming this role in April 2017 Mickael was Co-Head of Global Bonds. Before joining Pictet he was Head of Euro Aggregate Fixed Income for AXA Investment Managers where he worked for five years. Mickael has more than 20 years professional experience that includes working at the Dresdner Group and BNP Paribas Group. Mickael holds a MSc in Mathematics and a post-graduate degree in stochastic models from the University of Paris Jussieu and Paris Panthéon-Sorbonne.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.