Asset allocation: central banks set to disappoint investors

The global economy continues to count the cost of the trade war but most investors seem convinced that central banks will ride to the rescue with aggressive monetary stimulus. We don’t share their optimism.

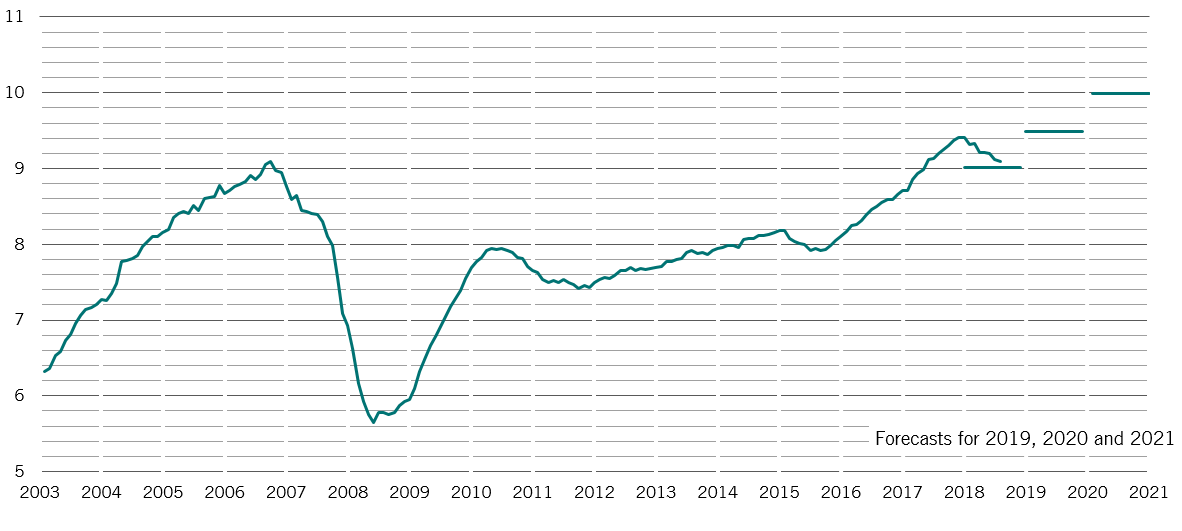

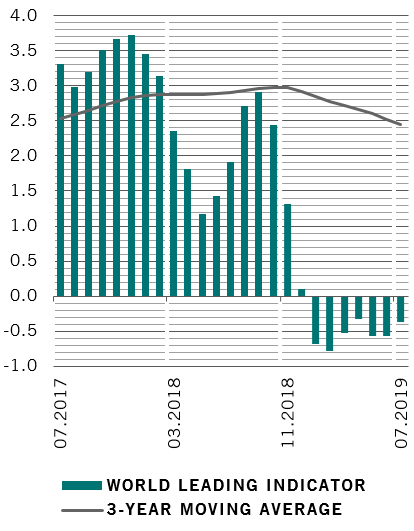

Our leading indicators point to subdued global growth in the coming months as uncertainty from trade tensions hits industrial production and business sentiment, especially in developed economies.

What is more, corporate earnings growth should grind to a halt this year after a stellar 2018.

Although we expect central banks to ease monetary policy to arrest the economic slowdown, policymakers are unlikely to deliver the sort of stimulus the market is currently discounting.

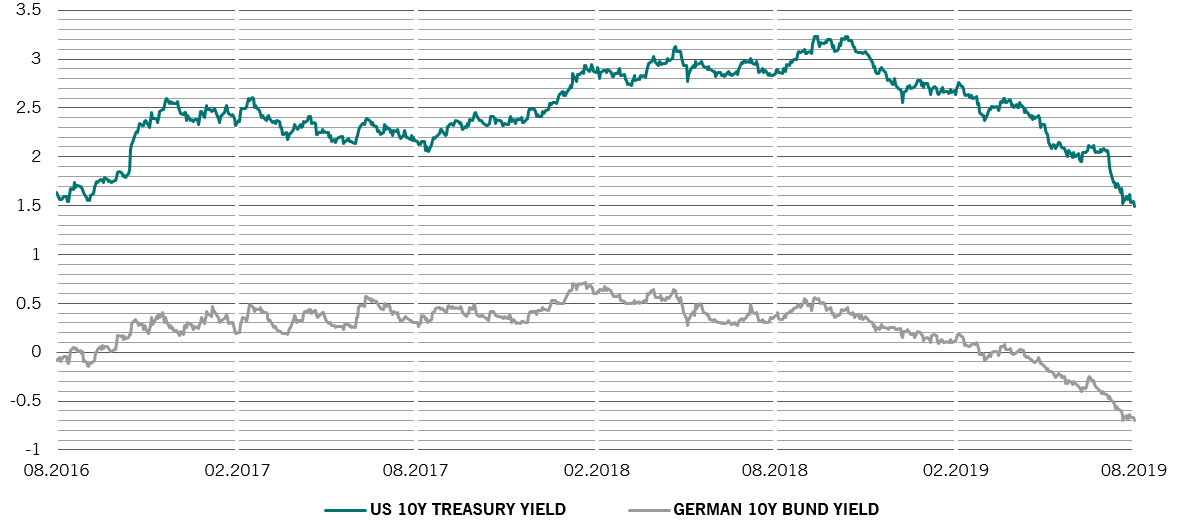

Against this background, we remain underweight equities. At the same time, we have more reasons to keep our cautious stance on bonds now that this year’s rally – the strongest in 20 years -- has pushed the yield on nearly a third of the global bond universe below zero1. We maintain our overweight in cash.

Our business cycle analysis shows global economic growth is likely to slow to an annualised 2 per cent this year from 3.4 per cent in 2018, with developed economies suffering most. Business sentiment, as measured by the Purchasing Managers Index, has fallen below the critical 50 threshold, the lowest since 2012, while industrial production in developed economies is contracting for the first time since 2016.

While the outlook for export-oriented sectors is gloomy, consumers are not tightening their purse strings yet. Globally, consumer sentiment is at a record high, supported by a strong labour market and falling mortgage rates. For these reasons, we think the probability of a global recession is lower than consensus estimates of around 30-40 per cent.

World Leading Indicator*

Liquidity indicators support our cautious stance on stocks. Even though the US Federal Reserve cut interest rates in July, the volume of new liquidity provided by global monetary authorities has contracted at a rate of 0.5 per cent in the past six months. This is primarily down to developments in China, where the central bank is implementing measures to reduce corporate indebtedness. We think monetary conditions will ease somewhat in the coming months, given that the Fed is expected to cut interest rates again and the European Central Bank is set to announce fresh bond buying worth EUR600 billion later this month. Still, we think investor expectations that the world’s central banks would provide a monetary stimulus of as much as USD1.5 trillion over the next year are wide of the mark2.

Our valuation model shows that some equity markets, notably the US and Switzerland, continue to be expensive. A decline in capital spending and uncertainty over the outcome of the trade war have weighed on corporate earnings, with the US Bureau of Economic Analysis cutting its 2018 corporate profit calculations by 8.3 per cent, wiping USD188 billion from the previous tally.

Europe, in contrast, is becoming attractive as corporate earnings stabilise and bond yields fall. The equity risk premium – an estimate of how much return stocks provides over the risk-free rate – has in Germany shot up above 9 percentage points for the first time ever. Valuations for emerging markets are also attractive, especially in Asia, where the price-earnings ratio is a modest 11. Japan has shown a remarkable resilience in the face of a rising yen; given the market's favourable valuation, there is the potential for Japanese stocks to rise by as to 20 per cent over the medium term.

Industry sectors most sensitive to the economy – industrials and IT stocks – continue to look expensive, trading at a premium of over 12 per cent relative to their defensive counterparts such as consumer staples and pharmaceuticals.

Our technical indicators are neutral for stocks, but are flashing red for those defensive assets that have rallied strongly in recent months, such as the yen and government bonds.