Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Capitalising on currencies to boost EM returns

Economics and valuations point to EM currency appreciation this year potentially offering investors an extra source of returns.

Written by

Patrick Zweifel

Chief Economist

Fixed income investors ignore exchange rates at their peril. They have the power to either erode or enhance the returns on an overseas bond portfolio. Which is why, in our emerging market debt strategies, we embrace them as separate sources of both risk and return.

Each currency, of course, has its unique drivers and the foreign exchange market overall is known for bouts for volatility. However, taking a medium-term view, we see the potential for broad-based appreciation of EM currencies versus the US dollar, providing a lift to total returns from local currency debt.

Going for growth

Emerging markets are traditionally associated with faster economic growth than their developed peers – after all, they usually have some catching up to do in terms of wealth.

Recently, that growth premium has widened to 270 basis points from a low of 170 basis points in 2015.

The gap is likely to increase further in coming months for two key reasons. First, emerging markets are particularly well placed to benefit as a ramp-up in the investment cycle boosts global trade. According to our models, a 1 per cent increase in cross-border flows lifts EM economic output by 0.26 percentage points. The impact on developed world activity is about half as much.

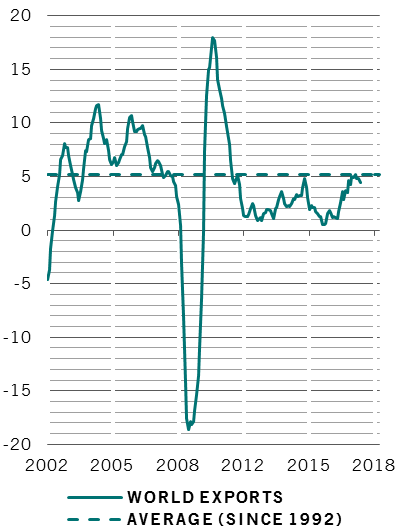

powered by exports

World export growth (% Y/Y, 3-month moving average)

Global exports rose by 4.4 per cent in 2017 (see chart). That’s the fastest pace since 2011, but still below their multi-decade trend, potentially leaving scope for further acceleration. In fact, we expect that export growth will overshoot the long-term average of 5.1 per cent before peaking, as it has done in previous cycles.

Moreover, commodity and energy prices look well supported as global economic growth remains strong. This should boost those commodity-producing emerging markets.

Over the next five years, we forecast that annual EM growth will average 4.6 per cent – 300 basis points higher than that of the developed world.

This could prove to be good news for emerging currencies. Historically, the differential between EM and DM real GDP growth has displayed a strong correlation with the exchange rate, with a six-month lag. The wider the growth gap, the weaker the US dollar against a basket of EM currencies.

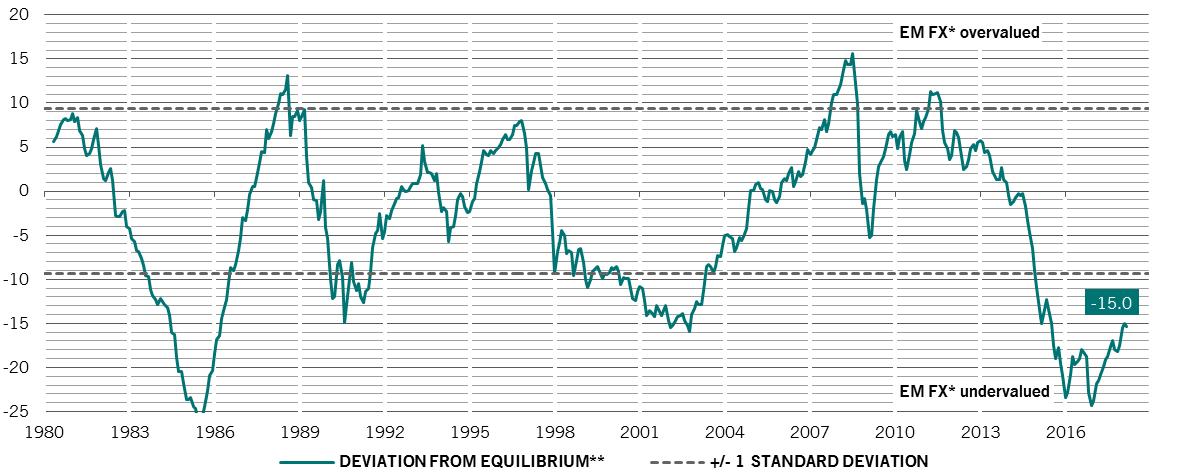

The value view

This time round, the case for currency appreciation is strengthened by very attractive valuations.

According to our models, EM currencies are currently 15 per cent undervalued against the US dollar. They are also trading at some of the cheapest levels seen over the past two decades (see chart).

undervalued

EM currencies: over (+) and under (-) valuation vs USD (%)

Source: Pictet Asset Management, CEIC, Thomson Reuters Datastream. Data covering period 01.01.1980 - 01.03.2018.

We also have inflation on our side. The inflation differential between emerging and developed nations is at its lowest level in recent history (at 140 basis points), offering further support to the exchange rate.

Of course, emerging markets span a very diverse universe of countries, which in turn have many different individual circumstances and drivers for their economies, exchange rates and bonds. So any general potential appreciation of EM currencies will likely have some specific exceptions. And even for those currencies which do appreciate, short term bouts of volatility and corrections cannot be ruled out, given the nature of the asset class.

The broad trend of appreciation, however, should remain intact. For EM debt investors, that creates an opportunity to further maximise returns by taking active positions in the currencies against their benchmark.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.