Asset allocation: balanced forces

Strong corporate earnings, steady economic growth and the lack of fallout – so far – from trade wars are helping to mitigate the US Federal Reserve’s steady withdrawal of liquidity from the global system.

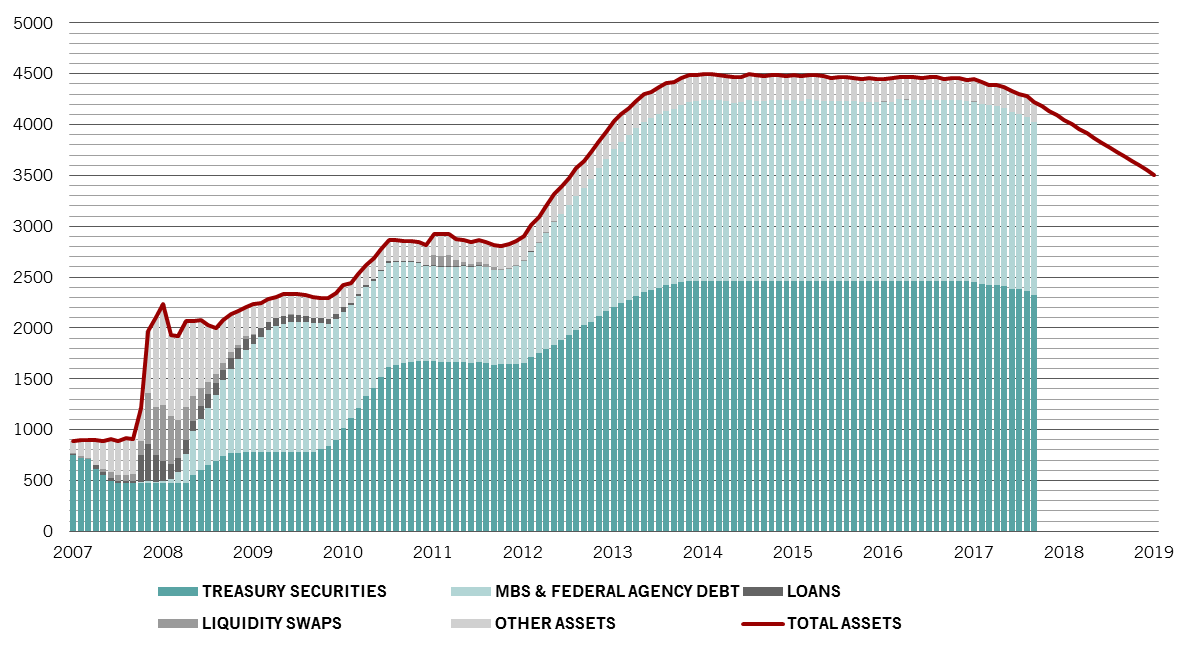

The tension between these opposing forces is likely to continue for the coming months. The pace at which the Fed’s balance sheet is due to shrink hits a peak in early October, while the European Central Bank’s asset purchase programme is coming to an end this year.

And although corporate earnings continue to grow, there are signs momentum could be slowing – perhaps unsurprising given the pace at which profits were previously expanding.

October 2018

Countering this is the US’s fiscal stimulus programme, which hits full throttle in the first quarter of 2019 and the tempering of the Chinese government’s push to deleverage the economy after signs growth was starting to flag.

Taking these offsetting factors into account, we are maintaining our neutral weightings on the three main asset classes, equities, bonds and cash.

Our global business cycle indicators are tilting positive. Our generally upbeat reading of the US economy is balanced against concerns about trade tensions and the impact tightening monetary policy is beginning to have on interest-rate sensitive industries, particularly construction and residential investment.

China’s leading indicators, meanwhile, have rebounded from weakness earlier this year. A drop in car sales is likely to be the temporary effect of ending sales incentives. And weak infrastructure spending is offset by growth in private housing. Besides, the government is likely to boost infrastructure investment should the economy falter.

Our global liquidity readings remain neutral. Monetary tightening and a slowdown in private credit creation in the US is being offset by massive liquidity flows into the country from the rest of the world. That’s not just a matter of repatriation of US corporate cash from abroad. Investors worldwide are focused on strong US corporate earnings, a strong dollar and the prospect of rising US bond yields. These flows help explain why the US equity market has been so robust this year while those in the rest of the world have struggled.

US Federal Reserve balance sheet, actual and forecast, USD billion

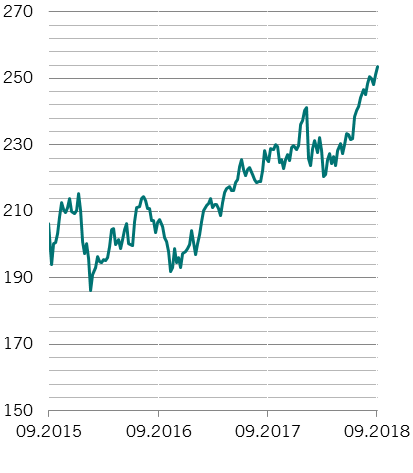

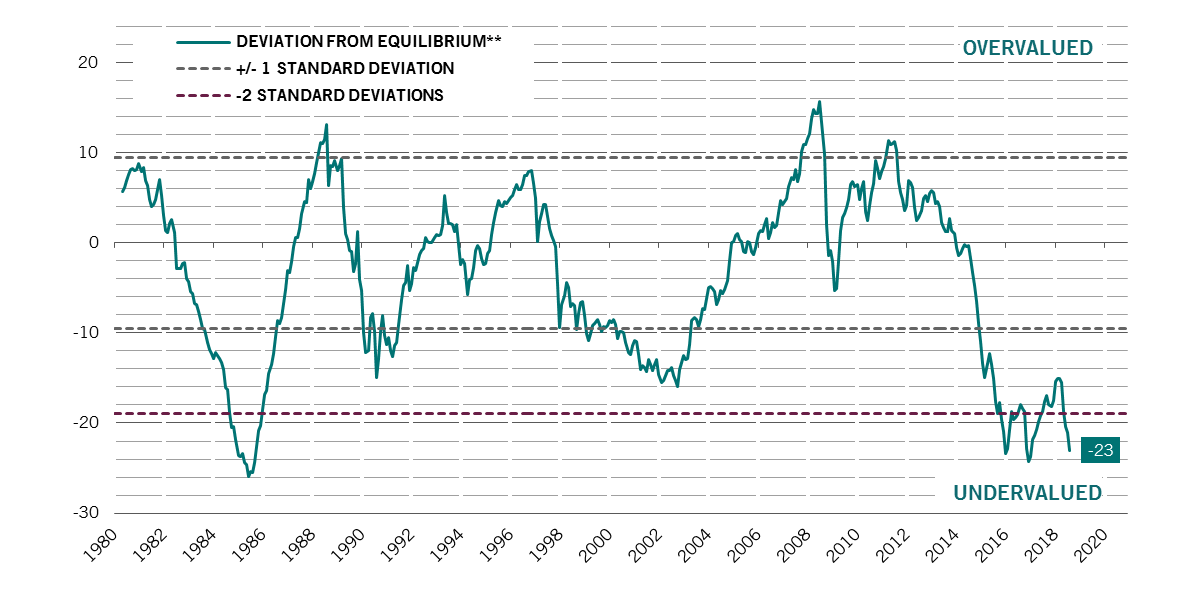

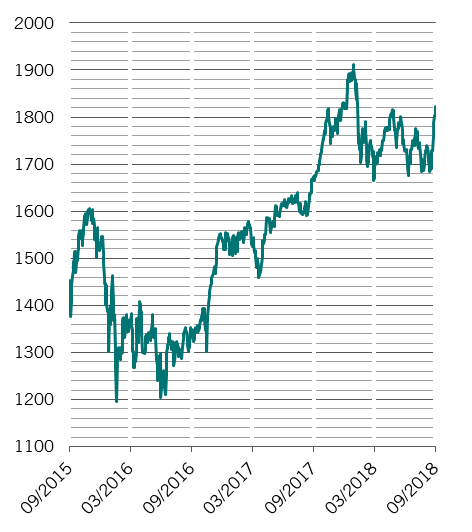

Our valuation metrics show that global equities are in neutral territory, albeit with large valuation gaps within the asset class. Global bonds are looking slightly less expensive - but still overvalued. Emerging market (EM) local debt isn’t as quite as cheap as it was last month, though with EM currencies still 20 per cent undervalued against the dollar, they’re still attractive. Corporate bonds, especially in Europe, are expensive and carry lower credit ratings, on average, than in the past.

From a technical standpoint, seasonal factors strongly favour equities across all regions apart from emerging markets, while Japanese stocks look overbought. The technical picture for EM assets is mixed: on the one hand, investment flows seem to be stabilising, but, on the other, the degree to which these flows are dispersed across developing countries' markets remains poor. One point worth noting is that using the VIX to hedge against volatility in other asset classes hasn’t worked lately as the correlation among the returns of different asset classes has been unusually high.