Asset allocation: risks evenly balanced

Investors heading into summer had no shortage of worries as escalating trade tensions threatened to hit corporate profits and derail the global economy at a time when major central banks were draining monetary stimulus.

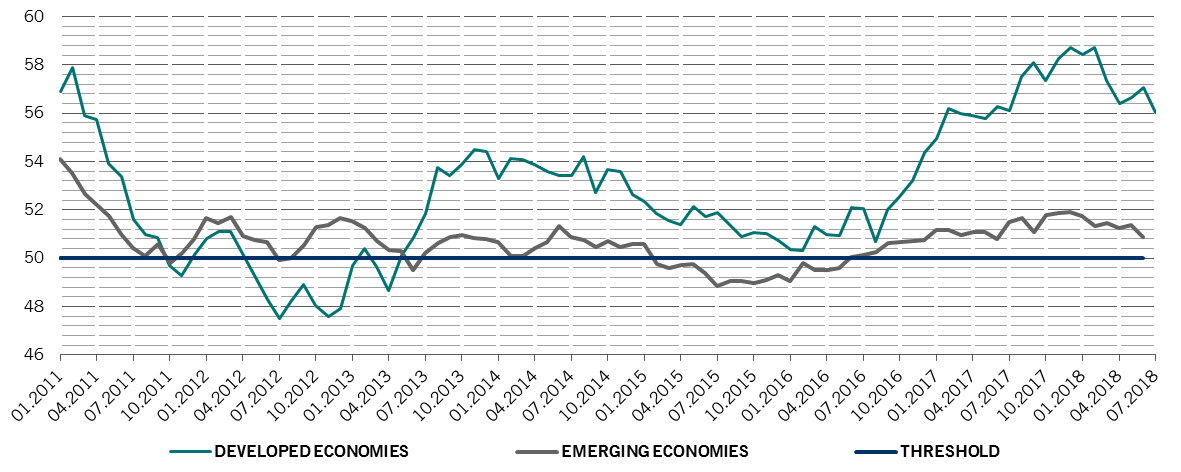

However, their worst fears failed to materialise. The global economy remains resilient, supported by a buoyant US and euro zone, while companies worldwide continue to report healthy profits, even though their earnings growth may be plateauing. Monetary conditions also remain accommodative, with real interest rates in advanced economies standing at -0.9 per cent1. At the same time, the crises engulfing Turkey and Argentina have so far been largely contained, while monetary easing in China has helped stabilise the rest of the developing world, offsetting the impact of US import tariffs.

For all this, we feel it is too early to raise our allocation to equities from neutral to overweight or change our neutral stance on bonds – our liquidity and valuation indicators suggest caution is warranted.

September 2018

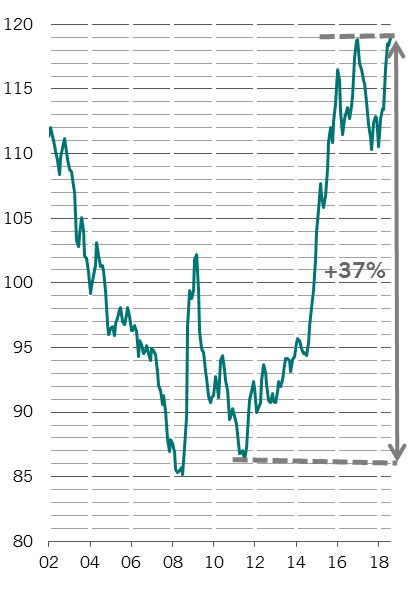

Purchasing Managers Survey for developed and emerging economies

The US economy seems to be reaccelerating, supported by robust private consumption and labour market conditions. The only area of softness is in the housing market, which appears sensitive to changes in the cost of borrowing.

We still expect the US Federal Reserve to raise interest rates twice more this year, which would take the benchmark rate towards what is considered to be a neutral territory – neither expansionary nor stimulative. Beyond this point, however, we’re not convinced the Fed will carry on hiking.

Economic conditions in the euro zone are stabilising, where falling unemployment and improving sentiment are supporting consumption.

More substantial improvements can be seen in China, where our leading indicator hit its highest in at least two years thanks in part to stronger construction activity. A fall in the yuan – its trade-weighted basket is 1-2 per cent below its central parity – has helped support the country’s exports despite ongoing trade rows with the US.

Our liquidity readings remain neutral, supporting our stance on both bonds and equities. The People’s Bank of China’s monetary easing has lifted the country's total liquidity flow to 6.3 per cent of GDP, near its 10-year average, from 4.9 per cent2. This has helped offset tighter liquidity conditions in the US. While we don’t expect the PBOC to abandon its campaign of reducing private sector debt, the stimulus should help support Chinese growth for the time being.

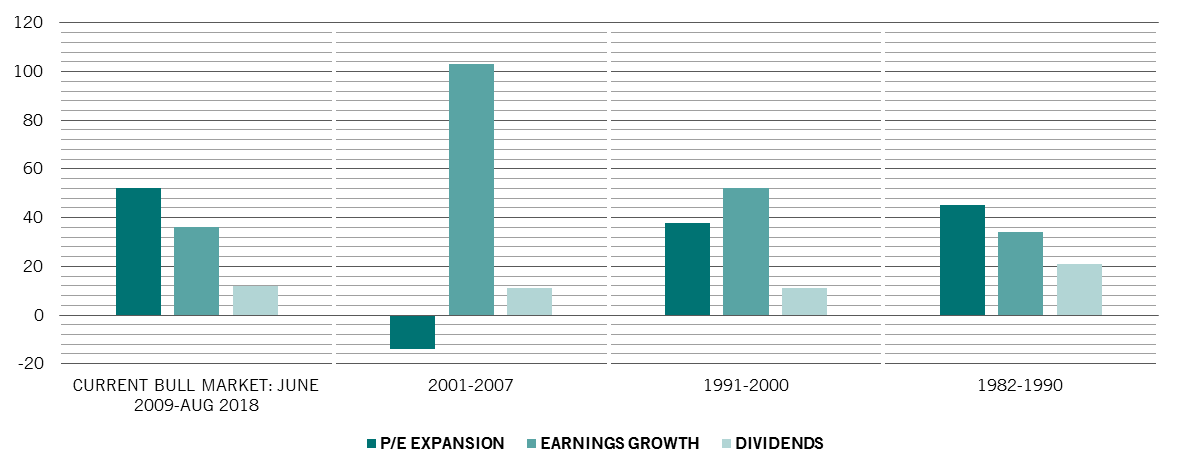

Valuation metrics are also neutral for equities overall although this masks major divergence between regions and sectors. The US remains the most expensive region and US companies are unlikely to repeat their blockbuster earnings performance of the second quarter. And, as we expected, we have seen the beginning of an investor rotation away from cyclical stocks into defensive ones – the premium at which cyclical stocks trade over their defensive counterparts now stands at 23 per cent on a cyclically-adjusted price-earnings basis, down from a record 30 per cent but still far above the long-term average of 10 per cent.

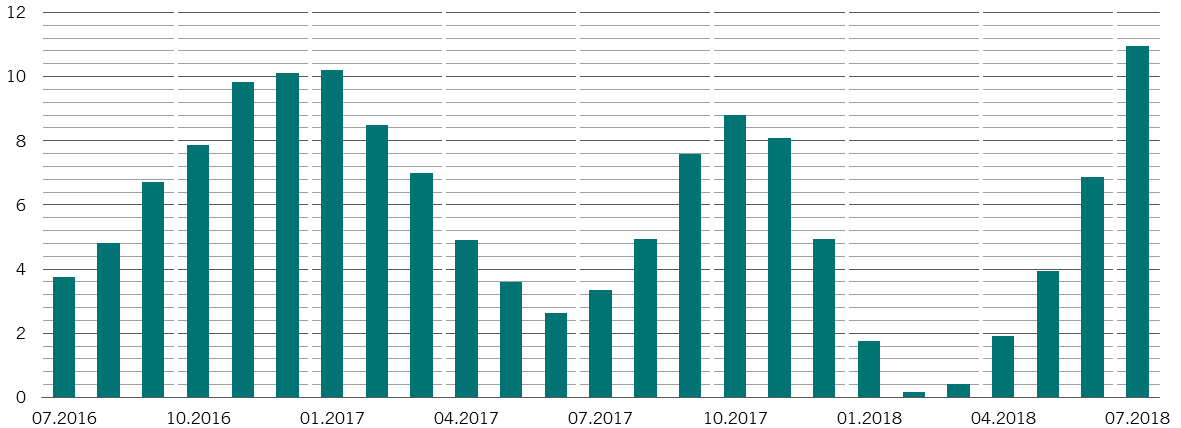

Technical gauges have improved slightly for equities, especially for defensive sectors such as healthcare. Encouragingly for stock investors, the rally in the equity market has broadened, with a greater number of industry sectors participating in it. The technical picture for emerging market (EM) stocks is also improving. The gauges we monitor show that flows out of EM assets are slowing even if the Turkish lira crisis led to outflows of USD1.4 billion in the week to August 15, according to the Institute of International Finance.