Four reasons why Russia will shrug off the latest round of US sanctions

We look at why the latest US sanctions are unlikely to be as harmful for Russia as the 2014 ones reinforcing the investment case for Russia.

Written by

Patrick Zweifel

Chief Economist

Nikolay Markov

Senior Economist

Share this article

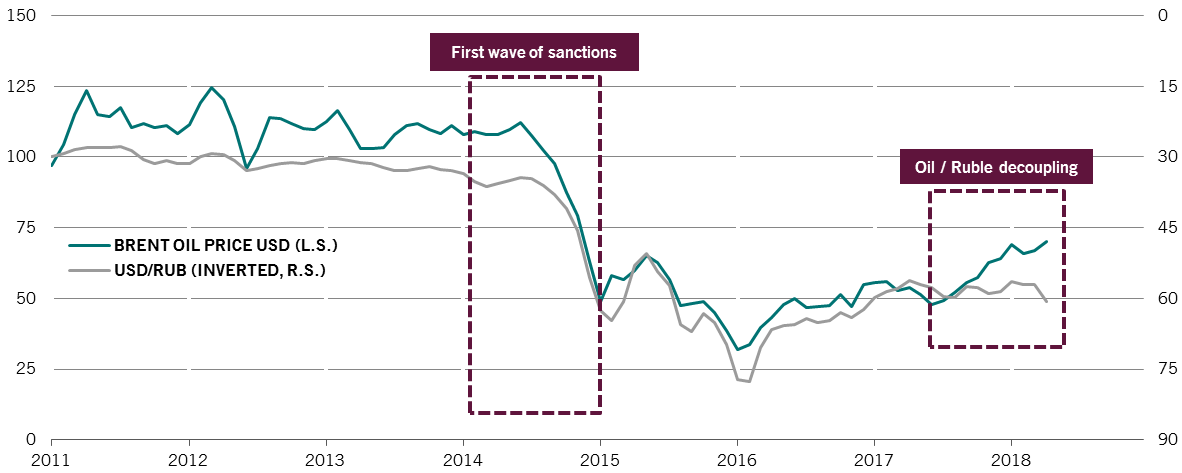

1. Decoupling between oil prices and the ruble

US sanctions in 2014 occurred at a time when both oil prices and the ruble were declining. This time, rising oil prices have decoupled from a falling ruble (Fig.1). This is exceptional.

Fig.1 - Oil price & ruble exchange rate

Source: Pictet Asset Management, CEIC, Datastream. Data as of May 2018.

Strong global demand and an extension of the OPEC production cut have lifted oil prices.

Meanwhile, the already undervalued ruble acted as shock absorber of the new sanctions, depreciating 6.2 per cent in April against the US dollar, but just 0.3 per cent in nominal trade-weighted terms1.

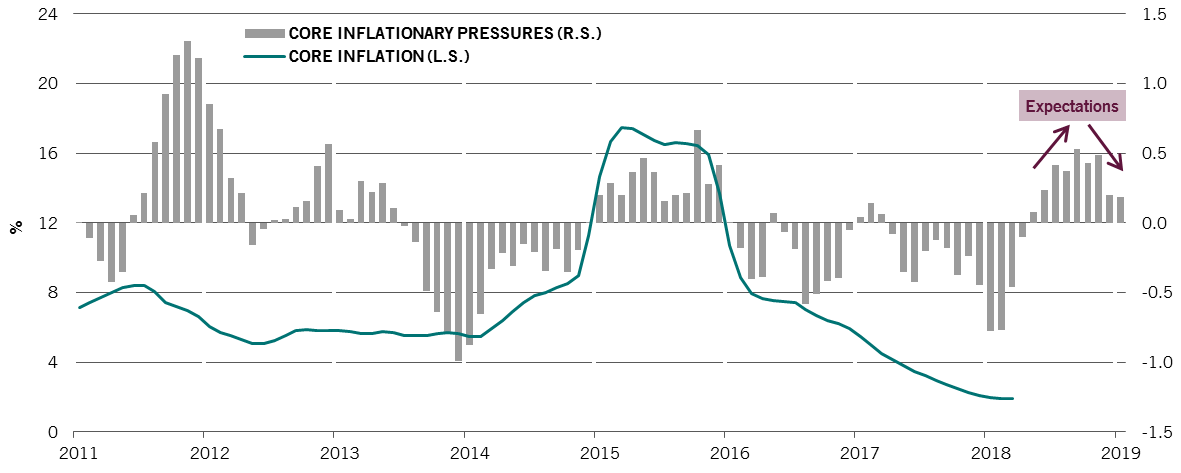

2. Contained inflationary pressures

Short-term inflationary pressures have increased but we expect them to fade towards the end of the year and into early 2019 (Fig.2 below).

Source: Pictet Asset Management, CEIC, Datastream. Data as of May 2018.

Although moderate, inflationary pressures are likely to impact monetary policy, marking a pause in the current easing cycle and implying more limited interest rate cuts in 2018.

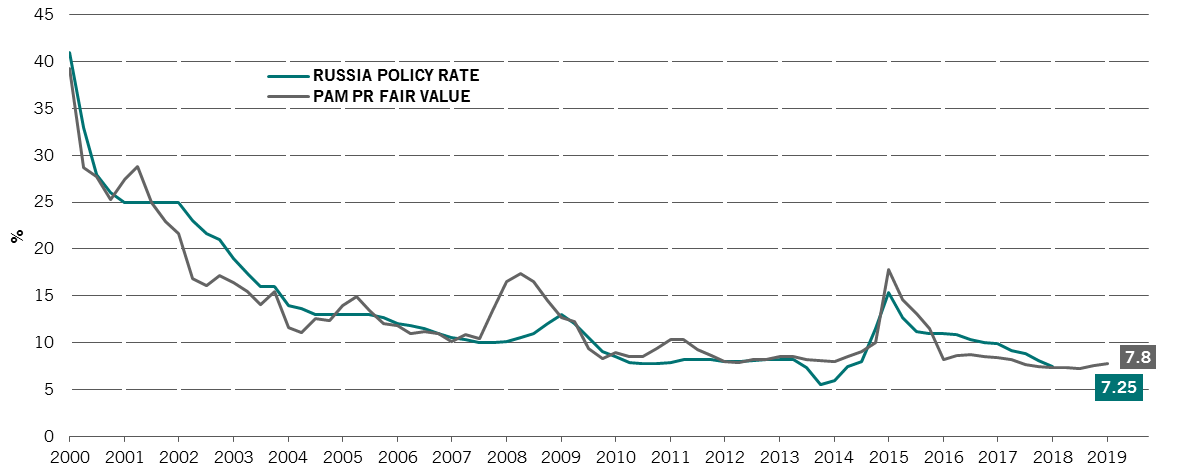

The current policy rate of 7.25 per cent is in line with our estimate of fair value (Fig.3). It leaves limited room for interest rate cuts in 2018, especially given the need to reduce households’ inflation expectations. These remain above target at 7.8 per cent according to the latest Central Bank of Russia (CBR)’s survey in March and may increase due to the sanctions.

Fig.3 - Russia policy rate & fair value (Q2 2018)

Source: Pictet Asset Management, CEIC, Datastream. Data as of May 2018.

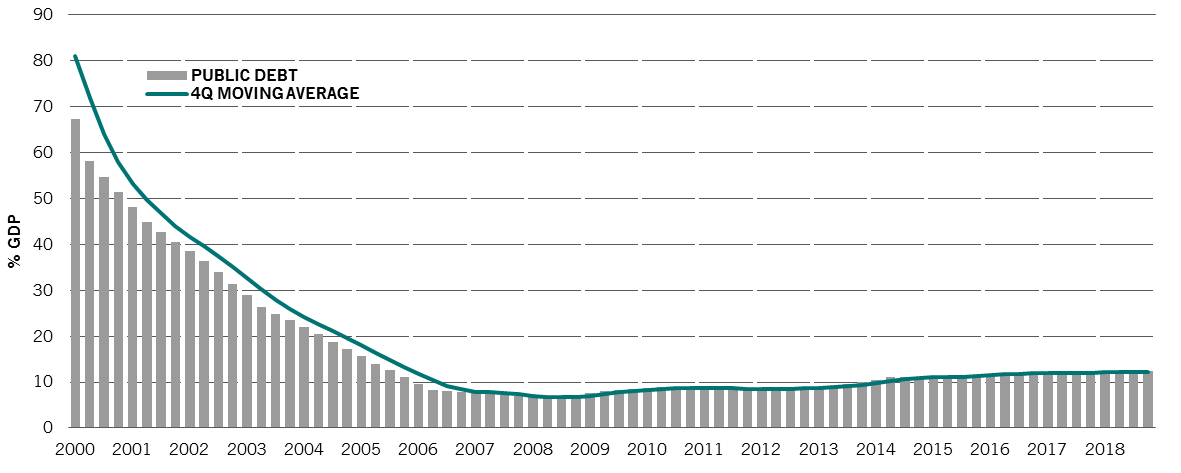

3. Russia’s economic strength

As illustrated in Fig.4, Russia’s public finances are in excellent shape. As a net creditor vis-à-vis the rest of the world, the country also runs a large current account surplus which provides a sufficient cushion to absorb the sanctions impact.

Fig.4 - General government debt to gdp ratio

Source: Pictet Asset Management, CEIC, Datastream. Data as of May 2018 with expectations to the end of the year.

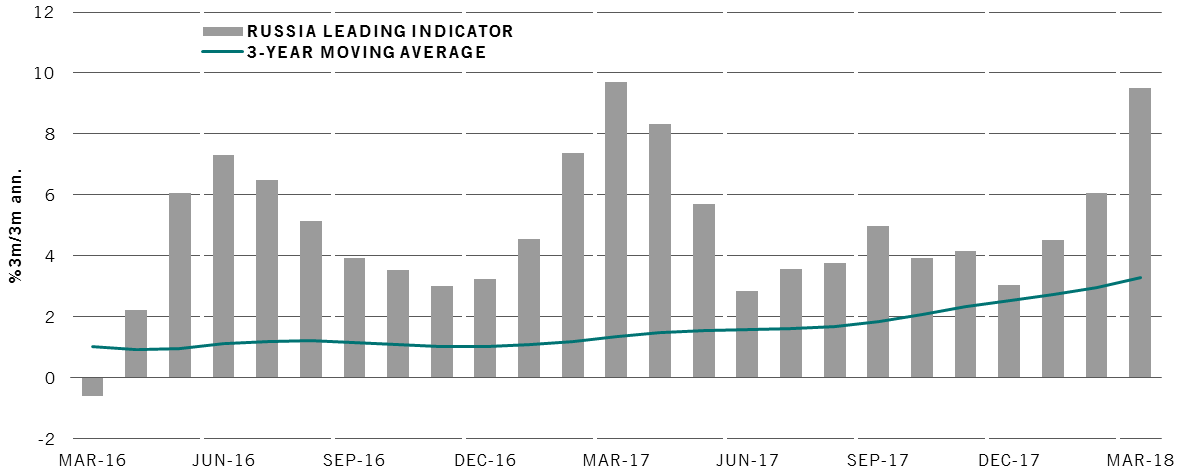

Our leading indicator also points to strong GDP growth ahead (Fig.5), driven by the energy sector, as well as improving labour market and industrial production.

Fig.5 - Pictet sequential leading index growth

(%3m/3m ann.)

Source: Pictet Asset Management, CEIC, Datastream. Data as of May 2018.

4. Football world cup

By boosting spending, the football World Cup in June should also help counterbalance the sanctions.

Fig.6 - Football world cup in russia - a few figures

Source: Pictet Asset Management, Reuters, The Guardian. Data as of May 2018.

*We expect the bulk of the contribution to GDP to be concentrated over the last 4 years to the World Cup.

CHART OF THE MONTH BY OUR EMERGING CORPORATE BONDS TEAM

By Karen Lam, Senior Client Portfolio Manager

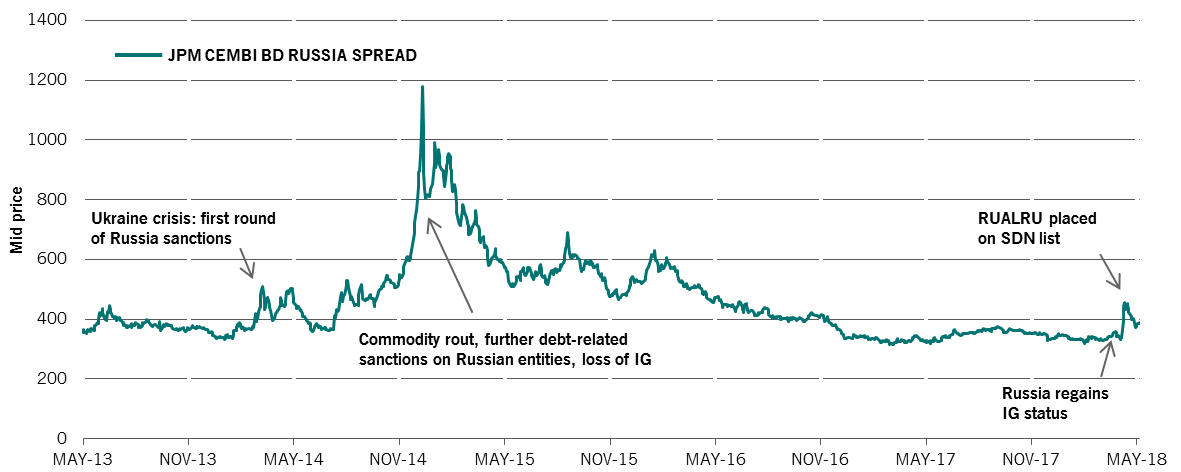

Russia’s strong position can also be observed in the corporate bond space. Russia index spreads, as represented by the JPM CEMBI BD Russia index, have only widened by c.60 basis points since the sanctions were announced.

We do not think that Russian eurobond prices will deteriorate significantly from the current levels because the original panic seems to have faded and the market is relatively small and shrinking, with limited scope for new supply. In fact, we believe demand from local investors will absorb any supply from forced US sellers, thus providing further support for the market.

Fig.7 - JPM CEMBI BD RUSSIA spreads

Source: Pictet Asset Management, Bloomberg. Data as of May 2018.

CHARTS OF THE MONTH BY OUR EMERGING MARKETS EQUITY TEAM

By Hugo Bain, Senior Investment Manager

and Christopher Bannon, Senior Investment Manager

Russia - all about the equity risk premium

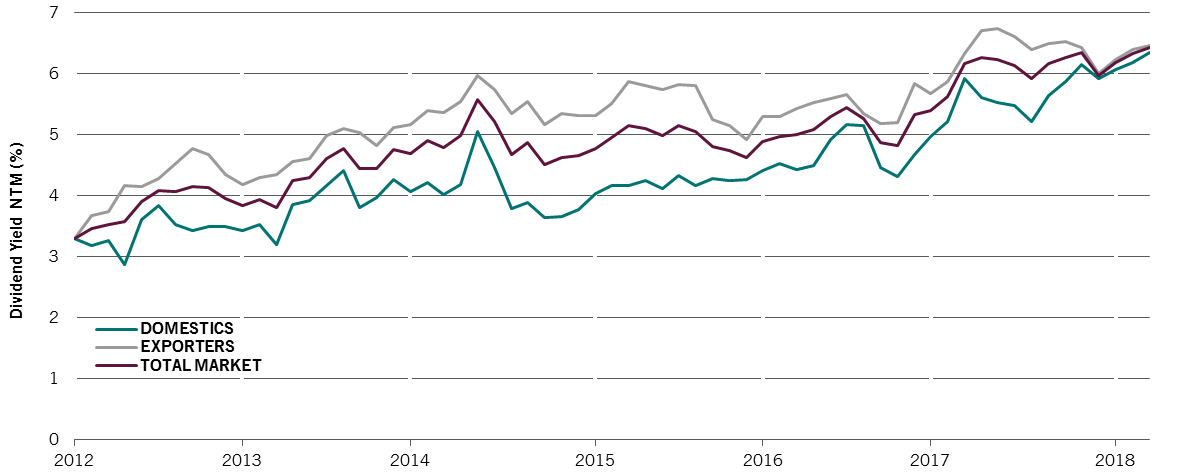

In the same way as Russia is proving strong faced with the latest US sanctions, the country’s companies are showing resilience. Forced to decrease their reliance on western capital over the past years, we believe this trend will continue, despite many of them already having no debt at all.

We also think that they will continue to pay dividends which, in the case of some companies, are at extraordinary levels. As Fig.8 shows, Russian companies are already offering record high dividend yields. Unlike the previous crisis in 2015, both domestic firms and exporters are offering high dividend yields, indicating all parts of the market are attractive.

Fig.8 - Russian companies returning record high yields

Source: Pictet Asset Management, MSCI Russia 10/40, Bloomberg. Data as of May 2018.

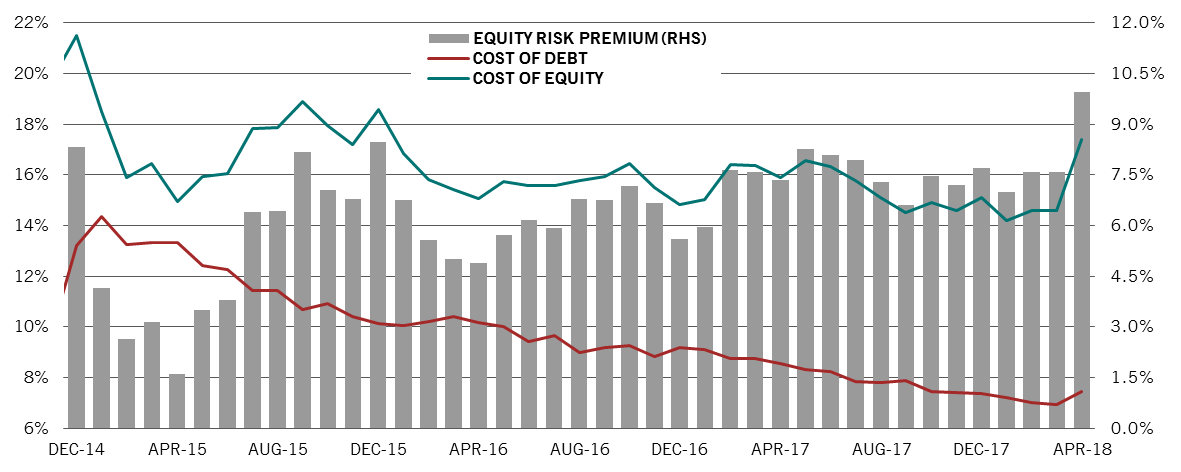

We suspect we may be at ‘peak sanctions’, and even a minor contraction in the Russian equity risk premium (Fig.9) could bring about significant outperformance.

Fig.9 - Russian equity risk premium

Source: Pictet Asset Management, Sberbank, as at 10th April 2018 (two days post OFAC sanction extension). Cost of equity is the forward earnings yield, and cost of debt is the average yield of RUB and USD bonds and loans.

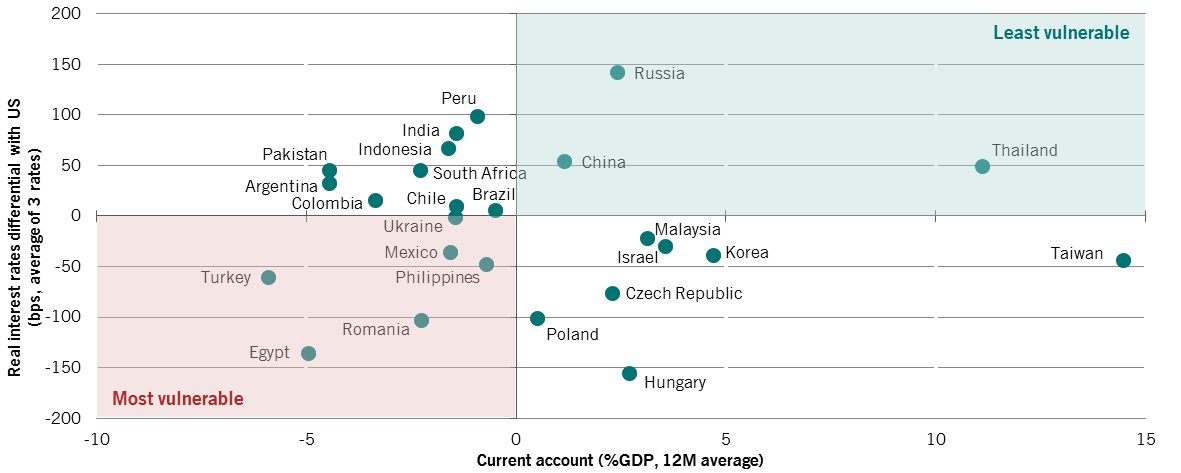

IDENTIFYING EMERGING MARKETS MOST VULNERABLE TO SHOCKS

By Patrick Zweifel, Chief Economist

A simple way to identify the emerging markets most vulnerable to shocks is to look at their external financial needs, via their current account positions (risk proxy) and an average of real interest rates (return proxy). As Fig.10 below shows, emerging markets are extremely diverse, thus still providing a wealth of investment opportunities.

Fig.10 - EM Current account (risk proxy) & real rates (return proxy)

Source: Pictet Asset Management, CEIC, Datastream, Bloomberg, May 2018

Looking at a broader set of 10 risk factors (e.g. excess debt, hard currency debt & FX reserves) shows that Argentina, Turkey, Colombia and South Africa would be other markets at risk. In fact, Argentina was recently forced to hike rates to 40 per cent to defend its currency, a 12.75 per cent rise in just a week.

A point to note is that unlike 2013, the largest emerging markets (BRIIC) seem much less vulnerable this time.

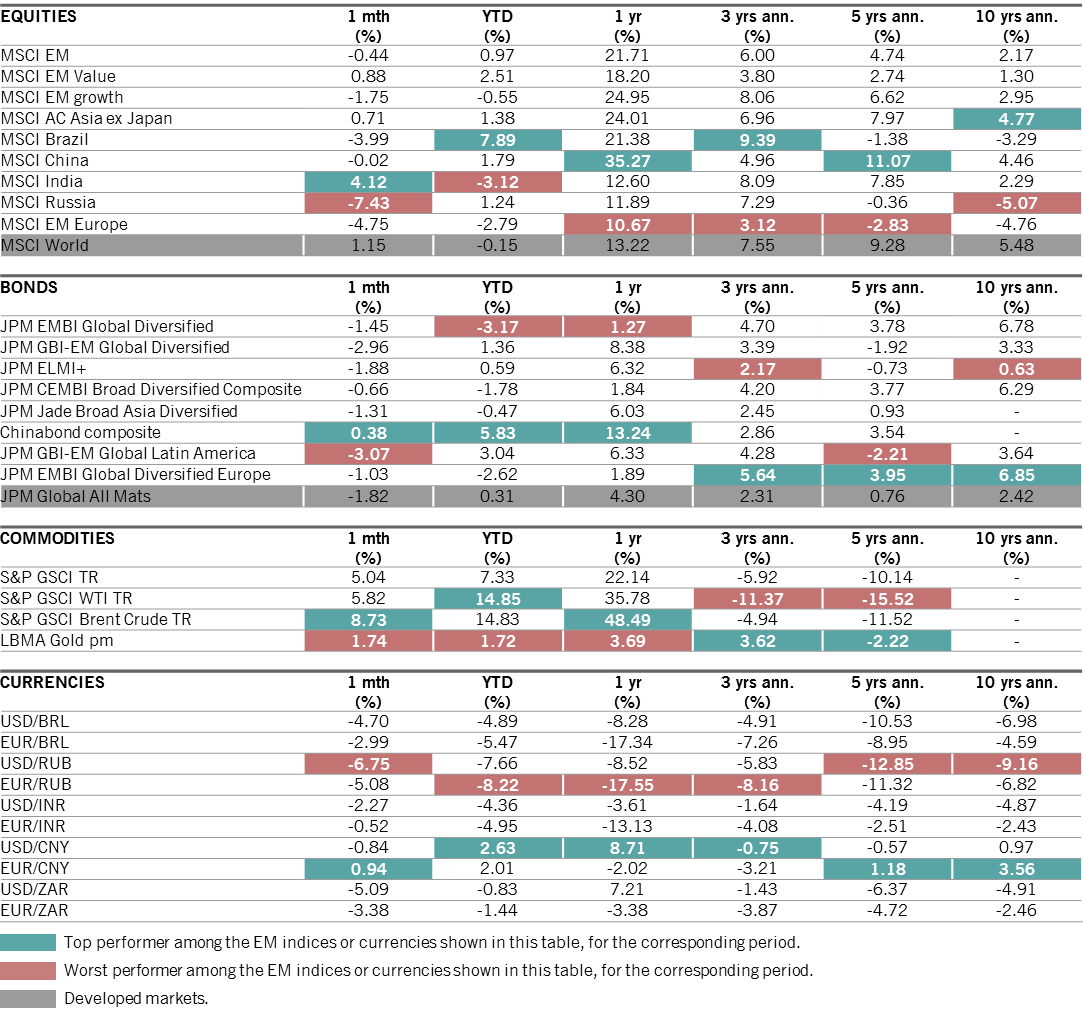

MARKET WATCH

Market watch data

30.04.2018

Source: Datastream, Bloomberg, data as at 30.04.2018 and in USD. Equity indices are quoted on a net dividend reinvested basis; bond and commodity indices are quoted on a total return basis. The currency rates evolution is treated as a performance calculation based on FX rates.

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management. Before assuming his current position in 2009, he was head of the “Macro Research Team” at Pictet Private Wealth Management. In particular, he had economic research responsibility for emerging markets and Japan, and for the development of quantitative models on major asset classes, primarily foreign exchange models. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in econometrics from the University of Lausanne.

About

Nikolay Markov

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Karen Lam

Karen Lam joined Pictet Asset Management in 2013 as a Senior Client Portfolio Manager in the Fixed Income Emerging Corporate team and is based in London.

Prior to joining Pictet Asset Management, Karen was an Executive Director at J.P. Morgan Asset Management working as a global rates portfolio manager and later as a senior client portfolio manager covering fixed income total return strategies and emerging market debt funds. Previously, Karen was the lead manager research analyst at J.P. Morgan Private Bank covering fixed income funds.

Karen holds an MBA from the University of Chicago Booth School of Business and an MSc in Epidemiology from Imperial College London.

About

Hugo Bain

Hugo Bain joined Pictet Asset Management in 2009 as a Senior Investment Manager in the Emerging Markets Equities team. He is a named Portfolio Manager on the Emerging Market strategy and is Co-Lead Portfolio Manager on the Russian Equities strategy, although this is currently suspended.

Before joining Pictet, he spent five years with Fleming Family & Partners Capital Management LLP (FCM) and was a founding partner and co-manager of the FCM European Frontier Fund. He began his career in 1997 at ING, where he remained until 2002 as Head of Russian, Emerging Europe, Africa and Latin America Sales. In 2002 he joined Merrill Lynch as an EMEA Sales Specialist.

Hugo has an MA in Modern History from the University of St Andrews.

About

Christopher Bannon

Christopher Bannon joined Pictet Asset Management in 2007 and is a Senior Investment Manager in the Emerging Markets Equities team, specialising in Emerging Europe and Russia.

Christopher joined Pictet in 2007, initially as a risk manager before moving across to the Emerging Equities Research team in 2011 specialising in the energy sector across global emerging markets. Christopher started his career in 2005 with Citigroup, where he spent 18 months on the corporate actions desk.

Christopher graduated from Trinity College Dublin with a BA (Hons) in Mathematics and Philosophy and he holds an MSc in Finance (graduated with Distinction) from Imperial College London. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.