Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

The Fed: pausing for thought?

The US Federal Reserve claimed its monetary policy tightening campaign would pass off without incident. Nothing could be further from the truth.

Written by

Steve Donzé

Senior Macro Strategist

The US Federal Reserve may come to regret suggesting that rolling back crisis-era monetary stimulus would be like “watching paint dry”.

That’s because the US economy is unlikely to grow quickly enough to justify the degree of tightening it envisages. The Fed could stop hiking interest rates as soon as the first quarter of next year.

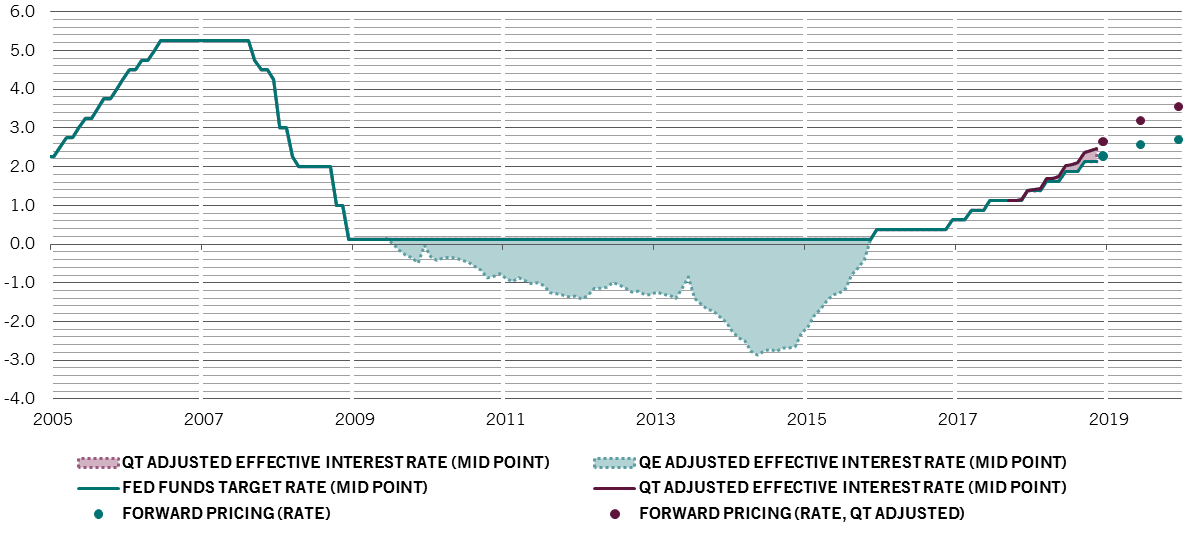

Since October 2017, when the central bank started running down its securities portfolio, its “twin” tightening has seen the cost of borrowing rise by 100 basis points (bps) and its balance sheet shrink by USD350 billion, which we estimate is equivalent to an additional 35 bps of rate hikes.

This has already started to weigh on industries that are traditionally most sensitive to interest rates, including the auto and housing sectors, which together make up a tenth of the US economy.

As the drag from tightening gathers strength, the next shoe to drop may be business investment, which is responsible for 15 per cent of economic output.

The bond market has already discounted the possibility that the Fed will raise rates by an additional 50 bps between now and end-2019 and reduce the size of its balance sheet by a further USD500 billion, which is equivalent to another 50 bps of rate hikes (see chart).

twin tightening bites

US interest rates, %, adjusted for quantitative easing and quantitative tightening

But that, in our view, amounts to an over-tightening that could leave the already cooling US economy in a more fragile state.

According to our calculations, a 100 bps of tightening in financial conditions typically leads to a 1 percentage point reduction in GDP growth in the following year.

Throw into the mix persistent trade tensions and the fading effects of tax cuts and government spending1, and the risk of a soft patch in the economy no longer seems like a distant possibility. It could emerge as soon as the first quarter of 2019.

Rather than risk economic pain, we believe the Fed will adjust the course of its tightening campaign by slowing the pace of interest rates rises. Putting the brake on portfolio asset sales would be more problematic as it would risk the wrath of Congress. Yet that too could become an option if a deeper malaise were to set in – what St Louis Fed President James Bullard describes as possible “cracks” in the economy.

In the event of a Fed rate pause, short-term interest rates would fall faster than longer-term rates, leading to what is known as bull steepening of the yield curve.

And, perhaps more importantly, the US dollar, which is most sensitive to moves in the short-end of the yield curve, would weaken, providing some relief to emerging market economies in particular, where a large number of corporations have accumulated sizeable dollar-denominated debts.

If and when the Fed eases up on the running down of its balance sheet, long-term rates should move downwards in what is known as bull flattening.

As the decade since the 2008 financial crisis has shown, following the intricacies of Fed policymaking is nothing like watching paint dry.

more from multi asset team

America's Road Runner economy

When the US economy does roll over there's little prospect of a fiscal safety net. America Inc is unlikely to come to the rescue either.

June 2018

Trumpism restrained not vanquished

The US mid-term elections delivered a partial victory to the Democrat opposition in a development that could reshape parts of President Trump's economic agenda.

November 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.