Proxy voting

Leveraging our power as investors to achieve positive change, we systematically exercise our voting rights in the best interests of our clients.

Exercising voting rights and responsibilities

The overarching purpose of our voting is to protect and promote the rights and long-term interests of our clients as shareholders. As such, we consider it our responsibility to hold companies and their executives accountable for their decisions. We aim to support a strong culture of corporate governance, effective management of environmental and social issues and comprehensive reporting according to credible standards.

Voting scope

Equity

For our equity funds, the following principles define the scope of accounts and securities eligible for proxy voting:

1. For actively managed funds, we aim to vote on 100 per cent of equity holdings.

2. For passive strategies, we aim to vote on companies representing 80 per cent by weight of underlying benchmarks. This target may be revised upwards or downwards for specific strategies depending on factors such as portfolio size, geography or market capitalisation.

3. For segregated accounts, including mandates and third-party (i.e. sub-advisory) mutual funds managed by Pictet Asset Management, clients delegating the exercise of voting rights to us have the choice between our policy or their own voting policy.

Multi asset

For our multi asset funds, voting takes place on the underlying equity funds managed by Pictet Asset Management. We also aim to vote where we have direct holdings in companies.

Voting guidelines

Our proxy voting guidelines, included within our Responsible Investment Policy, apply to all our investment strategies (we have not set any strategy-specific voting policies or guidelines) and are based on generally accepted standards of best practice in corporate governance. These include board and management, executive remuneration, risk control and reporting, and shareholder rights. The standards give a benchmark for assessing companies and exercising our active ownership duties throughout the life cycle of an investment, from pre-investment phase to engagement, proxy voting, up to the point of exit.

As active managers, we place significant importance on how we vote. The long-term interests of shareholders are our paramount objective. On occasion, we may vote against management if we believe that doing so is in the best interests of shareholders and our clients. Where we do this, we classify the vote as significant, in line with the EU Shareholder Rights Directive II, and we publicly disclose our rationale as part of our quarterly vote reporting. We also reserve the right to deviate from our voting policy to take into account company-specific circumstances.

We believe that governance, both for companies and countries, will come back to the fore and play a much more important role in investors’ agendas as the extended era of cheap money comes to an end.

Voting activity

The following charts provide an overview of Pictet Asset Management’s 2022 voting activity. These are aggregated data compiled during the year.

1. 2022 aggregated votes

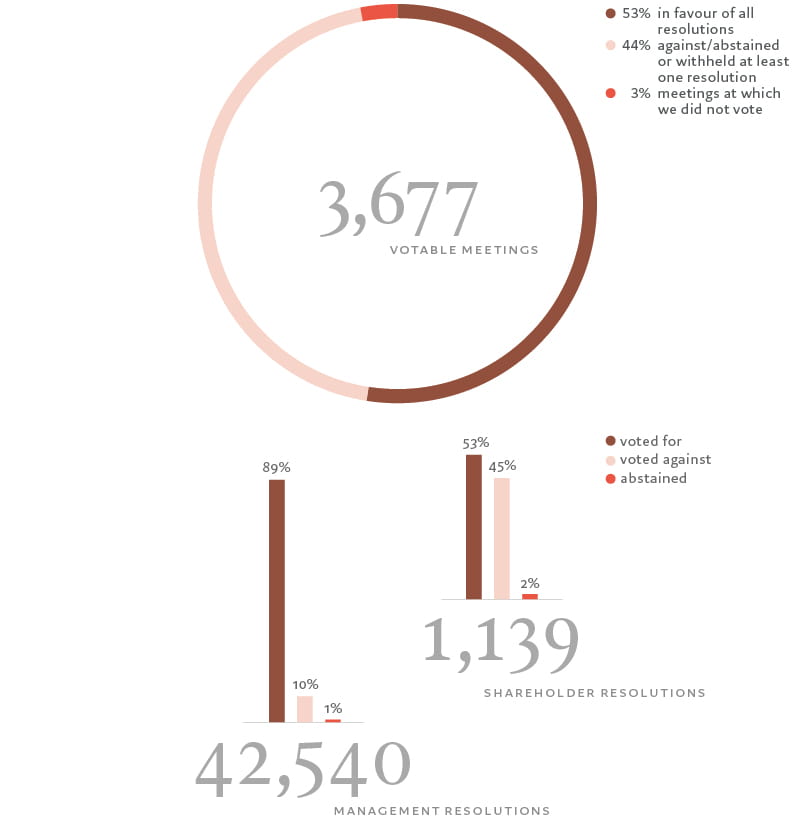

Meeting overview

In 2022, Pictet Asset Management voted at 3’576 general assembly meetings out of 3’677 votable meetings for active and passive equities. We voted "against" (including "abstained" or "withhold") to at least one resolution at 1’641 meetings and we did not vote at 101 meetings.

Fig. 1 - 2022 voting activity

Management resolutions

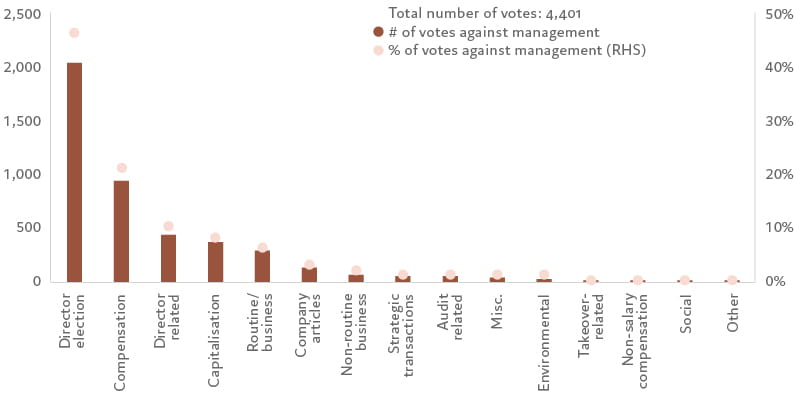

Out of 42’540 management resolutions we voted against management on 4'401 items (10%), supported management on 37'718 items (89%) and voted "abstain" on 421 items (1%).

We voted against management on resolutions that relate primarily to director election (46%), compensation (21%) and director related (10%)

Fig. 2 - Breakdown of management resolutions not supported

Shareholder resolutions

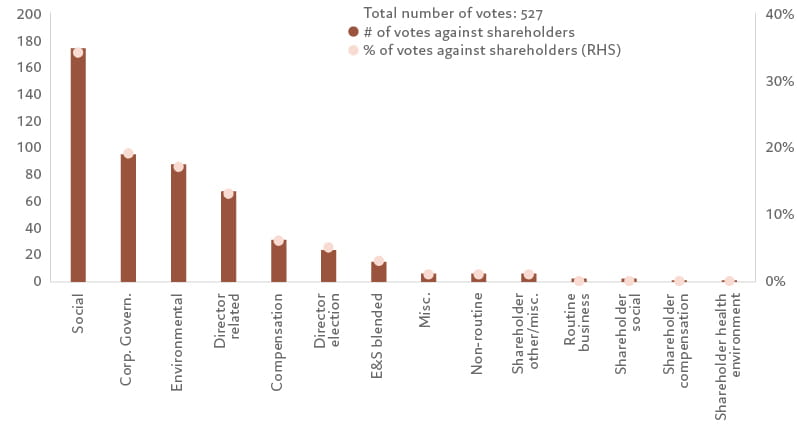

We voted against 527 shareholder resolutions out of 1’139 proposals (45%).

The main categories of shareholder resolutions that we didn't support relates to social (34%), corporate governance (19%) and environmental (17%) issues.

Fig. 3 - Breakdown of shareholder resolutions not supported

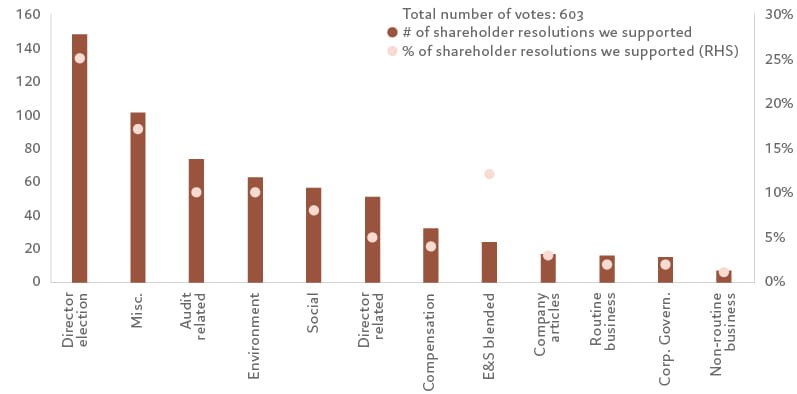

We supported 603 shareholder resolutions out of 1’139 proposals (53%).

The main categories of shareholder resolutions that we supported are director election (25%), audit related (12%) and environment (10%).

Fig. 4 - Breakdown of shareholder resolutions supported

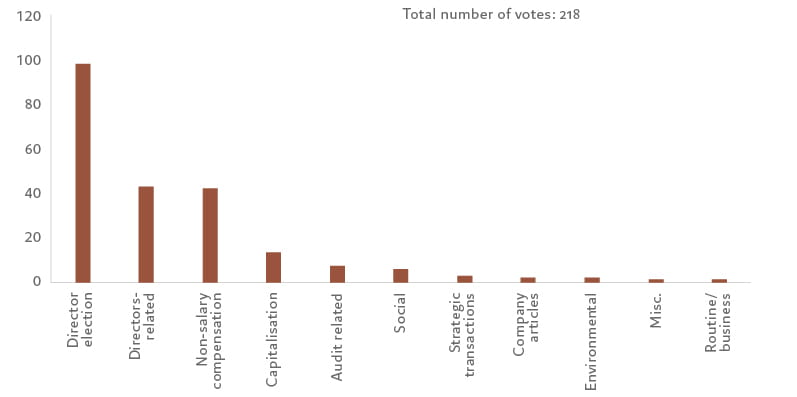

Deviations from voting guidelines

In 2022 we deviated from third-party recommendations on 218 resolutions. The main categories we deviated were related to director election (98 resolutions), directors-related (43 resolutions) and non-salary compensation including shareholder approvals of compensation related matters (42 resolutions).

Fig. 5 - Breakdown of deviations from Pictet Asset Management's voting policy

2. Voting records

Both our annual and monthly voting records can be viewed here:

| |

Summary 2020 | |

Summary 2021 | Summary 2022 | |||

| Summary 2023 | January 2024 | February 2024 | |||||

| March 2024 |

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.