Asset allocation: stocks set for another slide

The escalation of trade tensions between the US and China has intensified concerns about the strength of the global economy and corporate earnings.

If prospects for global equity markets looked unfavourable before US President Donald Trump’s latest salvo in the trade battle, then they are even more discouraging now. We therefore retain our defensive asset allocation stance: underweight on stocks, neutral on bonds and overweight cash.

June 2019

In recent weeks, the US raised tariffs on USD200 billion of Chinese goods to 25 per cent from 10 per cent, prompting Beijing to retaliate with a similar move. Washington is now mulling higher duties for another USD300 billion of goods.

Our analysis shows that, if implemented, the cumulative impact of these tariff increases will cut some 0.2-0.3 percentage points from world GDP growth this year. That’s a sizeable amount which doesn’t even take into account any secondary effects that might ripple through the global value chain.

What is particularly concerning is that this hit comes at a time when the global economy is already stuttering. Our business cycle indicators show economic conditions deteriorated in many parts of the world last month, including China, which suffered an abrupt slowdown in April. The economic boost from Beijing’s stimulus measures appears to have faded in recent weeks and renewed trade tensions do not bode well for the coming months.

That said, emerging markets generally remain on a much stronger economic footing than their developed peers. And China still has plenty of stimulus at its disposal, both fiscal and monetary.

Indeed, China is one of the few countries where our liquidity indicators are positive. The flow of credit across the economy is improving and there are some signs that small and medium-sized companies are finding it easier to access bank lending. In the developed world, however, liquidity conditions aren't especially encouraging for riskier assets as central banks continue to shrink their balance sheets. From this perspective, emerging market (EM) assets look more attractive relative to their developed counterparts.

Our valuation models paint the same picture. EM currencies remain deeply undervalued – by as much as 20 per cent relative to the dollar – while EM local currency debt is easily the cheapest of all fixed income asset classes.

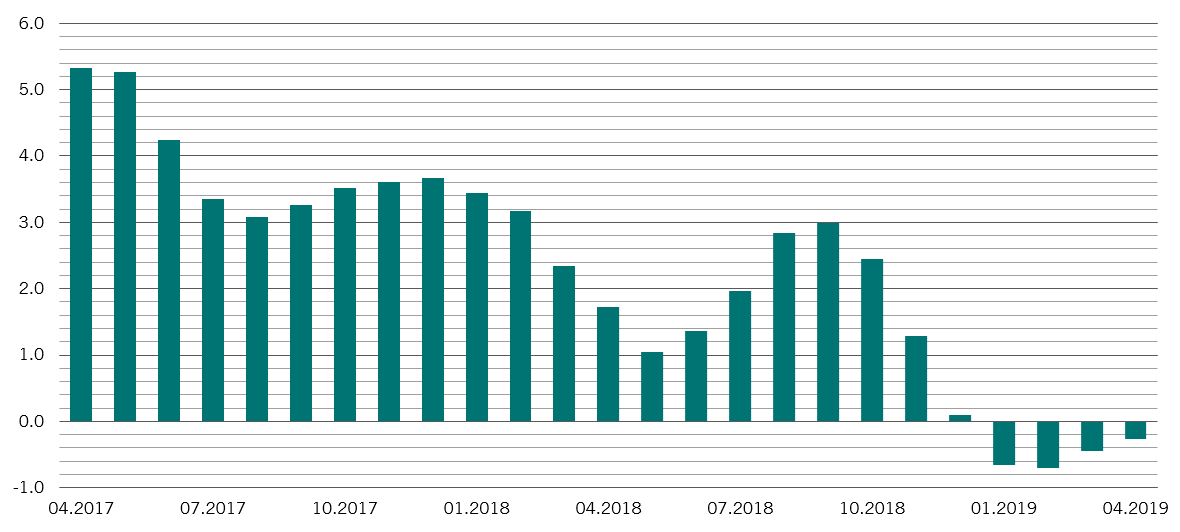

More broadly, world stocks are fairly valued according to our model, trading at a price-to-earnings ratio of around 15 times and a dividend yield of 2.9 per cent. Still, earnings prospects are uninspiring. Corporate profit growth can be expected to slow further in the coming months, with our model pointing to 3 per cent increase in profits this year versus the consensus view of 7 per cent. Corporate profit margins also remain under pressure.

The technical indicators we monitor, meanwhile, show that seasonality has turned deeply negative for equities across the board, ahead of what is traditionally a volatile summer period.