Asset allocation: a delicate equilibrium

The world has found a delicate state of equilibrium. On the down side, economic growth is faltering, and valuations for virtually all asset classes have become more expensive since the start of the year. And then there are also the unresolved matters of Brexit and the US-China trade dispute.

On the up side, however, liquidity conditions have improved and China is starting to reap the benefits of monetary and fiscal stimulus.

Although it is difficult to be enthusiastic about developed market assets in general – we remain neutral global bonds and stocks – defensive equities, where earnings are holding up well, and emerging markets (EM), which are growing faster than their rich world counterparts, both look promising.

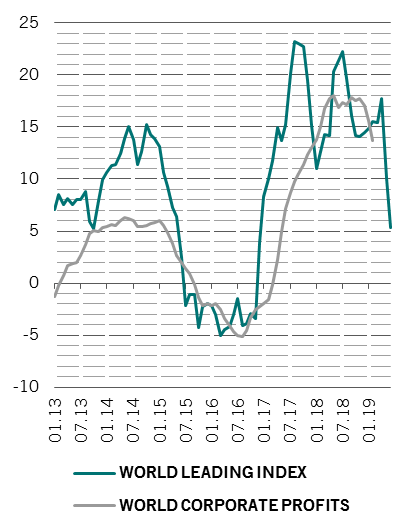

Our business cycle indicators show emerging economies are outpacing their developed counterparts. Historically, this has been supportive for all EM asset classes, and particularly for currencies.

Based on our leading indicators, the growth gap between the emerging and developed world – at nearly 5 percentage points – is at its highest in half a decade. The disparity reflects a steep drop in export orders among developed economies such as Germany, which appear to be suffering disproportionately from ongoing trade tensions. EMs – and particularly China – have also been hit to an extent. Indeed, our models show that the tariffs unveiled by the US to-date should shave around 0.5 percentage points off Chinese GDP growth. But Beijing authorities have acted fast to counterbalance this with stimulus. We estimate their measures so far – which include infrastructure projects as well as income and corporate tax cuts – will have a positive impact of 1 percentage point on growth, spread over last year and this.

The risk is that investors are too complacent. While central banks have proved responsive to signs of economic weakness, we believe this could prove a temporary shift in tone. In our view, the market’s interest rate projections underestimate the likelihood of US Federal Reserve hiking interest rates once more before the year end. Fed futures are pricing in only a 2 per cent chance of such a move; in October it was 98 per cent.

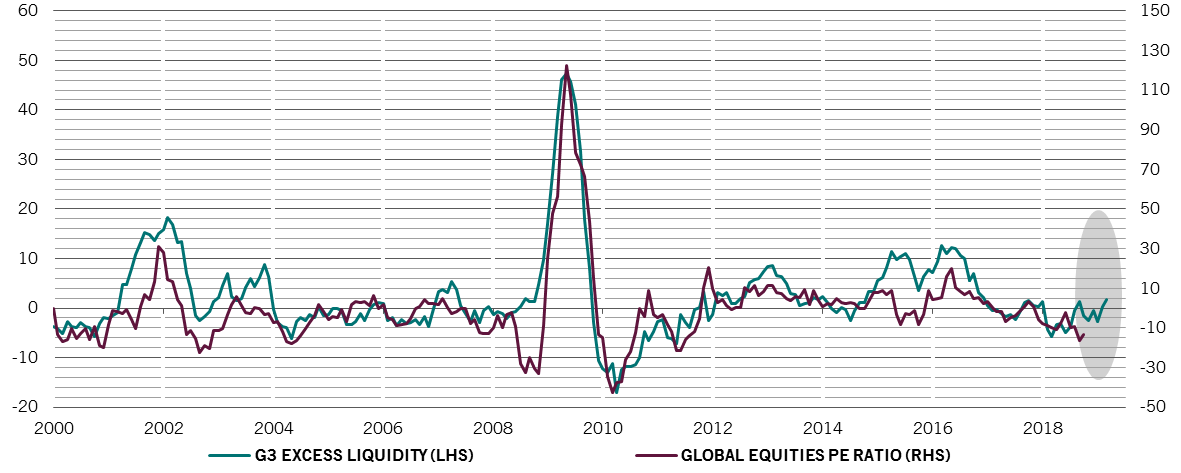

Valuations add a note of caution following strong market gains in early 2019. Virtually every asset class in our model is more expensive now than a month ago, with global equities among the priciest. This is worrying given that corporate earnings growth peaked in 2018, at 15 per cent, and that analysts have been reducing their expectations for future profits. However, we see early signs of stabilisation in earnings forecasts, which should prove positive.

Technicals paint a mixed picture. Although trends are generally positive for equities, in many regions – including the US and Europe – this is offset by some excessively bullish investor positioning in certain stocks. For bonds, meanwhile, upbeat momentum and breadth – the degree to which the recent rally has been broad-based – are counterbalanced by strongly negative seasonal trends. Taken together, these signals back our decision to remain neutral on both equities and bonds at a global level.