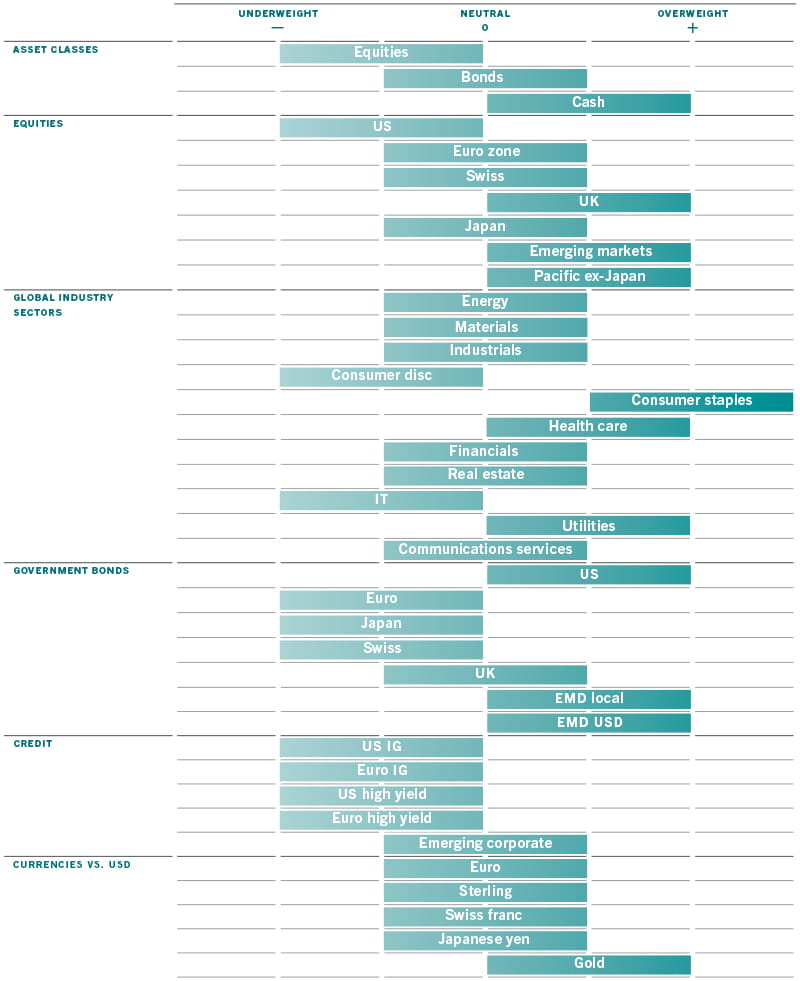

Asset allocation: downside risks persist

Equities had a banner month, thanks in part to continued progress in US-China trade talks and tentative signs of stabilisation in industrial production worldwide.

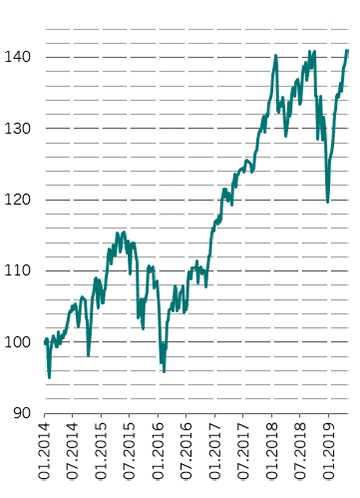

But the market’s stellar gains – global stocks are up more than 10 per cent so far this year – mask the fact that the world economy is not out of the woods yet.

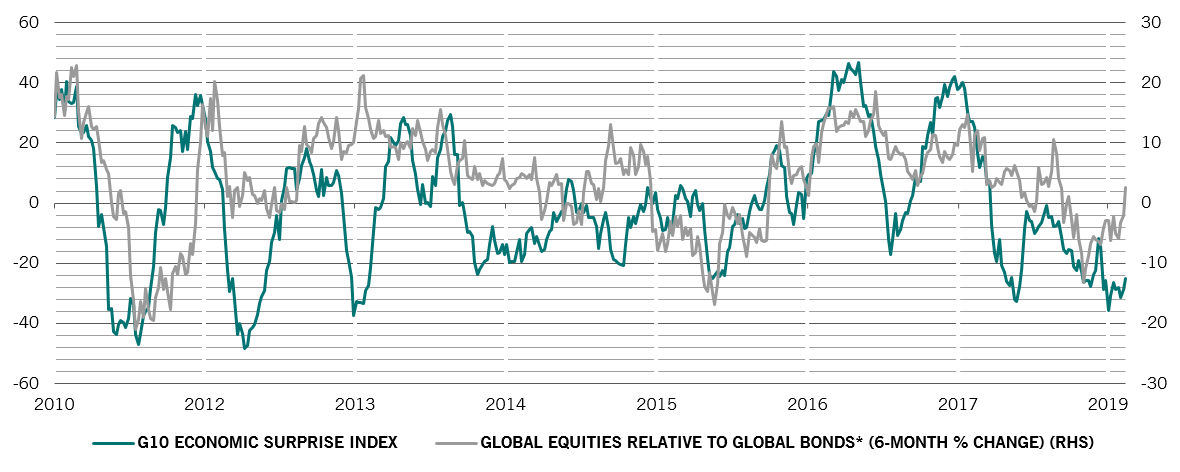

Globally, economic data has been below consensus expectations for 14 months in a row, the longest stretch since the financial crisis.

World trade, on volume terms, is now at its weakest level since 2009 while business confidence in developed economies is falling. At the same time, investors appear too optimistic about prospects for corporate earnings growth.

In this climate, equities may struggle to add to their recent rally. We therefore maintain our underweight stance on stocks. We remain neutral on bonds.

Our business cycle indicators persistently show risks to world economic growth. Our leading indicators suggest global GDP growth will slow to 2.4 per cent annualised by early July from 2.9 per cent at end-2018 – with developed economies responsible for most of that slowdown.

Emerging countries continue to enjoy brighter economic prospects; we expect their growth rates to improve to a yearly 4.4 per cent in 2019 from 4.2 per cent from last year.

The developing world’s outperformance owes a lot to China, where recent fiscal and monetary stimulus has helped stabilise the world’s second largest economy. China’s industrial production has rebounded to the strongest level since 2014, while infrastructure spending and car sales have stopped their precipitous decline. Russia’s economy, meanwhile, should benefit from the recent rise in oil prices.

Our liquidity indicators support our cautious stance on riskier asset classes. Financial conditions may have become less restrictive, but they are not loose.

The US Federal Reserve is still expected to withdraw some USD200 billion of liquidity from the market by September as it reduces the size of its balance sheet while China is no longer going full throttle on monetary stimulus.

We think markets have already priced in the prospect of additional monetary support in the coming months – attaching a 50 per cent probability to a US rate cut this year.

Our valuation scores show equities are not especially expensive. Global stocks trade at a price to earnings ratio of 17 and a price to book ratio of 2 – both are around the average of the past 35 years.

We are still concerned about the potential for corporate earnings to fall sharply after their 15 per cent rise last year. Our models suggest profits are likely to grow by just 1 per cent this year, compared with a consensus forecast for nearly 7 per cent.

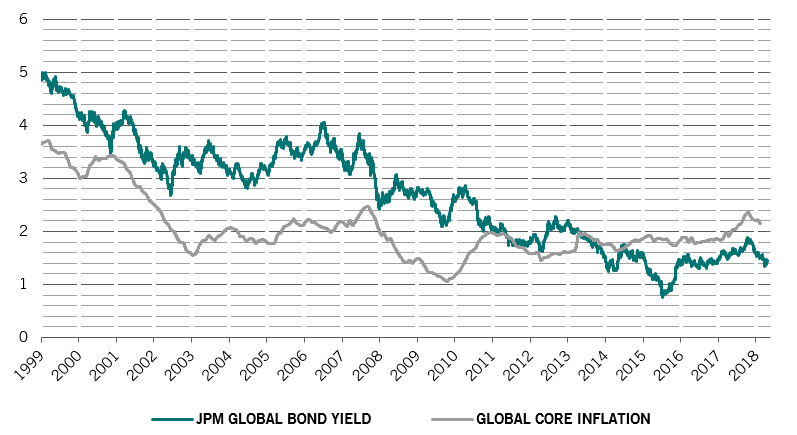

In the fixed income market, European and Japanese government bonds remain expensive.

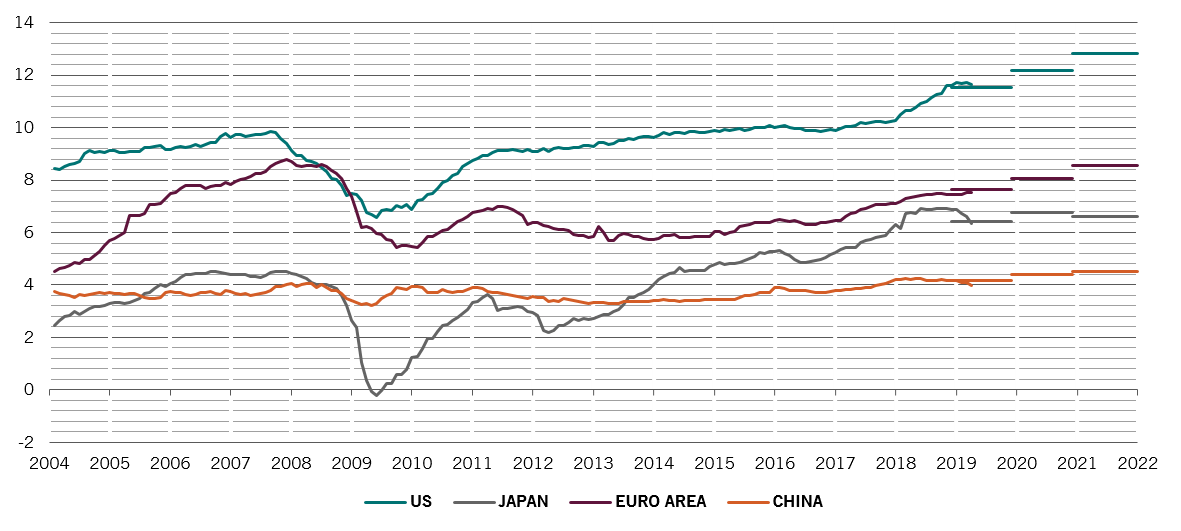

G10 economic data has been below expectations

Technical signals are generally supportive for equities and bonds.

They also highlight that implied volatility for equity markets has fallen sharply of late, while the MOVE volatility index for bonds is also back towards record lows.

Given this, it has become cost effective to deploy call options to hedge against the possibility of a sentiment-driven “melt-up” rally in equities – like the one seen in 1999. Such a risk is especially high as portfolio flows data shows institutional investors have yet to fully participate in the recent rally.