EM Monitor: Central Eastern European economic growth

July 2019

Marketing Material

Central European economies: decoupled from the Eurozone

Central European countries are defying Eurozone weakness with strong rates of growth. What is the reason and how can investors benefit?

Written by

Nikolay Markov

Senior Economist

Share this article

Central and Eastern European economies have managed to generate surprisingly robust growth rates and seem to have decoupled from the Eurozone slowdown. Their resilience can be attributed to buoyant domestic demand, led by consumer credit. How long can the boom last and how can investors benefit?

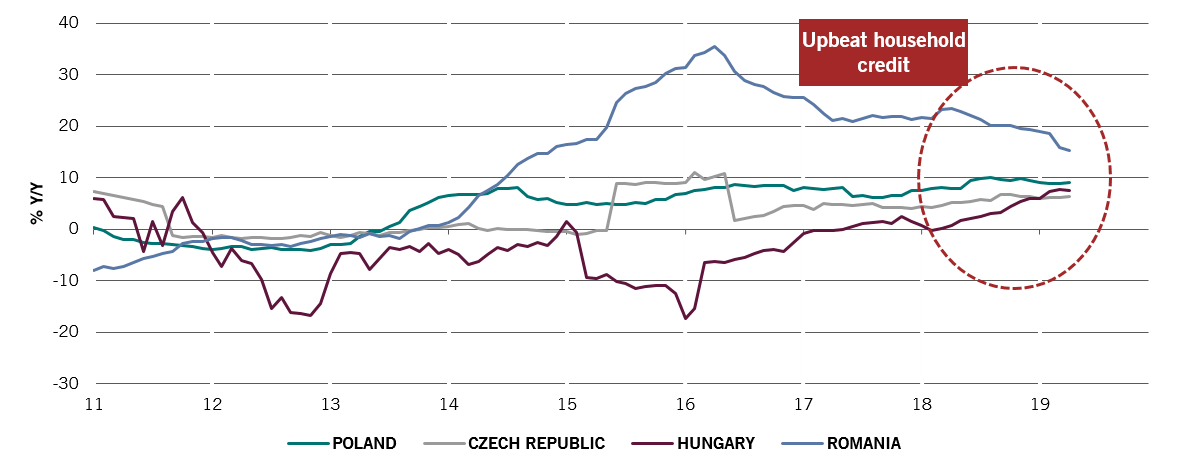

Rising Consumer credit in CEE4 countries

Fig.1 - CEE4 household consumer credit growth

Source: Pictet Asset Management, CEIC, Refinitiv, data to April 2019

There are three aspects to consider.

1. Tight labour market conditions

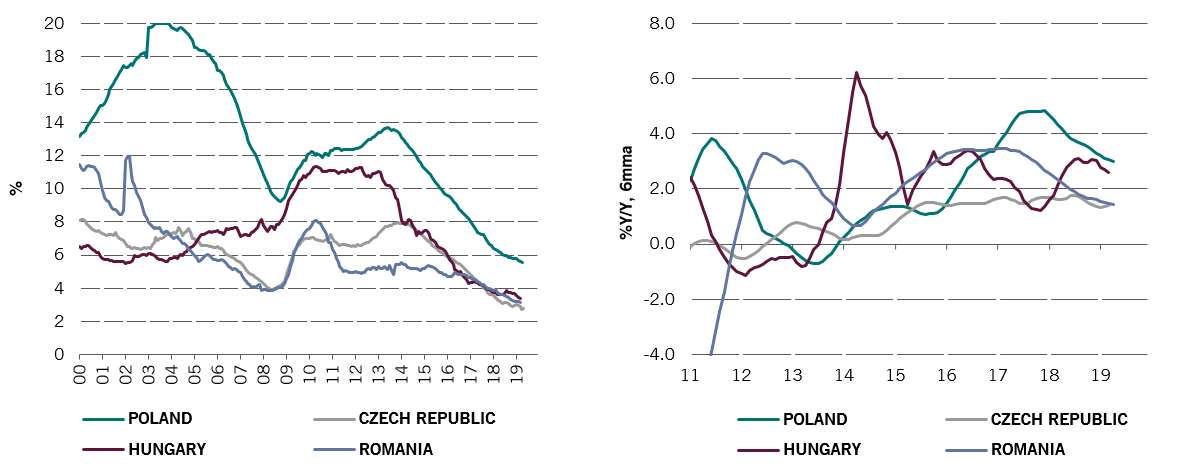

Very tight labour market conditions resulting from record low unemployment rates and strong employment growth are boosting consumer spending (see Fig.2 and Fig.3 below).

Falling unemployment and rising employment lead to tight labour market conditions

Source: Pictet Asset Management, CEIC, Refinitiv. Left: Hungary and Romania data to March 2019; Poland data to April 2019; Czech Rep. data to May 2019. Right: Czech Rep. and Hungary data to March 2019; Poland and Romania data to April 2019.

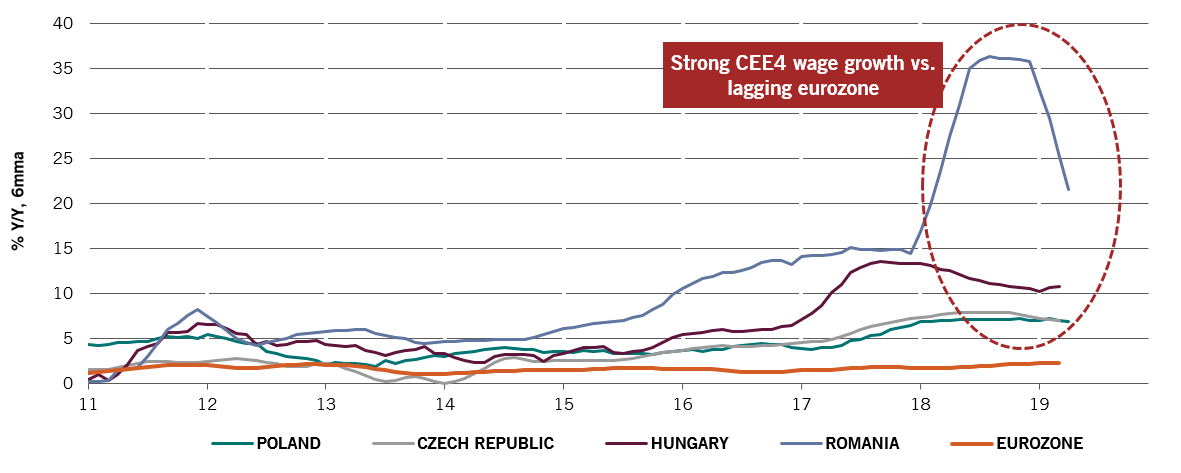

This has transmitted into strong nominal wage growth in all CEE4 countries: from 7.1 per cent for the Czech Republic, to 21.6 per cent in Romania – in strong contrast to the Eurozone’s 2.4 per cent.

Unlike in the Eurozone, Wages in CEE4 countries have been on the rise

Fig.4 - Nominal wages, % Y/Y, 6mma

Source: Pictet Asset Management, CEIC, Refinitiv. Data to March 2019 for the Czech Rep., Hungary and the Eurozone. Data to April 2019 for Poland and Romania.

2. From wage to consumer price inflation

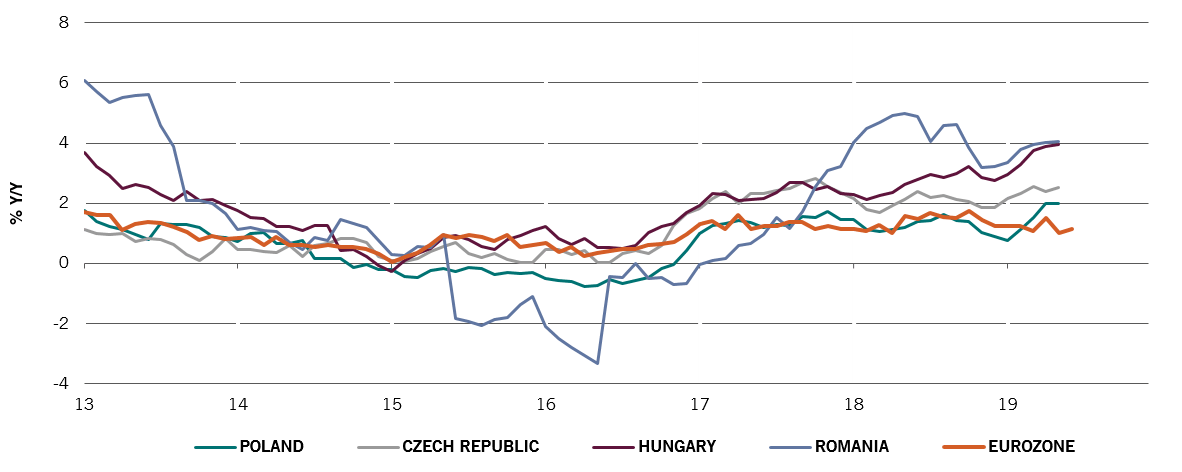

The second part of the transmission channel, from wage to consumer price inflation, has also materialised in the CEE4, unlike in the Eurozone. Both headline and core inflation rates have picked up (see below).

Strengthening wages feeding through to inflation

Fig.5 - Average of headline & core CPI, % Y/Y

Source: Pictet Asset Management, CEIC, Refinitiv. Data to May 2019 except for the Eurozone which is as at June 2019.

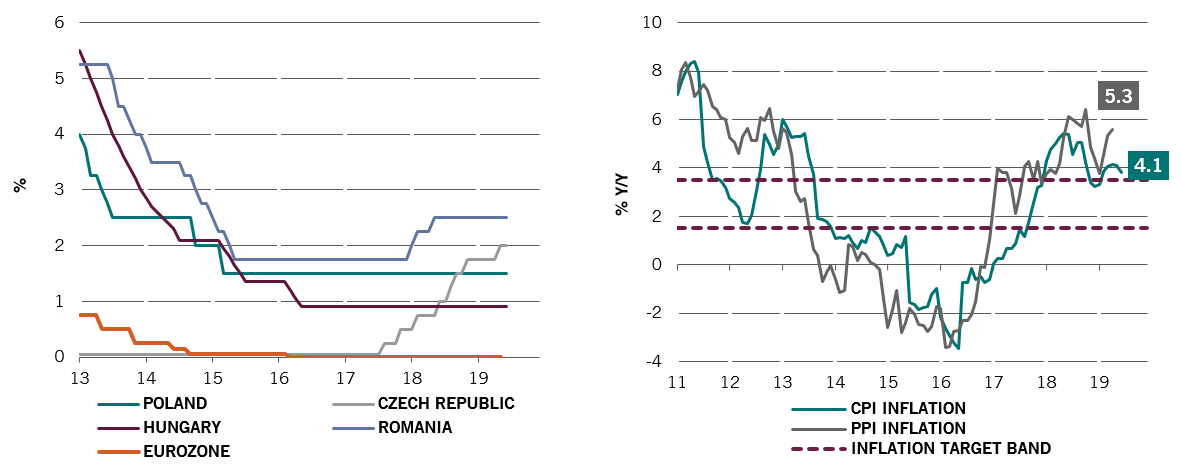

3. Central banks

With inflation pressures creeping up, central banks would be expected to ramp up measures to contain inflation. However, this has been the missing piece of the puzzle so far, except in the Czech Republic and, to a limited extent, in Romania.

Central banks slow to respond to inflationary pressures

Fig.6 (left) - Central banks key policy rates / Fig.7 (right) - Romania CPI & PPI inflation

Source: Pictet Asset Management, CEIC, Refinitiv. Left: all data as at June 2019 except for the Eurozone which is as at May 2019.

Right: PPI inflation as at April 2019, CPI inflation as at June 2019.

The most worrying example is Romania, where inflation has surged above the targeting range (see fig.7 above on the right), after the central bank started normalising monetary policy last year but then paused the tightening stance.

Investors in the CEE4 economies will need to watch out for a normalisation of monetary policy soon. This is justified by the upbeat domestic conditions which are feeding into higher core inflation. The Eurozone would have wished to be in this case, but finds itself at the other end of the spectrum. Nevertheless, investors also need to watch out for some economies at risk due to rising current account deficits, deteriorating public finances and increasing public debt. This is particularly the case in Romania and Hungary.

Conclusion

CEE4 countries’ wage-driven growth has made them largely immune to the slowdown in the Eurozone. We believe this provides investment opportunities, especially in the equity space (see next section).

THE VIEW FROM OUR EMERGING EUROPE EQUITY TEAM

By Christopher Bannon, Senior Investment Manager, Pictet Emerging Europe

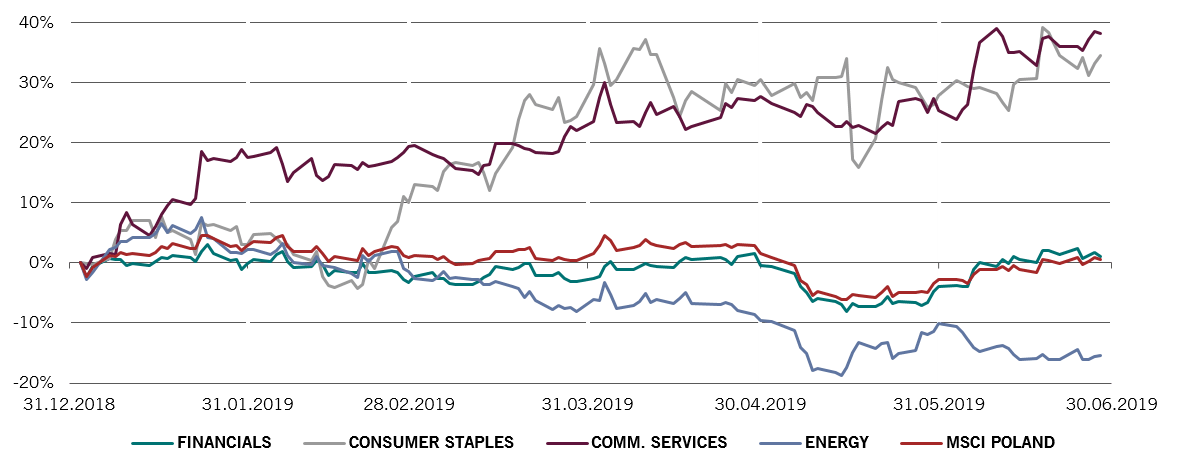

Whilst a rising tide lifts all boats, a booming economy does not always lift all stocks – and this is very much the case across CEE4 economies. Taking Poland for instance, the year-to-date underperformance of index heavy-weight sectors, i.e. financials and energy, has been striking versus the very strong outperformance of the mid-cap space of consumer staples and communication services.

Consumer-driven sectors leading the way up

Fig.1 - MSCI Poland indices

Source: Pictet Asset Management, Bloomberg L.P., as at 30.06.2019

Consumer-led growth has come at the expense of banks and energy firms – the fiscal funding source of expansionary policy.

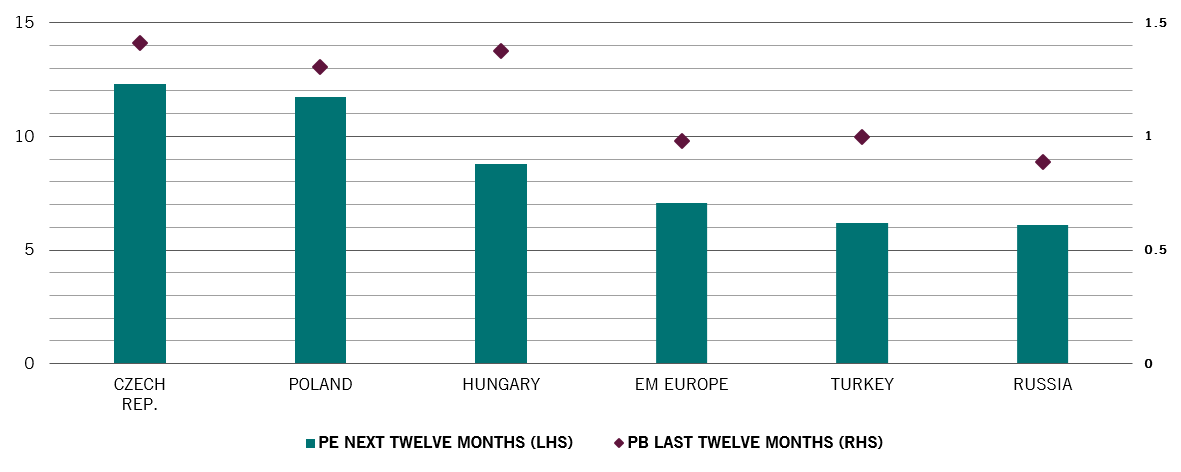

Moreover, CEE4 markets are expensive relative to benchmark peers* Russia and Turkey (see chart below).

CEE4 markets are expensive compared with benchmark peers*

Fig.2 - CEE4 valuations

Source: Pictet Asset Management, Factset, as at 30.06.2019

As a result – we view CEE4 economies as stock picking markets where we invest selectively and with high conviction. Today, we hold positions predominantly in Polish companies exposed to consumer spending, eschewing financials and banks.

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Christopher Bannon

Christopher Bannon joined Pictet Asset Management in 2007 and is a Senior Investment Manager in the Emerging Markets Equities team, specialising in Emerging Europe and Russia.

Christopher joined Pictet in 2007, initially as a risk manager before moving across to the Emerging Equities Research team in 2011 specialising in the energy sector across global emerging markets. Christopher started his career in 2005 with Citigroup, where he spent 18 months on the corporate actions desk.

Christopher graduated from Trinity College Dublin with a BA (Hons) in Mathematics and Philosophy and he holds an MSc in Finance (graduated with Distinction) from Imperial College London. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.