GDP growth should be stronger across many emerging markets in 2020 as Anjeza Kadilli explains.

Written by

Anjeza Kadilli

Senior Economist

Share this article

A stronger year ahead for emerging markets

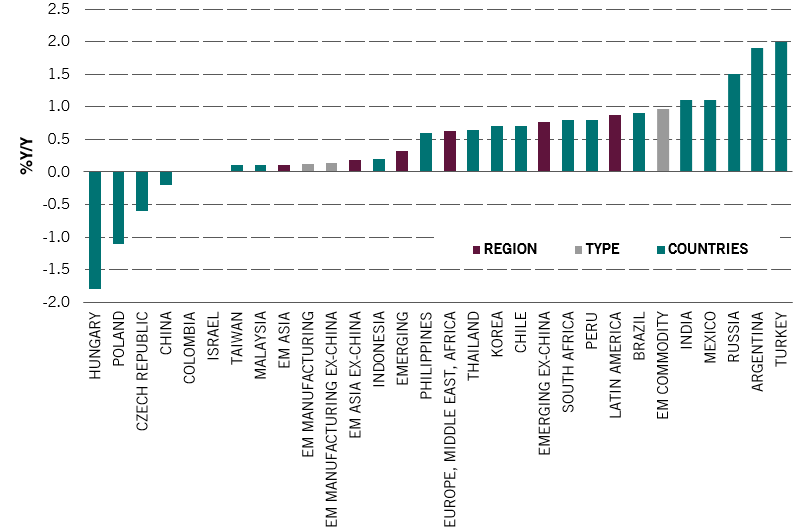

After a lacklustre performance in 2019, we expect 2020 to mark a shift in GDP growth momentum for the majority of emerging markets. In particular, we think Turkey will see the biggest growth rebound after a difficult 18 months. Next is Argentina, where we still forecast negative GDP growth, but at a much smaller magnitude than in 2019.

Clearly, both of these markets remain in stressed economic conditions, but overall, across all other emerging markets it is a more positive picture, underpinning our bullish house view.

Bouncing back...

Fig.1 - Real GDP growth change: 2020 forecast less 2019 forecast (%Y/Y)

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019.

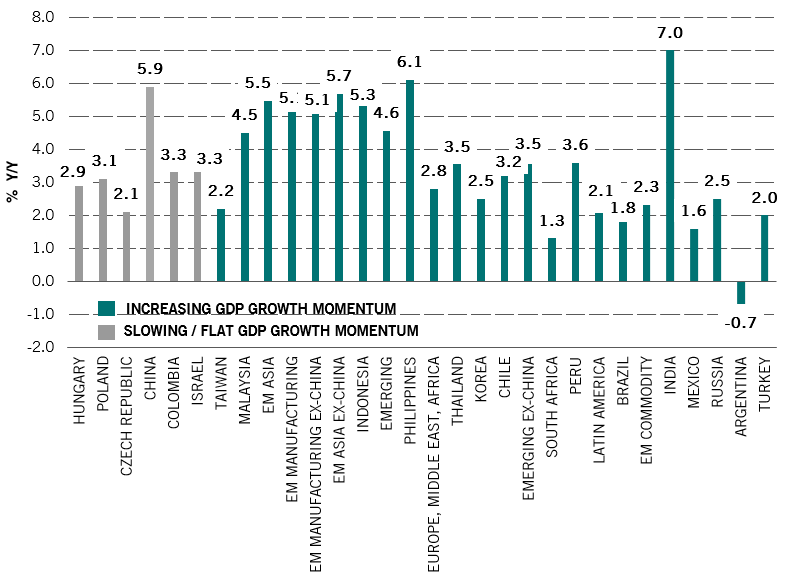

Indeed, as the chart below shows we expect all emerging markets, except for Argentina, to deliver positive real GDP growth in 2020.

Growth in positive territory

Fig.2 - Real GDP growth 2020 forecasts

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; September 2019.

Asia to remain the growth engine of emerging markets

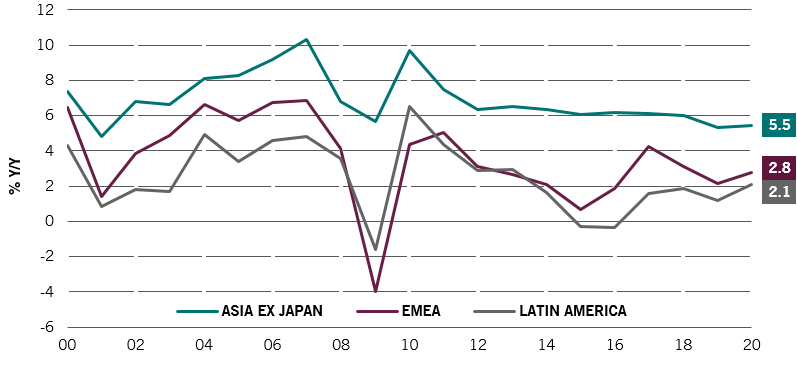

Drilling into regional clusters, we believe Asia ex-Japan will remain the growth engine of EM, despite slowing growth in China. Latin America and EMEA however are picking up but are still forecast to deliver GDP growth only half as significant as Asia.

Asia: the EM locomotive

Fig.3 - Real GDP growth: Asia ex Japan, EMEA, Latin America

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019.

Inflation under control

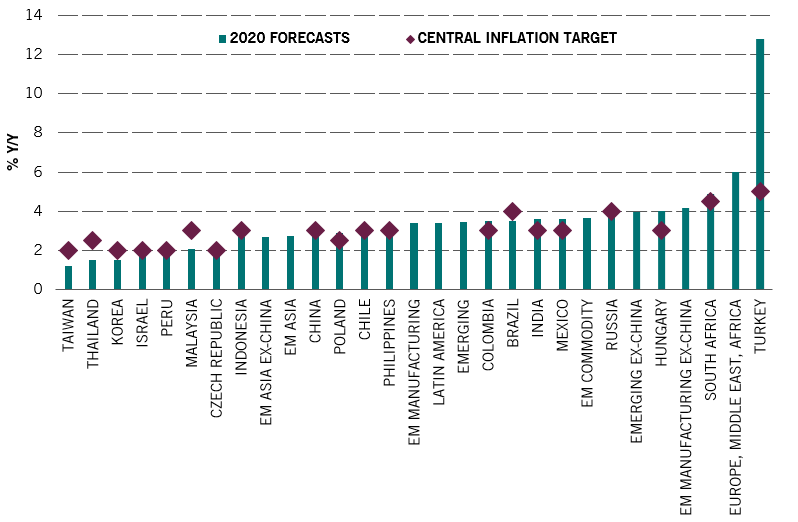

Another positive tailwind for EMs in 2020 is a relatively benign inflation outlook, except for outliers such as Argentina and Turkey (in the former inflation should be around 50% in the year ahead).

The genie appears to be back in the bottle...

Fig.4 - 2020 CPI inflation forecasts

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019.

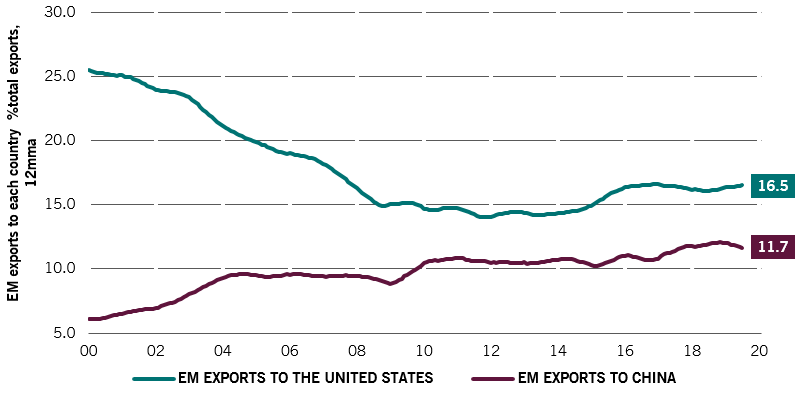

Final thoughts: will EM exports shift to China?

An interesting chart to watch will be the one below, which tracks the share of EM exports to the world’s two biggest economies: the US and China. With the trade tensions between the two ongoing will we see a crossover or narrowing of the gap in 2020? Our view is there will be a narrowing as China becomes an increasingly dominant source of exports for emerging markets.

China vs US

Fig.5 EM exports to China and to the US as share of GDP

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019.

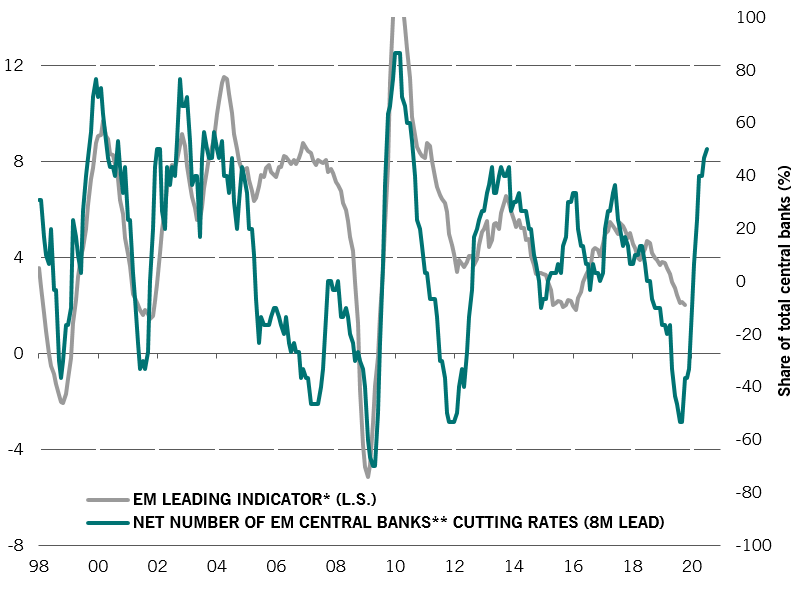

Chances of a 'melt-up recovery' - the view from our EM Equity team

By Kiran Nandra, Senior Product Specialist

After the volatility of 2019, we expect 2020 to be the year of ‘melt-up recovery’ linked to both an easing of trade tensions as well as very supportive policy easing measures across emerging markets (see chart below).

EM leading indicator and central bank actions

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019. *GDP weighted. **30 central banks

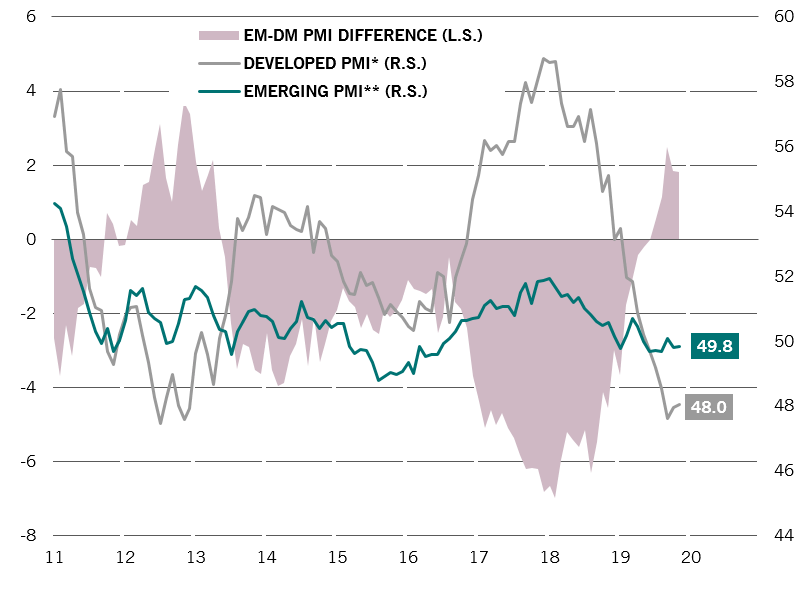

This is in addition to an already wide discrepancy between emerging and developed market business manufacturing surveys where the gap is currently the highest since 2013 in favour of EM – see below.

Emerging and developed manufacturing surveys

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019. *10 manufacturing PMIs GDP weighted. **22 manufacturing PMIs GDP weighted.

So where does this leave us?

Overall, among emerging markets we view the Asia ex-Japan region as highly attractive, particularly in specific niches of the market. For example, as bottom-up investors, we have been reducing our South Korea underweight for various reasons:

1. We are seeing a more benign domestic environment especially for an economy as exposed to global trade as South Korea

2. Corporate governance is showing nascent signs of improvement

3. A stronger outlook for the tech sector, in particular the memory chip industry.

Anjeza Kadilli joined Pictet in 2015. She is an Senior Economist in Pictet Asset Management’s Economic Analysis team where she conducts macroeconomic analysis of emerging markets. Anjeza holds a PhD in Econometrics from the University of Geneva - where she also obtained an MSc and BSc in Economics. During her PhD, Anjeza spent time at the University of Southern California, Riksbank and HEC Montreal as a visiting scholar.

About

Kiran Nandra

Kiran Nandra joined Pictet Asset Management in 2016. She is the Head of EM Equities Management and Senior Client Portfolio Manager for the Emerging Equities team.

Previously, Kiran worked at Wellington Management where she was most recently a Portfolio Specialist.

She joined Wellington in 2003 in a Relationship Management role before becoming a Research Analyst covering European and Latin American banks.

Kiran graduated from University College London with an LLB (Honours) degree in Law and has an MBA from The University of Chicago Booth School of Business.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.