Overview

It was Milton Friedman who said “only a crisis produces real change.” How ironic, then, that the Nobel Laureate’s observation now appears to apply to the euro zone – a project he famously described as economic and political folly.

For faced with a public health crisis and the deepest recession since World War Two, European leaders have fashioned a rescue plan that could, with luck, prove transformative for the region.

Conceived by Germany and France, the new EU recovery fund is revolutionary in several respects. First, it is large. Combined with measures such as the Guarantee Fund for EU businesses and the European Stability Mechanism (ESM), the EUR750 billion package takes Europe’s collective spending power to about EU1.2 trillion, or 6.5 per cent of its GDP. In every sense, it is a potent response to the pandemic shock.

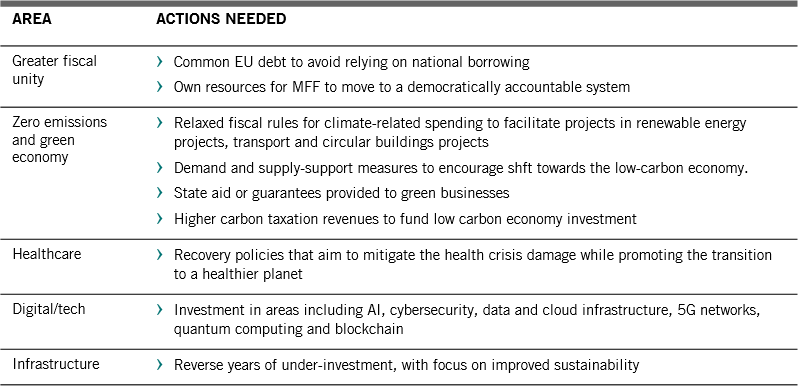

Second, it is ambitiously green. Up to a third of the planned investment is to be channelled to projects that will hasten the bloc’s transition to a net zero carbon economy.

There is every chance Europe could emerge from the pandemic with firmer political and economic foundations in place.

Third, and most importantly, the scheme embodies collective responsibility.

Specifically, it is predicated on closer fiscal co-ordination and the creation of a euro zone sovereign bond market worthy of the name.

In fact, how the fund is financed is arguably just as important for Europe’s long-term future as the existence of the fund itself. By agreeing to jointly-issued bonds that will later be repaid under the new EU budget and partly though new region-wide taxes, the bloc has taken the first steps towards greater fiscal integration.

The ramifications of this shift are difficult to overstate. Closer fiscal ties would bring economic and political stability to a region that has been sorely lacking in both. A more united Europe will be able to better shape and direct its economic future and carve out a more influential role on the world stage. That will have repercussions for investors: Europe’s stocks bonds and currency could become a bigger feature of international portfolios.

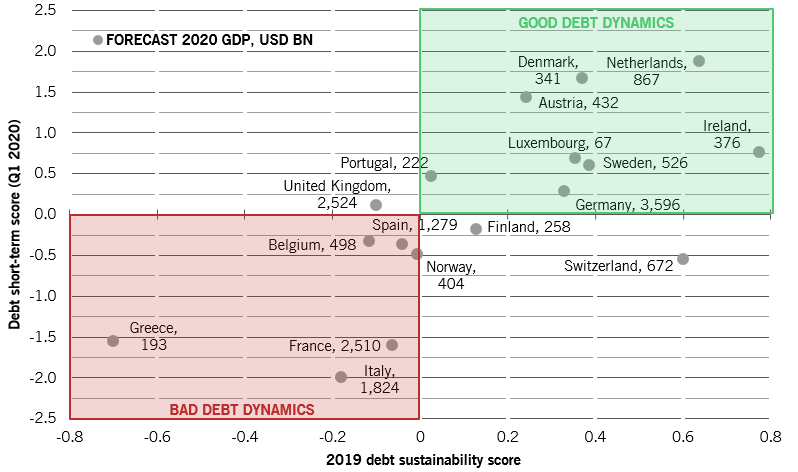

The path to European reform is treacherous, however. Although the deal has won the support of the EU 27, resistance to the recovery fund remains strong, particularly among the Netherlands, Sweden, Denmark and Austria - the region’s ‘frugal four’ economies. An unravelling of the scheme now, or indeed in future, cannot be ruled out. The risk of long political disputes and spending delays is still uncomfortably high.

Even so, with the unequivocal backing of Germany and France, there is every chance Europe will emerge from the Covid-19 pandemic with firmer political and economic foundations in place.