Asset allocation: autumn chill in markets

Expectations for tighter monetary policy are intensifying.

Central banks continue to lay the groundwork for a withdrawal of pandemic-era monetary stimulus in the face of rising inflation.

But higher interest rates are not the only concern for equity markets. Events in China are also worrying. Its strong recovery from the pandemic is now at risk as Beijing battles to avoid the collapse of its most indebted property company Evergrande.

We have reduced our forecasts for China’s economic growth by 1 percentage point for 2021-22 to 8.6 per cent as we expect the fallout from Evergrande debacle to spread throughout real estate sector. The country’s leading indicator is falling at a 5 per cent annualised rate, the same pace seen at the height of the Covid crisis in March 2020.

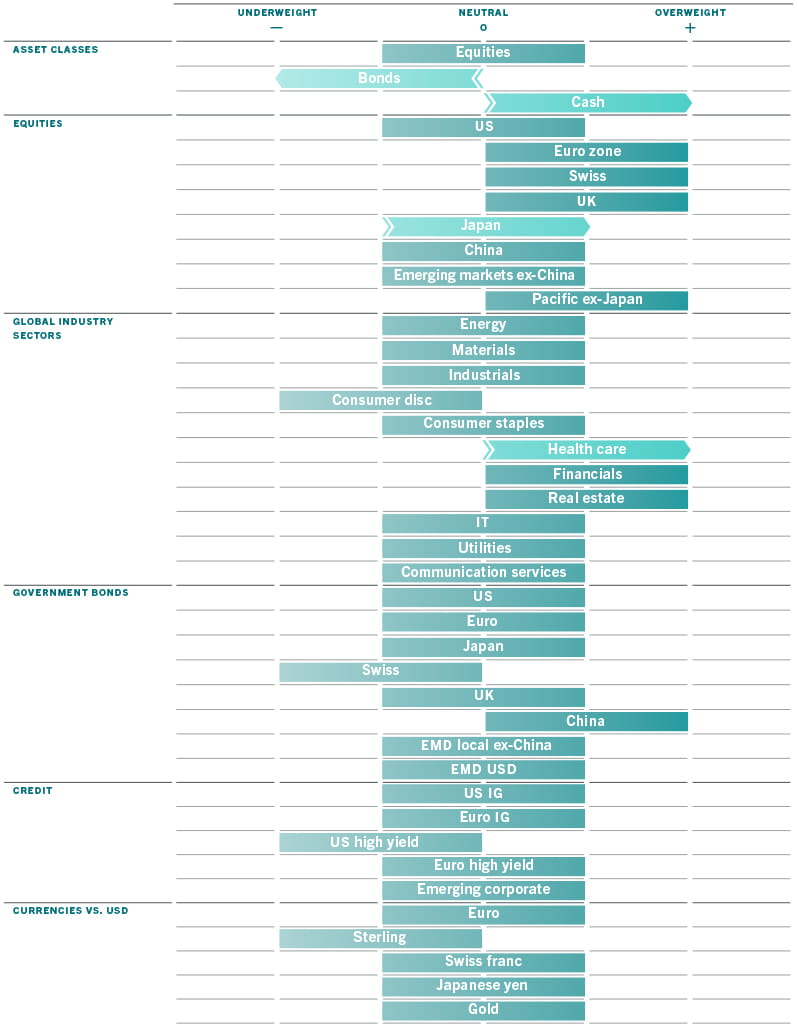

That shouldn’t come as a surprise considering real estate and related industries account for up to 30 per cent of Chinese GDP and property makes up more than two thirds of household wealth. Tighter monetary policy has led us to downgrade bonds to underweight while China's troubles have convinced us to increase exposure to defensive equity sectors and upgrade cash to overweight.

October 2021

Business cycle analysis shows world economic activity is cooling. Our global leading indicators contracted in August for the first time since the start of the post-pandemic recovery. We cut our global GDP growth estimates for the third month in a row to 6.2 per cent for 2021 from 6.4 per cent last month, led by downgrades of the US and China.

While slowing, growth in the US is still significantly above potential and we expect the world’s biggest economy to remain firm as job gains and wage increases boost consumer spending in the coming quarters.

Labour and raw material shortages and a spike in oil and gas prices are keeping inflationary pressures high, although the pace of consumer price rises has slowed in the most recent month.

Europe remains a bright spot as the region’s leading index rose for the fourth month in a row, supported by a weaker euro, the European Central Bank’s generous monetary stimulus and a successful vaccine rollout.

Our liquidity analysis shows central banks are still providing ample stimulus for now, but at a slower rate.

The world’s five major central banks are pumping in just USD500 billion of liquidity on a three-month basis, the lowest in 18 months and compared with USD1.5 trillion during the peak of the pandemic.

That said, our calculations show the US Federal Reserve's monetary tightening trajectory remains well behind the curve. The central bank’s “shadow rate”, adjusted for the effect of asset purchases, is about 500 basis points below its equilibrium levels.

That is despite Fed officials having taken a clear hawkish turn in their communications, suggesting a faster withdrawal of the central bank's USD120 billion monthly bond buying and a more aggressive interest rate hike campaign that could start as early as end-2022.

Liquidity conditions in the euro zone remain the loosest in the world and the European Central Bank should continue to provide stimulus in excess of GDP next year – the only monetary authority to do so among major economies.

China's central bank has stepped up net cash injections in response to a funding squeeze among real estate developers. We expect liquidity conditions to gradually loosen across the country in the coming months; the People's Bank of China may cut its reserve requirement ratio for banks for the second time this year when its medium-term loans mature.

Our valuation model supports our downgrade of bonds and neutral equity stance.

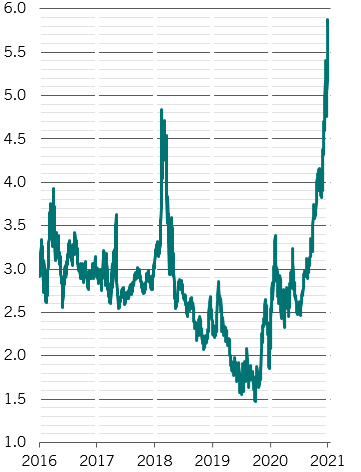

Despite a recent rise in yields, bonds remain below fair value and we expect a further correction in prices.

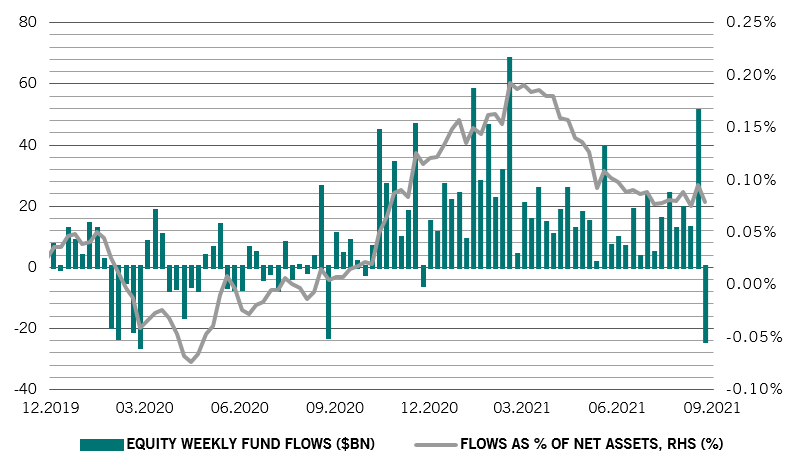

Equities have suffered their first weekly outflow of this year, of more than USD24 billion (see Fig. 2).

Rising bond yields are likely to weigh on equity earnings multiples given the asset class’ expensive valuation. Another red flag is corporate profits.

Earnings momentum has peaked, with 12-month forward earning per share now rising at 20 per cent for MSCI All-Country World Index, compared with 60 per cent in June.

Our models suggest earnings growth will continue to decelerate significantly in the coming quarters as the pace of economic expansion slows.

Our technical indicators paint a positive picture for riskier assets, supported by seasonal factors as well as moderate investor sentiment.