Sustainability-linked bonds: emerging market corporations up the ante

Emerging market companies are increasingly turning to an innovative type of bond to aid their green transition efforts.

Written by

Qian Zhang

Senior Client Portfolio Manager

Share this article

From coastal floods to potential slumps in agricultural output, emerging economies are more vulnerable to the effects of global warming than their richer counterparts.

A recent study by the University of Oxford commissioned by Pictet Asset Management found unmitigated climate change could reduce the world GDP per capita some 45 per cent by 2100, with emerging countries in latitudes that are already warm, such as India, suffering far greater economic losses.1

Just as importantly, however, the same report also stated that developing nations could provide many of the solutions that could halt or reverse global warming.

In some areas, emerging economies are well placed to take a lead in the battle against climate change. China, for example, already accounts for the lion’s share of photovoltaic cell manufacturing, is at the forefront of research and development and is one of the biggest adopters of the technology. India has one of the largest renewable energy capacity expansion programmes in the world, with a target of 175 gigawatts of installed renewable energy capacity by 2022, a five-fold increase from present levels.

Emerging market's role in the transition is already taking shape in the corporate bond market.

An increasing number of companies are beginning to embrace sustainable practices and, as they do so, they are making use of an innovative funding channel to finance their transformation.

The securities in question are sustainability-linked bonds. These are performance-based debt instruments issued with specific, corporate-wide sustainability performance targets (SPT), ranging from greenhouse gas emissions to water use.2

The bonds are structured to incentivise the adoption of sustainable business practices. If the issuer fails to meet its objectives within the pre-defined time frame, the coupon paid to the investor increases, by at least 25 basis points per annum.

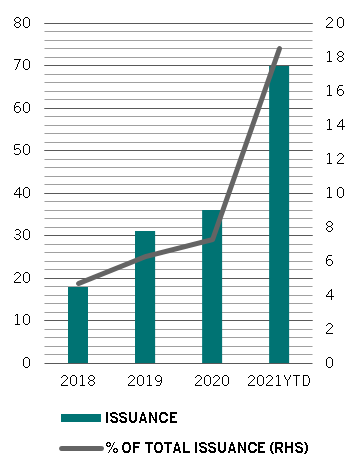

So far this year, sustainability-linked bonds have been on a tear in emerging markets. Issuance of corporate sustainability-linked debt has risen four-fold to USD70 billion in the first eight months of 2021, accounting for 18.5 per cent of total issuance (see chart).

That compares with less than 5 per cent three years ago, closing the gap with Europe, which has issued more of such paper than any other region.

Fig. 1 - Big jump

Issuance of sustainability-linked bonds among emerging market corporates

Source: JP Morgan, BondRader, data covering period 31.12.2017-31.08.2021

The distinguishing feature of sustainability-linked bonds is that they embed corporate-wide objectives.

This is in contrast with both sustainability and green bonds, which raise funds for specific environmental or sustainability-oriented projects.

It is still a nascent market, representing just 6 per cent of total environmental, governance and social (ESG)-labelled bond issuance in the world.3

But it is attracting growing interest among investors, chiefly because it allows them to benefit from an improvement in company's sustainability and choose issuers whose overall priorities align with their own.

It is also potentially more diverse than any other type of ESG bond market.

Green bonds tend to be issued by companies that operate in industries with significant environmental projects to finance. The market is dominated by energy, utility and construction companies.

By contrast, sustainability-linked bonds can be issued by companies operating in virtually any sector - including consumer goods technology, which tend not to have large green projects to fund.

This, in turn, give greater choices for investors.

So far, some 85 per cent of SPTs used in sustainability-linked bonds have been related to environmental targets such as greenhouse gas reduction, renewable energy and waste consumption, according to rating agency Standard & Poor's.4

Asian hotspots

Asia-based companies are leading the charge in sustainability-linked bonds. They account for more than 60 per cent of new bond issues; Latin American firms, by comparison, make up 20 per cent.

In some ways, that makes sense.

Extreme weather caused by global warming pose particularly serious threats to the bloc’s heavyweights China and India, the Oxford study found.

China is home to almost half of the world’s electricity and industrial assets, infrastructure that is most at risk from stranding, it said.

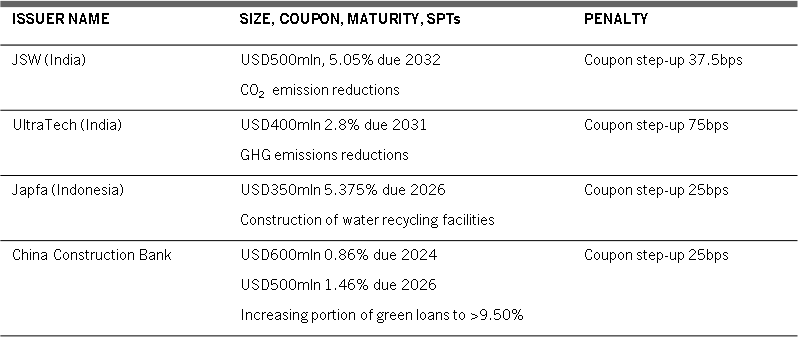

Fig. 2- Recent sustainability-linked bonds in Asia

We believe Asia will continue to dominate the emerging ESG bond market. As a decarbonisation laggard, the region can be expected to redouble its efforts to reduce carbon emissions.

China, for example, aims to become carbon neutral by 2060 in an ambitious goal that is expected to require some USD16 billion of investments, a large portion of which we expect will come via sustainability-linked corporate bonds.

Dissecting the greenium

For all their appeal, investors should submit sustainability-linked bonds to even greater scrutiny than conventional instruments.

On the one hand, investors should not lose sight of the credit profile of the issuer and valuation of bonds which we think should matter the most.

On the other, they should also scrutinise the issuer’s SPTs and the penalty mechanism.

This is because a lead time given for sustainability targets can sometimes be too long and the coupon step-up too modest in proportion to the original coupon rate – usually 5 or 10 per cent.

More thought needs to be given to the penalty structures in particular. Relying solely on a coupon step-up may lead to the unintended consequence of seeing investors rewarded for the issuer’s failure to hit sustainability targets. Other more progressive mechanisms include a mandatory purchase of carbon offsets.

The International Capital Market Association, an industry body which provides a set of voluntary guidelines that recommend best practices on structuring features, disclosure and reporting under the Sustainability-Linked Bond Principles (SLBP), encourages issuers to publish a framework and information template to cover their alignment with components of the SLBP where feasible.4

But we believe a standardised, and perhaps compulsory, disclosure and more robust objective-monitoring framework is needed to build investor confidence and unlock bigger investments in emerging economies, which sometimes lack the level of corporate disclosure and transparency required by foreign investors.

Sustainability linked bonds provide an alternative route for EM companies to aid their sustainability transition and tap into a wider group of investors.

Central bank endorsement could also help.

In January 2021, the European Central Bank became the world’s first monetary authority to classify sustainability-linked bonds as eligible as collateral and for its asset purchase programme.

The ECB has said the coupons on such debt must be linked to a performance target based on the environmental objectives set out in the EU Taxonomy Regulation and UN Sustainable Development Goals.

A similar development in emerging markets would be welcome.

Sustainability-linked bonds provide an alternative route for emerging companies to finance their sustainability transition and tap into a wider group of investors. They also provide a way for investors to align their investments with their own ESG objectives and principles.

Qian Zhang joined Pictet Asset Management in 2019. She is a Senior Client Portfolio Manager for the Fixed Income Emerging Market Corporate and Greater China Debt team.

Before joining Pictet, she was a client portfolio manager in J.P.Morgan Asset Management Global Fixed Income team and Emerging Markets Debt team, based in both London and Hong Kong. Prior to JPMorgan, Qian worked for Merrill Lynch in Tokyo where she focused on Interest Rate Derivatives.

Qian obtained a B.A. in Economics and Statistics from Peking University, Beijing, China and an M.Sc. in Mathematical Risk Management from Georgia State University, U.S. Qian is a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.