Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Bond investors need to understand the volatility cycle

Fixed income markets have become increasingly volatile, a trend that looks set to continue. Investors need to adapt themselves.

Written by

Jon Mawby

Co-Head of Absolute & Total Return Credit

The recent surge in bond yields has rocked fixed income investors. Losses on one benchmark bond index from its 2021 highs have already exceeded their near 11 per cent drawdown during the global financial crisis in 2008. What’s more, this sort of volatility isn’t going away – indeed, it has jumped sharply in recent weeks. Investors will need to learn a different, more active approach to fixed income investing.

An era of unconventional monetary policy – which drove yields to exceptionally low levels – is coming to an end amid a broadly global inflationary surge. This suggests bonds are no longer the safe haven for investors they once were, with particularly significant risks for those holding longer-dated securities, an investment staple for institutional investors with long-term liabilities, such as pension funds.

The roots of this predicament are 30 years in the making. It has been a period of ever-intensifying financial repression, with central banks deliberately holding interest rates below the rate of inflation. The result was not only that yields were artificially compressed, but also that the ups and downs of credit and economic cycles were far less pronounced.

When, in 2006, then-UK Chancellor Gordon Brown claimed to have ended economic ‘boom and bust’, he was right – to a point. But the side effect of smoothing these cycles through highly interventionist policies was periodic and severe bouts of volatility. These have included the 1987 stock market crash, the economic and property crisis in Japan, the tech bubble bursting, the sovereign debt crisis, Grexit, Covid. Common to each of these episodes is that central banks stepped in to ‘save’ markets, resulting in volatility cycles caused by investor herding and subsequent market tightening and repricing.

Another side-effect financial repression is that traditional credit markets have become more highly correlated with equities, shrinking investors’ margin for error. Which means future return characteristics of fixed income assets will not be the benign ones of the past four decades. Add in routine spikes in volatility and investors now face difficult periods.

In light of these dramatic changes, how should investors approach fixed income selection and portfolio construction? In his 1998 book, Winning the Loser’s Game, Charles Ellis offered an insight by looking at investing through the lens of sport. Successful professional athletes, he argued, tend only to be defeated by those with superior skills. By contrast, amateurs, defeat themselves through poor play, such as unforced errors in the case of tennis. By extension, investors who can avoid making mistakes – like chasing returns – and yet exploit opportunities that present themselves will tend to succeed.

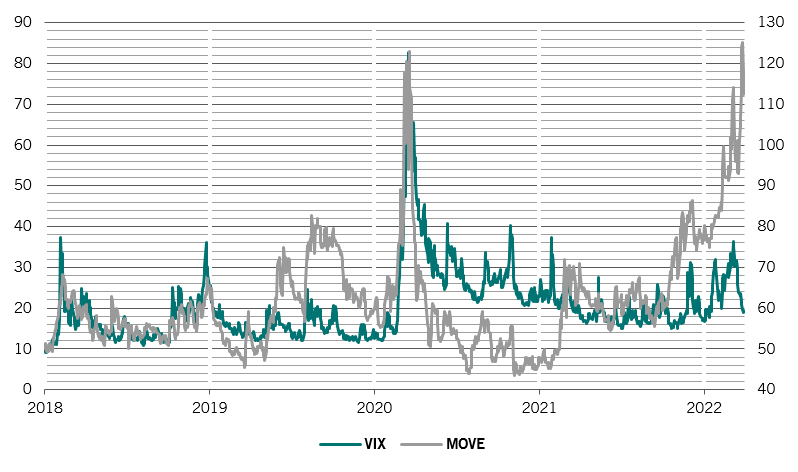

Fig. 1 - Volatile volatility

CBOE SPX S&P 500 volatility (VIX), Merrill Lynch Move 3-month bond volatility, price indices

That’s especially true now. The sheer number of credit investors is staggering, not least because of the ever-growing number of passive products that are available. This has increased volatility as an ever-larger number of investors move in and out of the market simultaneously, particularly through exchange traded funds. Meanwhile, there has been a huge accompanying deterioration in the credit quality of company issuing bonds. As a result, investors’ risks have grown significantly.

This idea of not chasing returns will inevitably feel alien to investors. Reducing risk when valuations are stretched and taking opportunities to add risk when other investors are fearful is indeed contrarian. Yet, it is this contrarian, value-focused mindset and objective assessment of the state of credit markets that offers the strongest basis on which to navigate these volatility cycles.

The Covid pandemic and the events of March 2020 are salient examples. Many high yield bond investors suffered significant losses during the worst of the crisis. But for those who had previously taken steps to minimise risk and were therefore well placed to take advantage of the value that was on offer, there were many good quality credit securities available at multiple percentage points below their par values.

Today, interestingly, it is investment grade credit that appears particularly risky. That’s because in this part of the market, asset allocation decisions come with very little margin of error and much of the generational high risk previously outlined. In contrast, rising stars within the high yield bond market – sub-investment grade companies whose financial prospects have been improving – offer much better risk-adjusted prospects.

Given how markets have behaved in recent times, it is inevitable that there will be many more bouts of intense bond market volatility, accompanied by severe peak-to-trough declines. Interestingly, bond volatility has spiked even as equity market volatility has remained relatively well behaved, an anomalous condition that few fixed income investors would have been prepared for (see Fig. 1).

Though we can produce a list of potential risks in store, we can’t predict the specific catalyst. What we can do, however, is position ourselves to take advantage of these events when they happen. This means understanding what reflects fair value in asset allocation decisions and then trying to realise as much of the total return available as possible – but without becoming greedy and chasing returns unnecessarily.

read more about fixed income investing

Dispersion dominance: how bond investors can capitalise on emerging markets' idiosyncrasies

Because the countries that constitute the emerging market debt universe are so very different from one another, investors should consider an absolute return approach.

February 2022

Sovereign bond investing: a climate-focused approach

When it comes to responsible investment strategies, sovereign bonds have so far largely been overlooked. We believe that needs to change.

March 2022

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.