Asset allocation: in a holding pattern

It’s been a tough month for investors. From the Italian political crisis to simmering US-China trade tensions, not to mention a sharp sell-off in some emerging market currencies, there has been plenty to worry about. But there’s no need for panic. For one thing, the global economy is humming along, even though the pace of growth has slowed in the past few months. And while the US Federal Reserve seems intent on sticking to its well-publicised programme of gradually raising interest rates, we don’t think it is in a hurry to tighten monetary policy. Nor, for that matter, are any of its peers in the developed world. If anything, we believe monetary authorities are prepared to slow the pace of stimulus withdrawal should threats to growth materialise, particularly the European Central Bank.

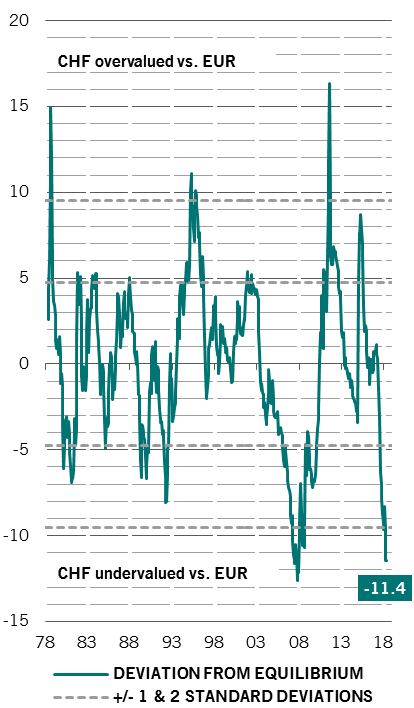

Against this backdrop, we’re keeping our neutral position on equities, bonds and cash. We are dialling back our cyclical bias slightly by lightening up on financials and raising our exposure to the Swiss franc to overweight as a hedge against market turbulence.

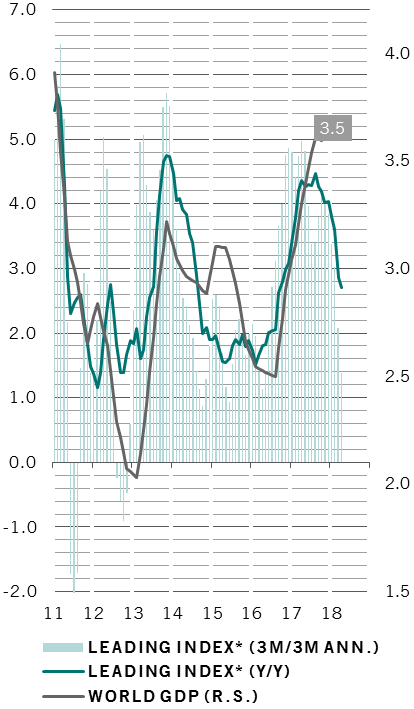

Our business cycle gauges continue to show a divergence in economic conditions between developed and emerging countries. Leading indicators in industrialised nations fell for the fourth consecutive month, while the readings for their developing counterparts have held steady. In the US, the construction sector is starting to feel the chill from monetary tightening; other data show private consumption is healthy.

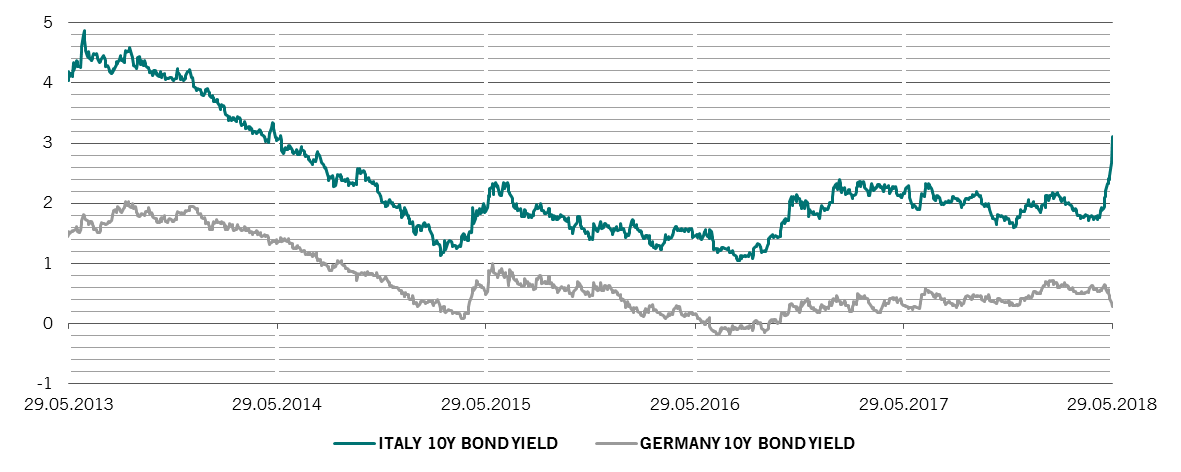

The outlook is a little less encouraging for the euro zone, where leading indicators dropped below the three-year average even before the latest bout of political turmoil in Italy. That said, we think the euro zone economy will be supported by improving labour market conditions and an uptick in business investment. We don’t expect the Italian political crisis to pose a systemic threat to the region’s banking system. What is more, European leaders may yet come up with policies to soothe investor jitters at their June summit.

World leading indices and GDP growth, %

Our liquidity readings remain negative for riskier assets. Worries about Italy have helped send the dollar higher, which is in turn putting pressure on currencies of emerging countries that are most reliant on dollar funding, such as Argentina and Turkey. We expect the effect of tighter liquidity to be felt more in coming months: central banks are removing liquidity at an annualised rate of about USD700 billion and our analysis shows it takes up to 18 months for any tightening to feed through to the broader economy.

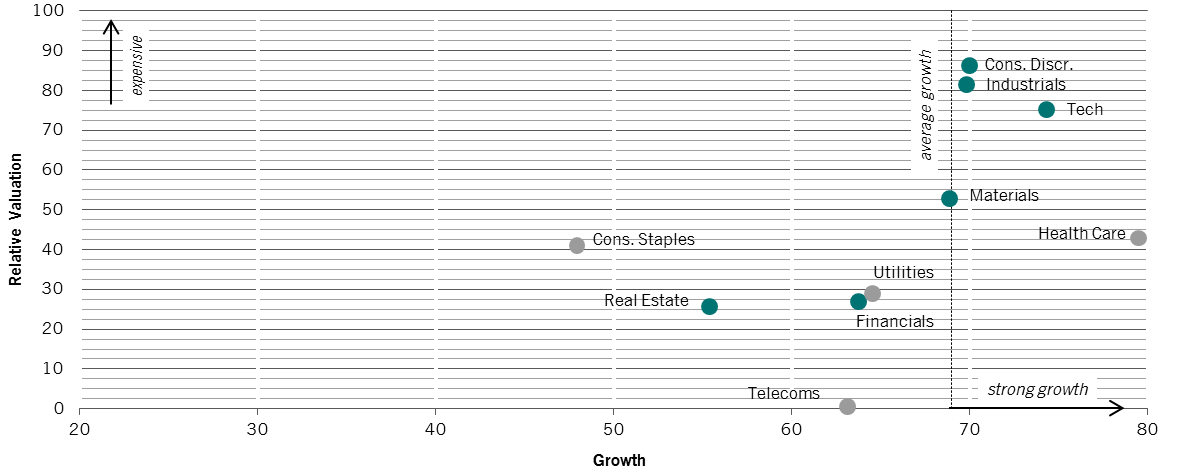

The valuation signals we monitor suggest taking a neutral stance on equities. But there’s a wide dispersion in valuations between regions and sectors. Japan remains the cheapest developed equity market. The US is the least attractive, especially if we are right in assuming that market expectations for corporate earnings growth will ease to a more realistic level of about 18 per cent this year from the current 22 per cent. Commodity-related sectors, such as energy and materials, look more appealing as they tend to outperform in the late stage of the economic cycle. Other cyclical sectors – industrials and consumer discretionary stocks in particular – look expensive. Elsewhere, emerging local currency debt and currencies look attractive after a recent sell-off; European credit is vulnerable to any re-rating of euro zone sovereign debt triggered by Italy's political ructions.

Technical indicators have turned positive for some riskier assets after a recent correction in stock markets. However, equities are likely to struggle due to seasonal factors - summer months don't tend to be kind to stocks.