Thematic stocks: a smarter approach to global equity investing

A concentrated portfolio with a high active share Global Thematic Opportunities aims to deliver superior returns by investing in specialised companies operating in the world's most dynamic industries.

Readers of the financial press could be forgiven for thinking that active investing - particularly the long-only kind - is no longer worthwhile.

We are told that, as stocks are getting better at reflecting all available information, and with portfolio management fees taking a sizeable bite out of investment returns, equity investors should abandon their pursuit of alpha altogether.

Clearly, passive investing offers a simple solution. Fees are low and there is no risk of disappointment. But it would be wrong to say that long-only active equity investment has outlived its usefulness.

Research shows that a significant proportion of active equity portfolios do distinguish themselves over time. Provided their investment managers prevent the dilution of their research - which often happens when they default to a benchmark - long-only equity strategies have the potential to deliver superior returns.

This commentary sets out why Pictet Asset Management believes that thematic investment represents a credible alternative to mainstream global equity portfolios.

We describe the distinctive qualities of Pictet AM’s thematic approach, and why they serve as a lens through which to assess and identify investment opportunities.

02

Dynamic industries, enduring sources of capital growth

The primary purpose of a thematic equity strategy is to invest in stocks whose returns are influenced by structural forces of change that evolve independently of the economic cycle. In other words, thematic investing focuses on identifying enduring sources of capital growth.

At Pictet AM, we achieve this by following a disciplined investment process. Central to our approach is the construction of a distinctive lens through which we can identify long-term investment opportunities.

With the help of outside experts from industry and academia, we undertake research to unearth the most dynamic areas of the global economy, industries whose growth prospects are being transformed by profound structural trends, forces that we call "megatrends". Our view is that the listed companies operating within the globe's fastest-evolving industry sectors offer among the best prospects for capital growth.

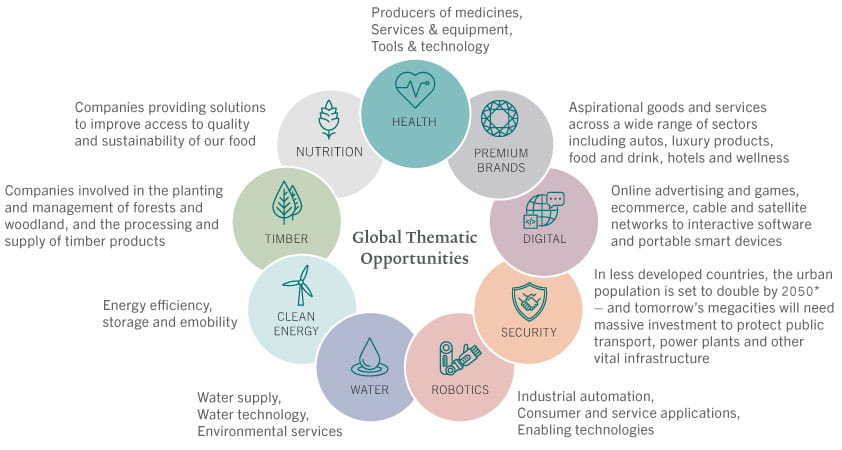

One of the industries we have identified using this process is water. Water services companies operate in an environment in which structural forces of change abound. For instance, climate change and urbanisation – the seemingly unstoppable migration of the world’s population from the country to the city – promise to speed up the depletion of the planet’s water resources unless new water-preservation or recycling technologies can be developed.

Another industry that is both witnessing profound change and home to a rich variety of investment opportunities is robotics. Here, rapid technological advances in artificial intelligence and robotics technology mean robots are becoming part of everyday life, whether that's in the home, in the office or on the factory floor.

Water and robotics qualify as investment themes because they possess a number of distinguishing characteristics that make them both investible and sources of superior long-term capital growth. In fact, all of the industries that form part of our thematic lens meet the following criteria:

Thematic purity - For an industry segment to be considered part of our investment universe, it should be home to a sufficiently large group of companies for whom structural trends are a major (and quantifiable) source of earnings growth. In addition, for an individual company to qualify as an investment candidate, it must demonstrate specialist expertise within that industry. For instance, we would consider a water services company as a potential investment only if it derived a sizeable proportion of its revenues and profits from that specialist activity.

Liquidity – The ability to buy and sell a stock in large quantities without adversely affecting its price is another indication of the investibility of a theme. A theme is technically investible as long as the stocks of thematically-pure companies can be liquidated easily within five days.

Minimal overlap with standard equity benchmarks – The final criteria is the distinctiveness of the investment universe. At Pictet AM, we define distinctiveness as the extent to which the companies that make up the industries we invest in also feature in mainstream global equity benchmarks such as the MSCI World.

Using this process, we have identified nine rapidly-evolving segments of the economy - all of which included in our thematic universe. In addition to water and robotics, these are are timber, health, nutrition, security, digital tech, premium-brand goods and clean energy.

Dynamic, Fast-growing and home to attractively-valued specialist companies

Industries that form part of Global Thematic Opportunities investment universe

Source: Pictet Asset Management, as of 31.08.2018

We believe that Pictet AM’s thematic approach gives portfolio managers every opportunity to maximise their investment selection skills.

That is primarily because thematic investing incorporates a broader view of alpha, one that goes beyond simply beating an index; it encompasses a holistic approach, starting with the selection of an appropriate – and we believe superior – group of investment candidates.

Since there are no consensus indices for thematic strategies, the investment team does not need to obsess about matching a benchmark but is able to focus on finding the most attractive stocks for its portfolio instead. The approach is truly benchmark agnostic.

There a number of features of the thematic investment universe that we believe make it a viable alternative to mainstream global equity strategies.

The first is that the universe is large – there are almost as many thematic stocks as there are companies represented in mainstream equity indices. This means it is just as easy to diversify an equity portfolio with a thematic approach as it is with a traditional that is benchmarked against a standard world equity index.

The second, and perhaps a more important characteristic, is that thematic companies are, at the same time, very focused in their business activities, with ‘pure plays’ making up a significant part of the investible market. Pure plays are always favoured over more diversified companies. That is a deliberate choice.

There is, in fact, a large body of research that suggests specialist companies make for better long-term investments than larger, more diversified firms. This literature, which appears to have been overlooked in recent years, points to the existence of a “conglomerate discount” – i.e. that big firms are worth less than the sum of their parts.

Our portfolio managers determine a company's degree of specialisation using a proprietary indicator we call thematic purity, which is based on a firm's enterprise value.

If, for example, a company operating within clean energy is found to have a purity of 50, this means that half of its enterprise value is derived from products and services that cater to that specific industry.

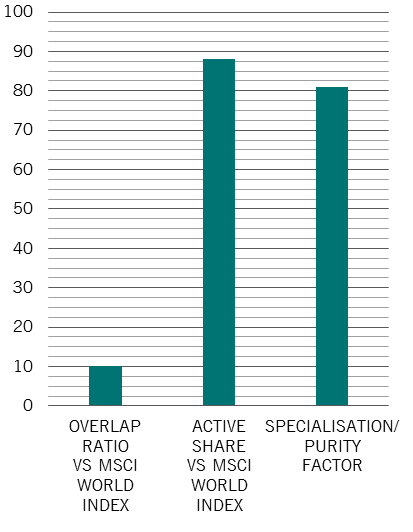

The average purity of the companies in our thematic portfolios is approximately 80.

The clear organisation and the simple construction process combine to maximise the likelihood of successful stock selection.

There is ample evidence that stock picking within – rather than across – sectors can work reasonably well for talented analysts. They seem to be able to discriminate between stocks that will perform well – their “best ideas” – and those that will do less well, on average.

A third feature of thematic equity investments is that - in most cases - they are not accessible via mainstream stock indices.

In other words, the make-up of a thematic equity portfolio bears little resemblance to standard global stock indices. This also reflects the fact that our investment teams have complete freedom in the selection of their stocks, eliminating ‘forced’ investment decisions that are made simply to alter a portfolio's tracking error.

03

Index-tracking and thematics

The proponents of passive management tell us that indexation is the best, if not the only imaginable, solution: it offers a low cost, perfect replication of market performance.

What is forgotten in this somewhat simplistic view is that the chosen index does generally not include the entire market. Any market index is an arbitrary choice both in terms of the stocks that it includes and the weighting of those stocks.

There cannot be any purely passive investment since the selection of any index is very much an active decision. The obsessive focus on standard benchmarks also encourages investors to disregard stocks that are not included in those indices.

This usually results in a large cap bias. We might therefore be able to obtain better results by simply expanding the investment universe.

Pictet AM’s thematic teams exploit this fact. They do not try to beat an arbitrary index through tightly controlled relative bets – to control tracking error – but focus instead on the creation of and selection from the most attractive investment universe possible.

04

A concentrated portfolio built company by company

Global thematic opportunities: a high conviction equity strategy

Overlap ratio, active share %, purity factor

Source: Thomson Reuters Datastream, Pictet Asset Management. Data as of 31.08.2018

The culmination of this investment process is Pictet Global Thematic Opportunities, a relatively concentrated portfolio that has a high active share, one close to around 90.

The vast majority of its holdings are in specialist companies that do not feature in mainstream global equity indices - a reflection of the strong investment convictions of our investment managers.

The active investment management of the thematic approach overcomes the shortcomings inherent in traditional long-only equity funds. The freedom from obsessive benchmark tracking facilitates stock selection and avoids forced investments. There is no complex portfolio construction element than can dilute the value of good stock selection.

It is a genuinely active strategy in every sense.

*Ammann, Manuel and Hoechle, Daniel and Schmid, successful stock picking. Markus M., “Is There Really No Conglomerate Discount?” (Working paper, 2011). Larry H. P. Lang, and René M. Stulz. “Tobin’s Q, Corporate Diversification,and Firm Performance”. Journal of Political Economy 102.6 (1994): 1248–1280.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.