Overview: risky business

If the stars were aligned for risk assets during most of the past decade, they look distinctly less bright for the coming year. An end to monetary stimulus across much of the world, the fading effects of the US’s fiscal boost, trade wars, uncertainty over Italy and Brexit are all likely to play their part.

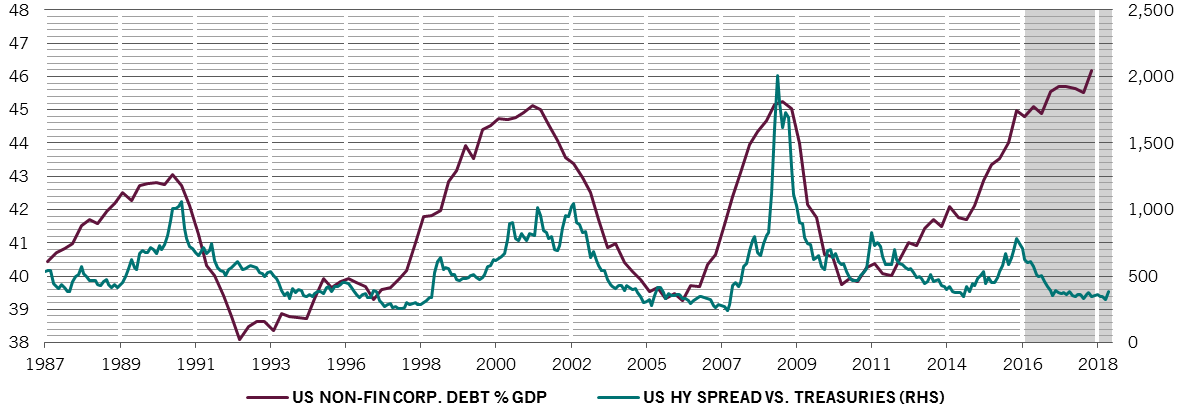

Slowing economic growth and a squeeze on corporate profit margins will take some of the shine off equities. And with wages at last growing and feeding through to inflation, bonds aren’t likely to be much of a haven either: both investment and speculative-grade credit look particularly vulnerable to a correction. On the other hand, a weaker economy could be good for long-dated and index-linked US Treasuries and gold, while an overvalued US dollar could give back some ground. Under the circumstances, cash is set to be the best performing asset class.

US macroeconomic and market cycle indicator relative to long term history (percentile)1

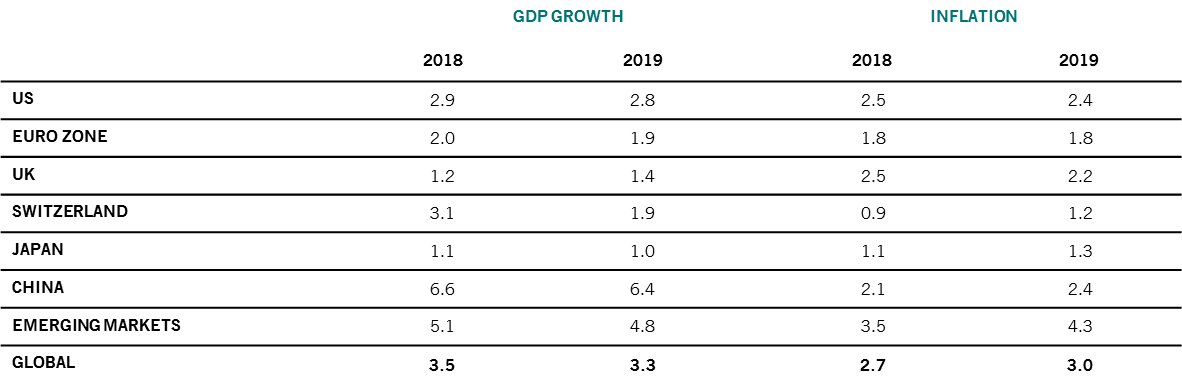

Our business cycle analysis suggests global economic growth will continue to slow – to 3.3 per cent from 3.5 per cent in 2018 – amid softening survey evidence, a winding down of US fiscal stimulus and rising bond yields. Underlying inflationary pressure will pick up, particularly in emerging markets. We’re forecasting global consumer price inflation of 3.0 per cent from 2.7 this year, with wage inflation already at a 10-year high across all major developed economies. A mix of slowing growth and rising inflation has historically been bad news for both bonds and equities, leaving cash the best alternative.

Central banks outside China will gradually turn off the liquidity taps during the coming year, setting the markets up for yet more ructions. Although monetary stimulus worldwide isn’t expected to peak until the end of 2019, a dramatic reduction in net flows – to USD140 billion from USD2.6 trillion in 2017 – is bound to make its mark on risk assets. Excluding China, global central banks will, for the first time since the global financial crisis, be net sellers of financial assets.2

And given the dollar’s primacy in the global financial system, all eyes will be on whether the US Federal Reserve doles out three more quarter point rate hikes rates, as most economists expect. Indeed, among the risks that worry us is the possibility of spike in US inflation that either forces Fed to act more aggressively or to shift to a new regime such as asset price targeting or rule-based rate setting. There’s the additional risk that President Donald Trump’s outspoken criticism of the Fed’s hikes ends up being counterproductive if it prods the central bank to prove its independence by taking an increasingly hawkish stance. None of this forms part of our base-case scenario, but they are possibilities that are worth insuring against.

Equity valuations are broadly neutral after one of the biggest contractions in earnings multiples ever seen outside of recessions – the 12-month forward price to earnings ratio for the MSCI US index dropped from 19.2 times at the start of the year to a low of 14.9 times at the worst of the October market rout.

We see global corporate earnings rising by around 7 per cent in the coming year, which is slightly below consensus, with profit margins coming under pressure, primarily from rising wages and higher debt servicing costs. As a result, we expect the MSCI World All Country World Index to deliver negligible to flat total returns, with losses on US shares offset by other markets.

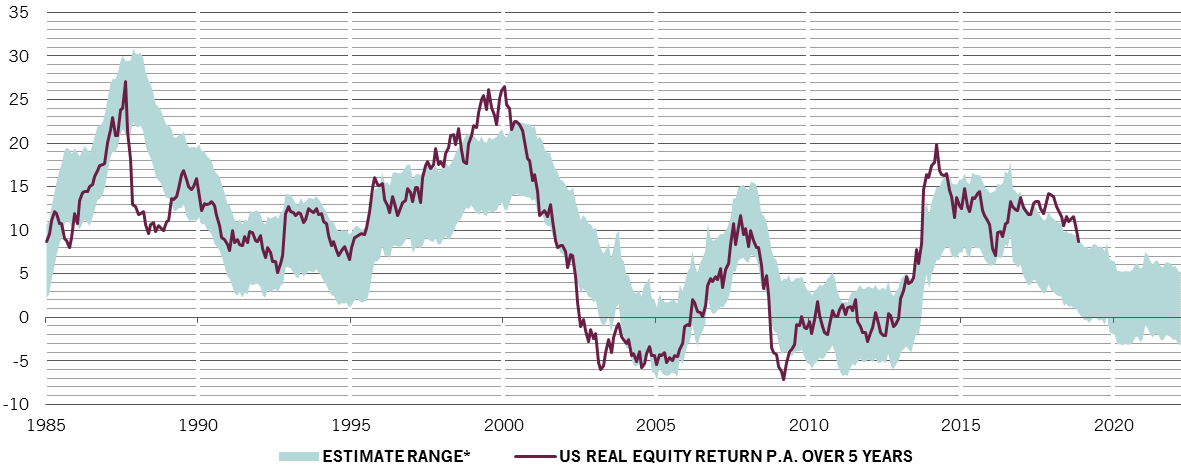

Meanwhile, growing inflationary pressures and a reduction in central banks’ debt purchases are set to push up bond yields, particularly now that wages are at long last starting to respond to unprecedented labour shortages across all major economies. This matters for equities too. A 1 percentage point rise in US bond yields reduces the fair value of the S&P 500 by around 20 per cent on our discounted cash flow models – though for equity valuations, it’s the gap between real bond yields and long-term EPS growth that matters. We think that a rise in 10-year Treasury yields to above 3.5 per cent would hurt equities from two fronts. Investors would be prompted to switch to bonds from shares. And rising yields would push up market interest rates, hitting borrowers and the economy more generally.

For now, our technical and sentiment indicators suggest the market shakeout that unfolded over the final months of 2018 seems overdone. Both global growth and corporate earnings may have peaked but there’s no sign of an impending economic downturn. Yes, the global yield curve has inverted this year, but historically recession has only followed a year or two after that occurs. As a result many risk assets look oversold, leaving them ripe for a sharp rally, particularly into any good news. This could be a US-China trade deal, or hints from the Fed that it is in a position to slow policy tightening. In any event, equities’ downside is limited by investors’ bearishness.